Printable Nj 1040 Es Form

Printable Nj 1040 Es Form

| Fact Name | Details |

|---|---|

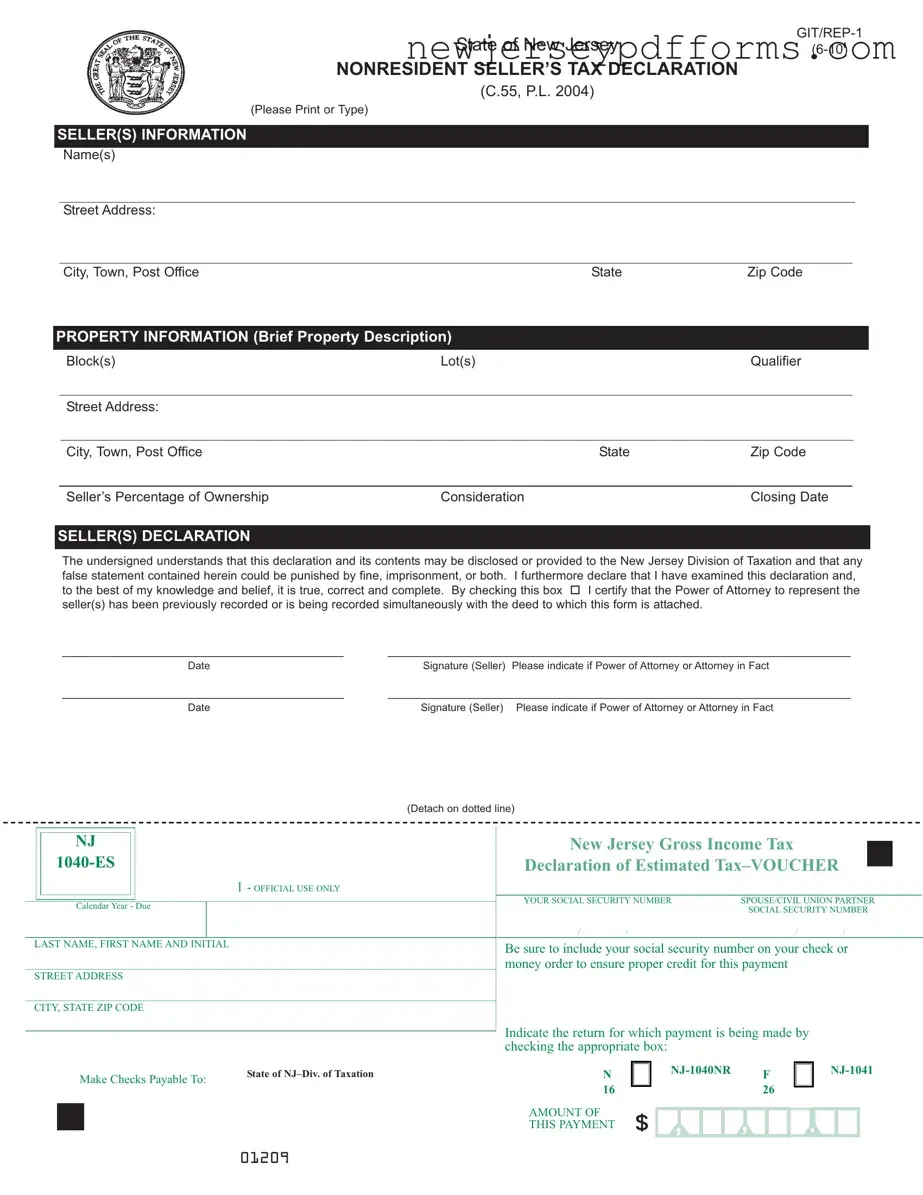

| Purpose | The NJ 1040-ES form is used by nonresident individuals, estates, or trusts selling property in New Jersey to declare and pay estimated Gross Income Tax on the sale. |

| Governing Law | This form is governed by New Jersey law, specifically under C.55, P.L. 2004. |

| Effective Date | The form applies to property sales occurring on or after August 1, 2004. |

| Ownership Declaration | Sellers must declare their percentage of ownership in the property being sold, especially if there are multiple owners. |

| Consideration Definition | Consideration refers to the total amount paid for the property, including any outstanding mortgages or liens associated with the sale. |

| Signature Requirement | The form must be signed and dated by the seller(s). If a representative signs, proper authority must be documented. |

| Payment Method | Payments should be made via check or money order, payable to the State of New Jersey - Division of Taxation. Cash is not accepted. |

| Submission Process | The completed form and payment must be submitted at closing, and the buyer's attorney must file it with the county clerk when recording the deed. |

New Jersey Medicaid Expansion - It aims to assist applicants in ensuring all pertinent information is reported accurately.

