Printable New Jersey Estate Tax Return Form

Printable New Jersey Estate Tax Return Form

| Fact Name | Description |

|---|---|

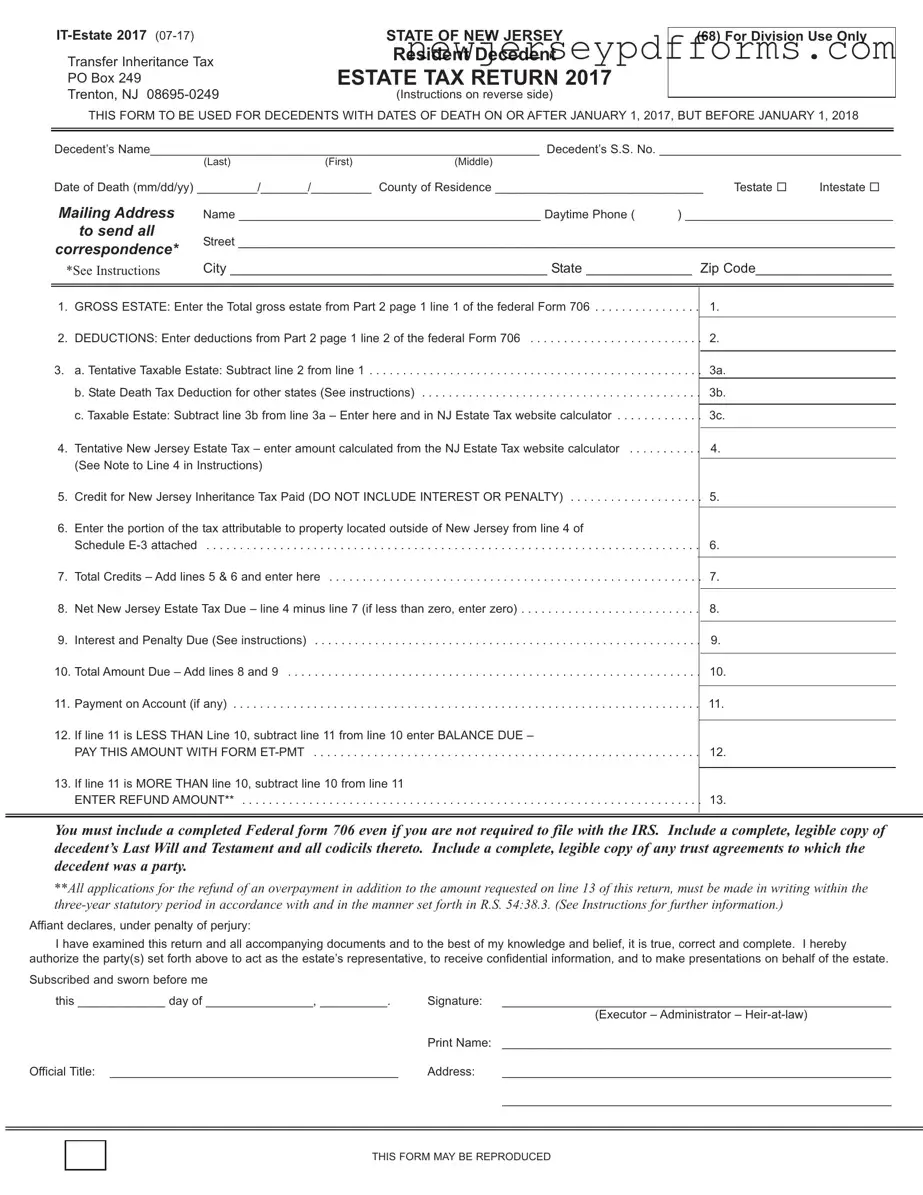

| Form Title | The form is officially known as the New Jersey Estate Tax Return, designated as IT-Estate 2017. |

| Governing Law | The estate tax return is governed by New Jersey Statutes, specifically R.S. 54:38-3. |

| Filing Requirement | Residents must file this return if the decedent's gross estate exceeds $2 million. |

| Documentation Needed | Include a completed Federal Form 706 and a copy of the decedent's Last Will and Testament. |

| Payment Due Date | Payments are due within nine months of the decedent's date of death to avoid interest accrual. |

| Interest Rates | The interest on unpaid taxes accrues at a rate set by the New Jersey Division of Taxation. |

| Amended Returns | If you need to amend the return, clearly mark it as “Amended” at the bottom of the form. |

| Mailing Instructions | Do not use staples or binders; use rubber bands or clips to keep documents together when mailing. |

Child Custody Application Form Nj - If you have questions about court procedures, staff may offer general guidance.

Imm-7 - The Annual Immunization Report plays a key role in public health surveillance in schools.

Understanding the importance of a Living Will is crucial for ensuring your healthcare preferences are honored. By utilizing the California Living Will form, you can clearly state your wishes, providing reassurance for both yourself and your family. For more information, please visit our comprehensive guide to Living Will preparation.

Proof of Service Nj - This form aids in fulfilling legal obligations regarding service of process in family cases.

Filling out the New Jersey Estate Tax Return form can be a daunting task, and mistakes can lead to processing delays or even penalties. One common error is failing to include all required documentation. The form explicitly states that a completed Federal Form 706 must accompany the return, even if you are not required to file with the IRS. Additionally, a legible copy of the decedent’s Last Will and Testament, along with any trust agreements, should be included. Omitting these documents can cause significant delays in processing.

Another frequent mistake involves inaccuracies in the decedent's information. It's crucial to ensure that the name, Social Security Number, and date of death are all correct. Any discrepancies can lead to complications. The estate representative must also verify that the mailing address is accurate, as this is where all correspondence will be sent. If the address is incorrect, important notifications may be missed, which could further complicate the process.

