Printable New Jersey Cbt 100 Form

Printable New Jersey Cbt 100 Form

| Fact Name | Description |

|---|---|

| Purpose | The CBT-100 form is used by corporations in New Jersey to report their business income and calculate the Corporation Business Tax (CBT). |

| Tax Years | This form applies to taxable years ending on or after July 31, 2010, through June 30, 2011. |

| Filing Requirement | All corporations doing business in New Jersey must file the CBT-100 form, regardless of income level. |

| Governing Law | The CBT-100 form is governed by the New Jersey Statutes Annotated (N.J.S.A.) 54:10A-1 et seq. |

| Net Income Calculation | Corporations must report their entire net income, which includes various income sources, on Schedule A of the form. |

| Tax Credits | The form allows corporations to claim various tax credits, which can reduce their overall tax liability. |

| Due Dates | The CBT-100 is typically due on the 15th day of the fourth month following the end of the corporation's tax year. |

| Signature Requirement | A duly authorized officer of the corporation must sign the form, certifying its accuracy. |

| Payment of Tax | If a corporation owes tax, payment is due with the filing of the CBT-100 form. |

| Record Keeping | Corporations must maintain detailed records supporting the information reported on the CBT-100 for at least four years. |

Nj Boiler License Renewal - All instructions for completing the form must be followed to ensure prompt processing of applications.

Nj Sales Tax Certificate of Authority - Proper completion of the ST-3 form aids in preventing tax disputes between buyers and sellers.

The importance of having a well-prepared Living Will form template cannot be understated, as it provides individuals the opportunity to articulate their medical preferences clearly, ensuring their wishes are honored in critical situations.

New Jersey Employer Taxes - Each seller and purchaser should retain copies for their records and future reference.