The Sample Tax Return Transcript is not only important for understanding one's financial history but can also be a valuable resource for anyone looking to gain insights into their tax situation. By utilizing services such as PDF Document Service, individuals can efficiently access and manage their tax documentation, ensuring they are well-prepared for any financial assessments.

New Jersey Employer Taxes - This form comprises a crucial part of the asset sale closing process in New Jersey.

Nj Annulment Forms Pdf - All financial contributions toward the bail must be accounted for.

Filling out the NJ 1040-ES form can be a daunting task, especially for those unfamiliar with the process. One common mistake is failing to include the social security number of the seller. This number is crucial for ensuring that the payment is properly credited. Without it, delays may occur, leading to complications in the recording of the deed.

Another frequent error is using the address of the property being sold instead of the seller's primary residence. The form requires the seller's current address, which should reflect where they live or conduct business. This detail is important for accurate identification and communication.

Many people overlook the percentage of ownership section, especially when multiple owners are involved. It is essential to indicate each seller's portion of ownership. Failing to do so can lead to misunderstandings regarding the distribution of proceeds and tax liabilities.

Additionally, some individuals mistakenly leave out the consideration amount, which represents the total compensation for the property. This figure should include not just cash, but also any other valuable items exchanged during the sale. Omitting this information can result in incorrect tax calculations.

Signature requirements are often misunderstood as well. Sellers must sign and date the declaration, and if a representative is signing on their behalf, proper documentation, such as a Power of Attorney, must be attached. Neglecting this step can invalidate the declaration and delay the process.

Another common oversight is not checking the appropriate box to indicate which return the payment is for. This detail, while seemingly minor, is critical for the tax authorities to correctly process the payment. Failure to do this may lead to confusion and potential penalties.

Some individuals also forget to make the payment in the correct form. Payments must be made via check or money order, as cash is not accepted. Ensuring the payment method aligns with the requirements is essential to avoid complications.

Moreover, it is vital to remember that the NJ 1040-ES must be completed in its entirety. Incomplete forms will not be processed, and the deed may not be recorded. This can create significant delays and additional stress during what is already a challenging time.

Lastly, failing to submit the NJ 1040-ES along with the required documentation at the time of closing can lead to serious consequences. This form, along with the Seller's Residency Certification or Tax Prepayment Receipt, must be presented to the buyer or their attorney. Missing these documents can result in the deed not being recorded, causing further complications for all parties involved.

What is the NJ 1040-ES form?

The NJ 1040-ES form is a declaration of estimated tax for nonresident individuals, estates, or trusts selling property in New Jersey. This form is required for sales occurring on or after August 1, 2004, and it helps ensure that the appropriate taxes are paid on any gains from the sale of real estate.

Who needs to complete the NJ 1040-ES form?

Nonresident sellers, including individuals, estates, and trusts, must complete the NJ 1040-ES form when selling property in New Jersey. If there are multiple owners, separate forms are required for each seller, except for spouses or civil union partners who file jointly.

What information is required on the NJ 1040-ES form?

Key information includes the seller's name, address, property details (block, lot, and address), percentage of ownership, consideration (total compensation for the property), and the closing date. The seller must also provide their social security number or federal tax identification number.

How is the tax payment calculated on the NJ 1040-ES form?

Tax payment is calculated by multiplying the gain from the sale by the highest Gross Income Tax rate of 8.97%. However, the payment cannot be less than 2% of the total consideration received for the property. It’s important to determine the gain without considering any distributions made to beneficiaries by estates or trusts during the taxable year.

What happens if the NJ 1040-ES form is not completed correctly?

Failure to complete the NJ 1040-ES form in its entirety will result in the deed not being recorded. It's essential to provide all requested information accurately to avoid delays in the transaction.

When should the NJ 1040-ES form be submitted?

The NJ 1040-ES form must be completed at the time of closing. It should be given to the buyer or the buyer's attorney, who will then submit it to the county clerk when recording the deed.

What if I have a Power of Attorney?

If a representative is signing the NJ 1040-ES form on behalf of the seller, a Power of Attorney must be recorded prior to or simultaneously with the deed. Alternatively, a signed letter from the seller granting authority to the representative must accompany the form.

What should I do if the total consideration for the property is $1,000 or less?