Many individuals overlook the importance of properly categorizing the estate as either testate or intestate. This distinction is vital because it affects how the estate is administered and taxed. If you fail to indicate the correct status, it may lead to processing delays or incorrect tax assessments. Ensuring that this information is clearly marked on the form can save time and hassle down the road.

Lastly, some people forget to sign and notarize the return. This step is essential for validating the document. The representative’s name should be printed clearly beneath the signature to avoid any confusion. A missing signature can halt the entire process, leading to unnecessary delays. By paying attention to these details, you can help ensure a smoother experience when filing the New Jersey Estate Tax Return.

What is the New Jersey Estate Tax Return form and when is it required?

The New Jersey Estate Tax Return form is a document that must be filed by the estate of a deceased person when the gross estate exceeds a certain threshold, which is determined by the state. If the decedent's date of death is on or after January 1, 2017, and before February 1, 2018, the estate must file this return if the gross estate exceeds $2 million. This form is essential for calculating the estate tax owed to the state of New Jersey.

What documents need to be submitted with the New Jersey Estate Tax Return?

When filing the New Jersey Estate Tax Return, several key documents must be included. These include a completed Federal Form 706, a legible copy of the decedent’s Last Will and Testament along with any codicils, and any trust agreements to which the decedent was a party. Additionally, if applicable, the estate representative should provide schedules that request necessary waivers for New Jersey assets. All documents must be clear and properly organized to avoid processing delays.

How should the New Jersey Estate Tax Return be filed to avoid processing delays?

To ensure timely processing of the New Jersey Estate Tax Return, follow specific guidelines. Do not use binders, sealed folders, or staples; instead, secure the return with rubber bands or clips. Include only one copy of all supporting documents, such as the will and trust agreements. Ensure that the return is signed by the legal representative of the estate and that the mailing address is accurate for correspondence. Clearly mark any amended returns as “Amended” and file both the Inheritance and Estate Tax returns together when possible, keeping them separate within the same envelope.

What are the penalties for late filing or payment of the New Jersey Estate Tax?

Late filing or payment of the New Jersey Estate Tax can result in penalties and interest charges. Interest accrues at a rate set by the state, beginning from the date of the decedent's death. If the estate tax return is filed late, the estate may face additional penalties based on the amount owed. It is crucial for the estate representative to adhere to the filing deadlines to avoid these financial repercussions.

Understanding the New Jersey Estate Tax Return can be challenging, and several misconceptions often arise. Here are five common misunderstandings:

Many people believe that only large estates need to file an estate tax return. However, if the gross estate exceeds a certain threshold, filing is mandatory, regardless of the estate's size.

While both taxes are related to the transfer of wealth after death, they are distinct. The estate tax is based on the total value of the estate, whereas the inheritance tax is imposed on the beneficiaries receiving assets.

Even if you are not required to file with the IRS, you must include a completed federal estate tax return, Form 706, with your New Jersey estate tax return. This is crucial for proper processing.

It’s important to follow specific guidelines regarding documentation. Only include necessary documents such as the will, trust agreements, and the federal return. Avoid sending duplicate copies or unnecessary attachments.

Failing to file the estate tax return on time can lead to penalties and interest charges. Timely submission is essential to avoid additional costs and complications.

The New Jersey Estate Tax Return form shares similarities with the Federal Estate Tax Return, Form 706. Both documents serve the purpose of reporting the value of a deceased person's estate and calculating the taxes owed. While the Federal form is used for estates exceeding a certain threshold set by the IRS, the New Jersey form is specific to state tax obligations. Each form requires detailed information about the decedent's assets, liabilities, and deductions. Furthermore, both forms necessitate the inclusion of supporting documents, such as wills and trust agreements, to substantiate the claims made in the returns.

Another document similar to the New Jersey Estate Tax Return is the New Jersey Inheritance Tax Return. While the estate tax applies to the overall value of the estate, the inheritance tax specifically targets the beneficiaries receiving assets from the estate. Both forms require similar information regarding the decedent and the assets involved. The inheritance tax return also requires details about the relationship between the decedent and the beneficiaries, which can affect the tax rate applied. This distinction highlights the different approaches to taxation at the state level, but both documents share the common goal of ensuring compliance with tax obligations.

When navigating the complexities of estate planning, it is essential to consider various legal documents that impact tax liabilities, including the New Jersey Estate Tax Return and the accompanying forms. Notably, a PDF Document Service can provide templates for documents such as the Release of Liability, aiding individuals in understanding their rights and responsibilities. Such resources ensure clarity in legal matters that could influence how estates are managed and taxes are assessed.

The Final Income Tax Return for the decedent is another document that mirrors the New Jersey Estate Tax Return in its purpose of reporting financial information. While the estate tax return focuses on the value of the estate, the final income tax return deals with the decedent's income up to the date of death. Both forms require accurate reporting of income, deductions, and credits. Additionally, they may require similar supporting documentation, such as W-2s and 1099s. Filing both returns is crucial, as they collectively ensure that all financial obligations are met for the decedent's estate.

Lastly, the Trust Tax Return (Form 1041) is comparable to the New Jersey Estate Tax Return in that it deals with the taxation of assets held in a trust. Both documents require detailed information about the trust's income, expenses, and distributions to beneficiaries. While the estate tax return is concerned with the overall estate of the decedent, the trust tax return focuses on the income generated by the trust after the decedent's death. Both forms aim to provide a clear picture of the financial situation of the deceased and ensure that all tax liabilities are addressed appropriately.