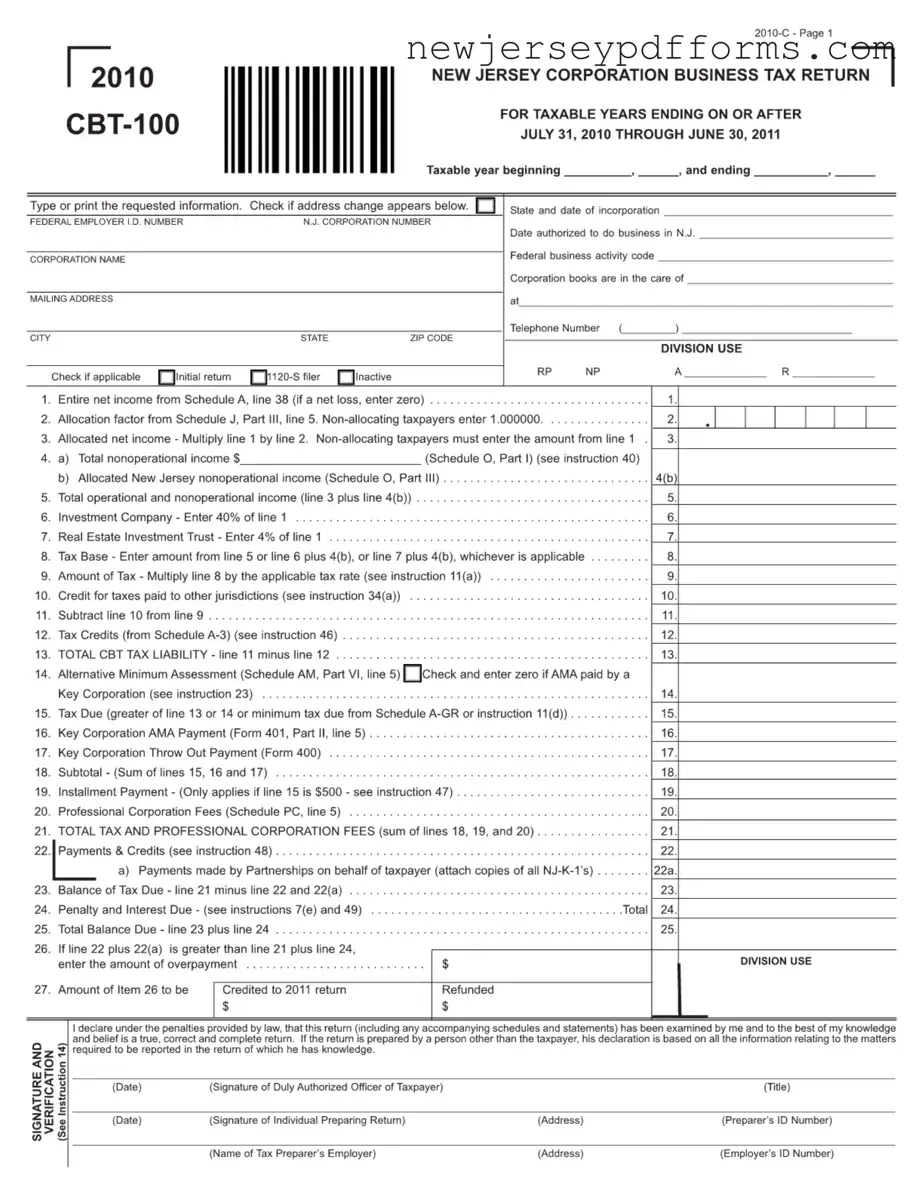

Filling out the New Jersey CBT-100 form can be a straightforward process, but mistakes can happen. One common error is failing to include the correct Federal Employer Identification Number (FEIN). This number is essential for the state to identify your corporation. If it’s missing or incorrect, it can lead to delays or issues with your return.

Another frequent mistake is not checking the box for an address change. If your mailing address has changed, it’s important to mark that box. Not doing so can result in important correspondence going to the wrong address.

People often overlook the need to report entire net income accurately. This figure is crucial for determining your tax liability. If you enter a net loss instead of zero, or if you miscalculate this amount, it can significantly affect your overall tax calculations.

Many filers forget to complete the allocation factor from Schedule J, Part III. This factor is necessary for calculating your allocated net income. If you skip this step, you may end up with an incorrect tax base.

Another mistake is not including all required schedules. For example, if you have nonoperational income, it’s important to fill out Schedule O properly. Failing to do so can lead to an incomplete return.

Some taxpayers miscalculate their tax credits. It’s vital to review the instructions carefully and ensure that all applicable credits are claimed. Missing out on credits can mean paying more tax than necessary.

When reporting the tax due, people sometimes confuse the amounts from different lines. Always double-check that you are using the correct figures from the right lines to avoid any discrepancies.

Lastly, signatures are sometimes forgotten. Both the authorized officer and the preparer need to sign the form. Missing signatures can delay processing and result in additional penalties.

What is the New Jersey CBT-100 form?

The New Jersey CBT-100 form is the Corporation Business Tax Return that corporations doing business in New Jersey must file. It reports the corporation's income, deductions, and tax liability for a specific taxable year. This form is essential for compliance with New Jersey tax laws and is required for corporations incorporated in the state or authorized to do business there.

Who needs to file the CBT-100?

Any corporation that operates in New Jersey or has income sourced from New Jersey must file the CBT-100. This includes traditional corporations, S corporations, and certain other business entities. If your corporation is inactive or has not conducted business, you may still need to file to maintain compliance.

When is the CBT-100 due?

The CBT-100 form is typically due on the 15th day of the fourth month following the end of the corporation's fiscal year. For corporations that follow the calendar year, this means the due date is April 15. It's important to keep track of these deadlines to avoid penalties and interest on late filings.

What information is required on the CBT-100?

The CBT-100 requires various pieces of information, including the corporation's name, federal employer identification number, New Jersey corporation number, and taxable income. You'll also need to provide details on deductions, credits, and any adjustments to income. Accurate reporting is crucial for determining your tax liability.

What if my corporation has a net loss?

If your corporation incurs a net loss for the taxable year, you must still file the CBT-100. You will report the net loss on the appropriate lines, and it can potentially be carried forward to offset future taxable income. However, you cannot claim a tax refund for a net loss; it simply reduces future tax liabilities.

Are there any credits available on the CBT-100?

Yes, the CBT-100 allows corporations to claim various tax credits. These may include credits for taxes paid to other jurisdictions, investment credits, and credits for job creation or retention. Be sure to review the instructions carefully to determine eligibility for these credits and how to claim them.

How do I report income on the CBT-100?

Income is reported on Schedule A of the CBT-100. You'll need to detail your gross receipts, sales, and any deductions such as the cost of goods sold. The total income will be calculated by adding various sources of income, including dividends and royalties. Accurate reporting here is essential for determining your overall tax liability.

What happens if I file the CBT-100 late?

Filing the CBT-100 late can result in penalties and interest on the unpaid tax. The New Jersey Division of Taxation imposes these charges to encourage timely filing. If you anticipate being late, it’s advisable to file for an extension and pay any estimated tax due to minimize penalties.