If the total consideration for the property is $1,000 or less, you should complete the Seller’s Residency Certification/Exemption form GIT/REP-3 and check the appropriate box under Seller’s Assurances on the NJ 1040-ES form.

Where do I send the NJ 1040-ES form and payment?

The completed NJ 1040-ES form, along with the payment, should be forwarded by the County Clerk to the State of New Jersey, Revenue Processing Center, PO Box 222, Trenton, New Jersey 08646-0222. Ensure that the payment is made by check or money order, as cash is not accepted.

Misconceptions about the NJ 1040 ES form can lead to confusion and mistakes during the property selling process. Here are seven common misunderstandings:

Understanding these misconceptions can help ensure a smoother transaction when selling property in New Jersey.

The NJ-1040-ES form is similar to the IRS Form 1040-ES, which is used by individuals to estimate their federal income tax payments. Both forms require taxpayers to project their income and calculate the tax owed for the year. Just like the NJ-1040-ES, the IRS Form 1040-ES includes a payment voucher that must be submitted with the payment. Each form serves as a means for taxpayers to avoid underpayment penalties by making timely estimated payments based on their projected income.

Another document that bears similarities to the NJ-1040-ES is the New Jersey GIT/REP-3 form, which is the Seller’s Residency Certification/Exemption form. This form is utilized when the total consideration for the property is $1,000 or less. Both forms are specifically designed for real estate transactions in New Jersey and require the seller to provide information about the property and the sale. The GIT/REP-3 form also includes assurances that help clarify the seller's residency status, akin to the declarations made in the NJ-1040-ES.

The New Jersey NJ-1040 form is another document that shares commonalities with the NJ-1040-ES. The NJ-1040 is the standard income tax return for New Jersey residents. While the NJ-1040-ES focuses on estimated payments for nonresident sellers, the NJ-1040 requires comprehensive income reporting for residents. Both forms require the inclusion of personal identification information, such as Social Security numbers, and both are essential for compliance with New Jersey tax laws.

Form W-9 is also comparable to the NJ-1040-ES in that it is used to provide taxpayer identification information. While the W-9 is primarily for independent contractors and freelancers to report their taxpayer identification number to clients, it serves a similar purpose of ensuring accurate identification for tax purposes. Both forms are crucial in the context of tax compliance and reporting, requiring accurate and complete information to avoid potential penalties.

Additionally, the IRS Form 1099-S is relevant as it pertains to the reporting of proceeds from real estate transactions. Like the NJ-1040-ES, the Form 1099-S is used in the context of real estate sales and includes details about the seller and the sale. Both forms ensure that the appropriate tax is reported and paid on the proceeds from property sales, reflecting the connection between federal and state tax obligations.

The New Jersey NJ-1041 form, which is the income tax return for estates and trusts, is similar to the NJ-1040-ES in that both forms deal with tax obligations related to property transactions. The NJ-1041 requires estates and trusts to report income, deductions, and credits, while the NJ-1040-ES focuses on estimated tax payments for nonresident sellers. Both documents are essential for ensuring that tax liabilities are met in accordance with New Jersey tax law.

The IRS Form 4562, which is used to claim depreciation and amortization, can also be likened to the NJ-1040-ES. Both forms involve financial transactions that may impact tax obligations. While the Form 4562 is focused on business assets and their depreciation, the NJ-1040-ES addresses tax liabilities arising from the sale of real estate. Both require detailed financial information to ensure compliance with tax laws.

Form 1040-X, the amended U.S. individual income tax return, is relevant as it allows taxpayers to correct errors on previously filed returns. This form shares a connection with the NJ-1040-ES in that both deal with tax obligations and the need for accurate reporting. If a seller realizes an error in their reported sale on the NJ-1040-ES, they may need to file an amended return similar to the 1040-X to rectify the situation.

The New Jersey Property Tax Reimbursement Application, also known as the Senior Freeze Application, is another document that has similarities with the NJ-1040-ES. Both forms require detailed information about property ownership and financial status. The Senior Freeze Application is aimed at providing property tax relief to eligible seniors, while the NJ-1040-ES addresses tax obligations for nonresident sellers. Both documents are crucial for managing tax liabilities in New Jersey.

Lastly, the New Jersey Tax Payment Voucher (Form NJ-1040-V) serves a similar purpose to the NJ-1040-ES. This voucher is used by taxpayers to submit payments for their New Jersey income tax liabilities. Both forms require the taxpayer to provide identification information and payment details, ensuring that payments are properly credited to the taxpayer’s account. They both facilitate compliance with New Jersey tax regulations and help avoid penalties for late payments.