Printable Cri 200 Nj Form

Printable Cri 200 Nj Form

| Fact Name | Details |

|---|---|

| Governing Body | The form is regulated by the New Jersey Division of Consumer Affairs. |

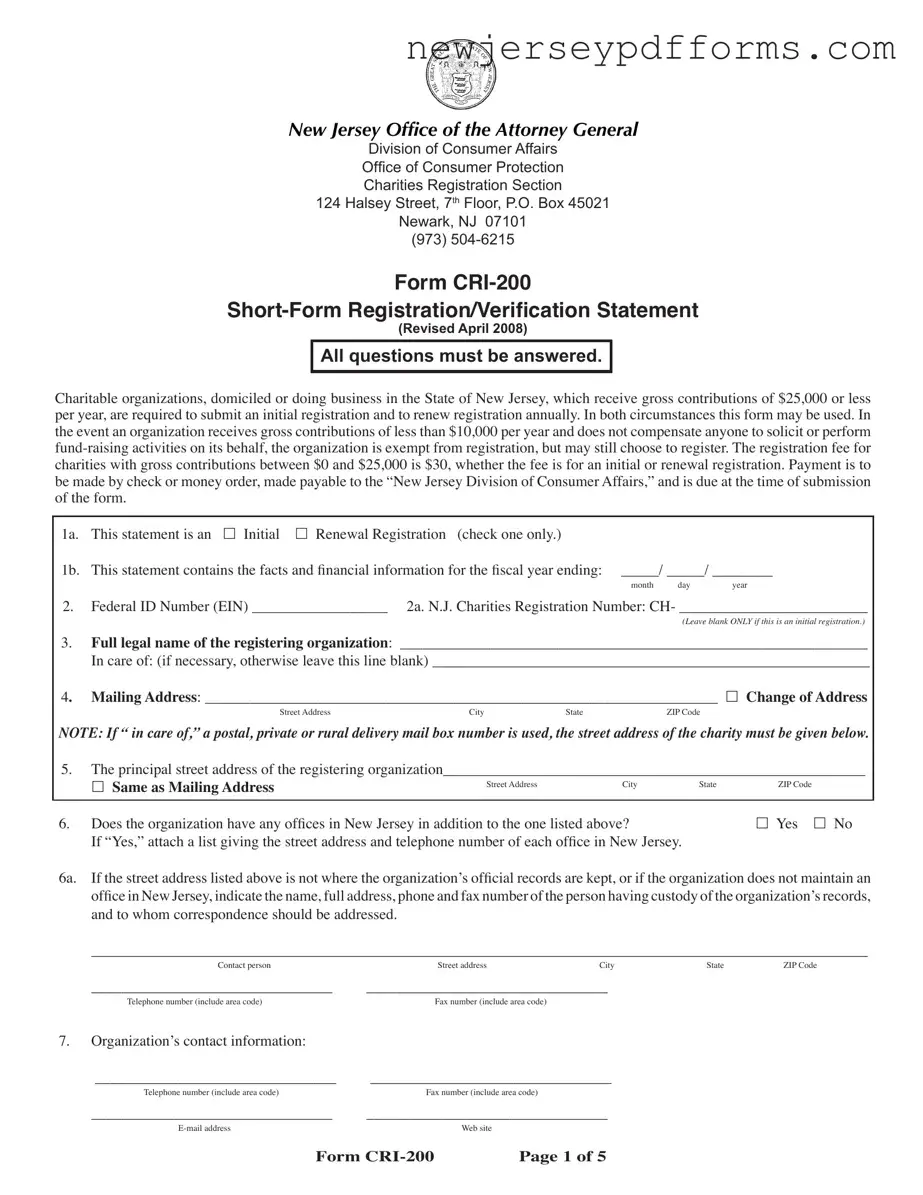

| Purpose | This form is used for the Short-Form Registration/Verification Statement for charitable organizations. |

| Eligibility Criteria | Organizations must receive gross contributions of $25,000 or less per year to qualify. |

| Exemption | Organizations with gross contributions below $10,000 and no paid solicitors are exempt from registration. |

| Registration Fee | The fee is $30 for both initial and renewal registrations. |

| Submission Requirements | All questions must be answered, and necessary documents must be attached. |

| Renewal Timeline | Annual renewals are due within six months after the fiscal year-end. |

| Payment Method | Payments must be made via check or money order, payable to the New Jersey Division of Consumer Affairs. |

| Contact Information | For questions, contact the Charities Registration Section at (973) 504-6215. |

Free Annulment Forms - Information subpoena forms are available on the New Jersey Judiciary's website.

When forming an LLC, having a comprehensive Operating Agreement is vital to define how the company will be managed and to clarify member responsibilities. For more details on crafting this essential document, you can visit https://topformsonline.com/operating-agreement, which provides valuable insights and guidelines to avoid ambiguities and ensure smooth operations.

Nj Senior Freeze Deadline Extended - Consulting with tax professionals may assist in ensuring the form is filled out correctly and completely.