Where can I find more information or assistance with the CBT-100?

For additional information, you can visit the New Jersey Division of Taxation's website, which provides detailed instructions and resources related to the CBT-100. You may also consider consulting a tax professional who specializes in corporate taxation in New Jersey for personalized assistance.

Misconceptions about the New Jersey CBT-100 form can lead to confusion and potential errors in filing. Here are five common misconceptions, along with explanations to clarify them.

This is not true. All corporations operating in New Jersey, regardless of size, must file the CBT-100 if they are subject to the corporation business tax. This includes small businesses and start-ups.

While both forms are related to corporate taxation, they serve different purposes and have different requirements. The CBT-100 specifically addresses New Jersey's corporation business tax, whereas the federal return is for federal tax obligations.

Even if a corporation has no income or is inactive, it is still required to file the CBT-100. Filing ensures compliance with state regulations and avoids potential penalties.

The CBT-100 requires reporting not just profits but also various types of income, including operational and non-operational income. This comprehensive reporting is essential for accurate tax calculation.

While tax credits can reduce the overall tax liability, they must be claimed correctly on the form. Failing to provide the necessary documentation or complete the required schedules can result in the credits not being applied.

The New Jersey CBT-100 form shares similarities with the IRS Form 1120, which is the U.S. Corporation Income Tax Return. Both forms are designed for corporations to report their income, deductions, and tax liability. Just like the CBT-100, Form 1120 requires detailed financial information, including gross receipts, cost of goods sold, and deductions for various expenses. While the CBT-100 focuses on New Jersey-specific tax obligations, the Form 1120 serves a federal purpose, ensuring that corporations comply with national tax laws. Both forms ultimately help determine the total tax due for the respective jurisdictions.

Another related document is the New Jersey CBT-100S, which is specifically for S corporations. Like the CBT-100, it requires corporations to report their income, deductions, and credits. However, the CBT-100S is tailored for S corporations, which are taxed differently than standard corporations. Both forms require similar types of information, such as gross income and deductions, but the CBT-100S also includes provisions for passing income through to shareholders, reflecting its unique tax structure.

The IRS Form 1065, the U.S. Return of Partnership Income, also has parallels with the CBT-100. Both forms are used to report income and deductions, but while the CBT-100 is for corporations, Form 1065 is specifically for partnerships. Each form requires a comprehensive breakdown of income and expenses, ensuring that the respective entities comply with tax regulations. The key difference lies in the tax treatment; partnerships typically pass income through to partners, while corporations face taxation at the corporate level.

The New Jersey Schedule A, which is part of the CBT-100, is comparable to the IRS Schedule C, used by sole proprietors. Both schedules require detailed reporting of income and expenses related to business activities. Schedule A focuses on the entire net income of the corporation, while Schedule C captures the net profit or loss from a sole proprietorship. Each schedule plays a crucial role in determining the overall tax liability for the respective business entity.

The New Jersey CBT-200 form is another related document, primarily used for corporations with a gross income of less than $100,000. Similar to the CBT-100, the CBT-200 requires corporations to report income and calculate their tax liability. The key distinction is the simplified reporting process for smaller corporations, which can benefit from reduced compliance burdens. Both forms, however, ultimately serve the same purpose of ensuring tax compliance within New Jersey.

As organizations and individuals navigate various legal documents, it's essential to recognize the importance of forms such as the Release of Liability, which safeguards against potential claims. For those interested in understanding and utilizing such templates effectively, resources like the PDF Document Service offer valuable guidance in drafting these essential legal documents.

The IRS Form 990 is relevant for nonprofit organizations and shares some similarities with the CBT-100 in terms of financial reporting. Both forms require organizations to disclose their income, expenses, and financial activities. While the CBT-100 focuses on for-profit corporations, Form 990 is designed for tax-exempt organizations, ensuring transparency and accountability in their financial dealings. Each form aims to provide a clear picture of the organization's financial health to tax authorities.

Lastly, the New Jersey Partnership Return (Form NJ-1065) is akin to the CBT-100 in that it requires partnerships to report their income and expenses. Both forms demand a detailed account of financial activities, but the NJ-1065 is specifically for partnerships, which are taxed differently than corporations. The reporting requirements are similar, as both forms ensure compliance with New Jersey tax laws while addressing the unique tax structures of their respective entities.