1040-nr Due Date - All amounts on the NJ-1040NR must be reported in U.S. dollars and reflect the actual income earned.

When filling out the CRI-200 NJ form, people often make several common mistakes that can lead to delays or complications in the registration process. One frequent error is failing to check the correct box for whether the statement is an initial or renewal registration. This oversight can cause confusion and may result in the form being rejected.

Another common mistake is neglecting to provide the organization’s Federal ID Number (EIN) or the New Jersey Charities Registration Number. Leaving these fields blank can lead to processing delays, as the registration cannot be completed without this essential information. It is crucial to double-check that all required identification numbers are accurately entered.

Many individuals also overlook the importance of providing a complete mailing address. If the mailing address is incorrect or incomplete, important communications from the Division of Consumer Affairs may not reach the organization. Additionally, if there is a change of address, it must be clearly indicated on the form to avoid any issues.

Inaccuracies in financial reporting are another significant mistake. When reporting gross contributions, individuals sometimes report net amounts instead. It is essential to report all figures as gross, not net, to ensure compliance with the requirements outlined in the form.

Another area where mistakes frequently occur is in answering eligibility questions. If none of the conditions in question 8 are met, organizations must use the Long-Form Initial Registration Statement instead of the Short Form. Misunderstanding this requirement can lead to submitting the wrong form, which complicates the registration process.

Additionally, some organizations fail to attach necessary documentation when required. For example, if there have been changes in the organization’s name or status, supporting documents must be included with the registration. Failing to provide this information can result in rejection of the application.

Lastly, many individuals do not ensure that the form is signed by two authorized officers, including the chief financial officer. This requirement is crucial, and without the proper signatures, the registration will not be valid. It is important to confirm that all signatures are present before submission to avoid unnecessary delays.

What is the CRI-200 form?

The CRI-200 form, also known as the Short-Form Registration/Verification Statement, is a document required by the State of New Jersey for charitable organizations that receive gross contributions of $25,000 or less per year. This form must be completed and submitted for both initial and annual renewal registrations. It ensures that the organization is compliant with state regulations regarding charitable solicitations.

Who needs to fill out the CRI-200 form?

Any charitable organization that is either domiciled in New Jersey or conducts business there and receives gross contributions of $25,000 or less annually must complete the CRI-200 form. If an organization receives less than $10,000 per year and does not compensate anyone for fundraising, it is exempt from registration but may still choose to register.

What is the registration fee for the CRI-200 form?

The registration fee for organizations with gross contributions between $0 and $25,000 is $30. This fee applies whether the submission is for initial registration or for renewal. Payment must be made via check or money order, made out to the “New Jersey Division of Consumer Affairs,” and submitted along with the form.

What information is required on the CRI-200 form?

The CRI-200 form requires various pieces of information, including the organization's legal name, mailing address, principal street address, and contact details. It also asks for the organization’s federal ID number, New Jersey Charities Registration number (if applicable), and financial information regarding contributions and expenses. Additionally, the form includes questions about the organization’s activities, any changes in status, and whether it has been involved in any legal issues.

How often must the CRI-200 form be submitted?

The CRI-200 form must be submitted annually for renewal, within six months of the organization’s fiscal year-end. Organizations should also submit the form for initial registration if they have never registered before. If the renewal is submitted after the due date, a late fee of $25 will be added to the $30 registration fee.

What happens if an organization does not file the CRI-200 form?

If an organization fails to file the CRI-200 form, it may face penalties, including fines or legal action. Additionally, non-compliance can affect the organization’s ability to solicit donations legally within New Jersey, which could hinder its fundraising efforts.

Can an organization submit the CRI-200 form online?

Currently, the CRI-200 form must be submitted by mail. Organizations should complete the form and send it, along with any required attachments and payment, to the New Jersey Division of Consumer Affairs at the specified address. For any updates regarding online submissions, organizations should check the New Jersey Division of Consumer Affairs website.

Where can I find more information about the CRI-200 form?

More information about the CRI-200 form, including instructions, forms, and a fee schedule, can be found on the New Jersey Division of Consumer Affairs website. If further assistance is needed, organizations can contact the Charities Registration Section by calling their hotline during regular business hours.

Misconception 1: The CRI-200 form is only for large charities.

This is incorrect. The CRI-200 form is specifically designed for charitable organizations in New Jersey that receive gross contributions of $25,000 or less per year. Even smaller organizations can and should use this form to register.

Misconception 2: Charities earning less than $10,000 do not need to register at all.

While it's true that organizations earning less than $10,000 and not compensating anyone for fundraising activities are exempt from registration, they still have the option to register if they choose. Registration can enhance credibility and transparency.

Misconception 3: The registration fee is waived for all charities.

This is a misunderstanding. All charities using the CRI-200 form must pay a registration fee of $30, regardless of their gross contributions. This fee is necessary for processing the registration.

Misconception 4: The CRI-200 form is a one-time requirement.

In reality, registration is an ongoing obligation. Charitable organizations must renew their registration annually. This ensures that the information remains current and accurate.

Misconception 5: Only the organization’s president needs to sign the form.

This is not accurate. The CRI-200 form must be signed by two authorized officers of the organization, including the chief financial officer. This requirement adds an extra layer of accountability.

Misconception 6: The form can be submitted without any additional documentation.

Submitting the CRI-200 form may require additional documents depending on the organization’s circumstances. For example, if there have been changes in the organization’s name or IRS status, supporting documents must be attached.

Misconception 7: The organization’s address can be a P.O. Box only.

This is misleading. While a P.O. Box can be used, the organization must also provide a physical street address. This ensures transparency and allows for proper communication.

Misconception 8: If the organization has registered once, it does not need to provide the IRS 990 form again.

This is not true. If the organization was required to file an IRS 990 for the fiscal year being reported, a copy must be submitted with the CRI-200 form each year. This keeps financial reporting consistent and transparent.

The Form CRI-150-I serves as the Long-Form Initial Registration Statement for charitable organizations in New Jersey. Unlike the CRI-200, which is designed for smaller charities with gross contributions of $25,000 or less, the CRI-150-I is required for organizations that exceed this threshold. This form gathers extensive information about the charity's structure, governance, and financial practices, ensuring that larger entities comply with state regulations. The CRI-150-I emphasizes detailed disclosures, such as the charity's mission, board members, and financial statements, which are critical for maintaining transparency and accountability in fundraising activities.

The Form CRI-300R is the Long-Form Renewal Statement for charities that have previously registered. This document is similar to the CRI-200 in that it requires annual updates, but it is intended for organizations that have previously filed the Long-Form Initial Registration Statement. The CRI-300R demands comprehensive information about any changes in the organization’s structure or operations since the last filing. Both forms aim to keep the state informed about the charity's activities and ensure compliance with state laws, but the CRI-300R requires a more thorough account of the charity's ongoing operations.

The IRS Form 990 is a federal tax form that most tax-exempt organizations must file annually. This form provides a detailed overview of a charity's financial activities, including revenue, expenses, and executive compensation. Similar to the CRI-200, the IRS Form 990 is a tool for transparency, allowing the public to access information about how a charity operates and manages its funds. However, the IRS Form 990 is more comprehensive and includes sections that may not be present in the CRI-200, such as detailed financial statements and governance practices.

The IRS Form 990-EZ is a shorter version of the IRS Form 990, intended for smaller organizations with less complex financial activities. Like the CRI-200, it simplifies the reporting process for charities that do not exceed certain revenue thresholds. Both forms serve to ensure that smaller organizations maintain transparency while reducing the burden of extensive reporting. However, the 990-EZ still requires essential financial disclosures, making it a valuable tool for both the IRS and the public.

Understanding financial performance is crucial for any organization, and utilizing tools such as the Profit and Loss form can aid in this process. For those seeking a structured template to help manage and report their finances more effectively, the PDF Document Service offers a valuable resource that aligns with the best practices in financial documentation.

The Form CRI-300 is used for the annual renewal of organizations that have previously filed the Long-Form Initial Registration Statement. Similar to the CRI-200, it requires updates on the charity's activities, but it is specifically for those that have a more complex structure. Both forms help ensure that charities remain compliant with state regulations, but the CRI-300 delves deeper into the organization's ongoing compliance and operational changes since the last registration.

The Form CRI-500 is a financial report required for charities that have received substantial contributions. This form is similar to the CRI-200 in that it collects financial data, but it is specifically designed for larger organizations that may have more complex financial operations. Both forms aim to provide oversight and accountability, ensuring that organizations report their financial activities accurately and transparently to the state.

The Form CRI-100 is a preliminary registration form for charities that are just starting to operate in New Jersey. This document is similar to the CRI-200 in that it requires basic information about the organization, but it is specifically for new entities. Both forms are essential for maintaining compliance with state regulations, ensuring that all charitable organizations, regardless of their stage, are registered and accountable for their fundraising activities.

The Form CRI-150 is the Long-Form Registration Statement for organizations that do not qualify for the Short-Form Registration. This form shares similarities with the CRI-200 in that both require detailed information about the organization’s structure and financial activities. However, the CRI-150 is more comprehensive, designed for larger organizations that must provide extensive disclosures to comply with state laws.

The Form CRI-600 is a report for charities that have had significant changes in their operational status. Similar to the CRI-200, it requires organizations to disclose their current activities and financial standing. Both forms serve as tools for regulatory compliance, ensuring that charities keep the state informed of their operational changes and continue to meet transparency standards.

The Form CRI-700 is a closure form for charities that are ceasing operations. While the CRI-200 focuses on registration and ongoing compliance, the CRI-700 requires organizations to report on their final activities and how remaining assets will be distributed. Both forms are crucial for ensuring that charities operate transparently, but they serve different purposes in the lifecycle of an organization.