Printable Nj 1040Nr Form

Printable Nj 1040Nr Form

| Fact Name | Details |

|---|---|

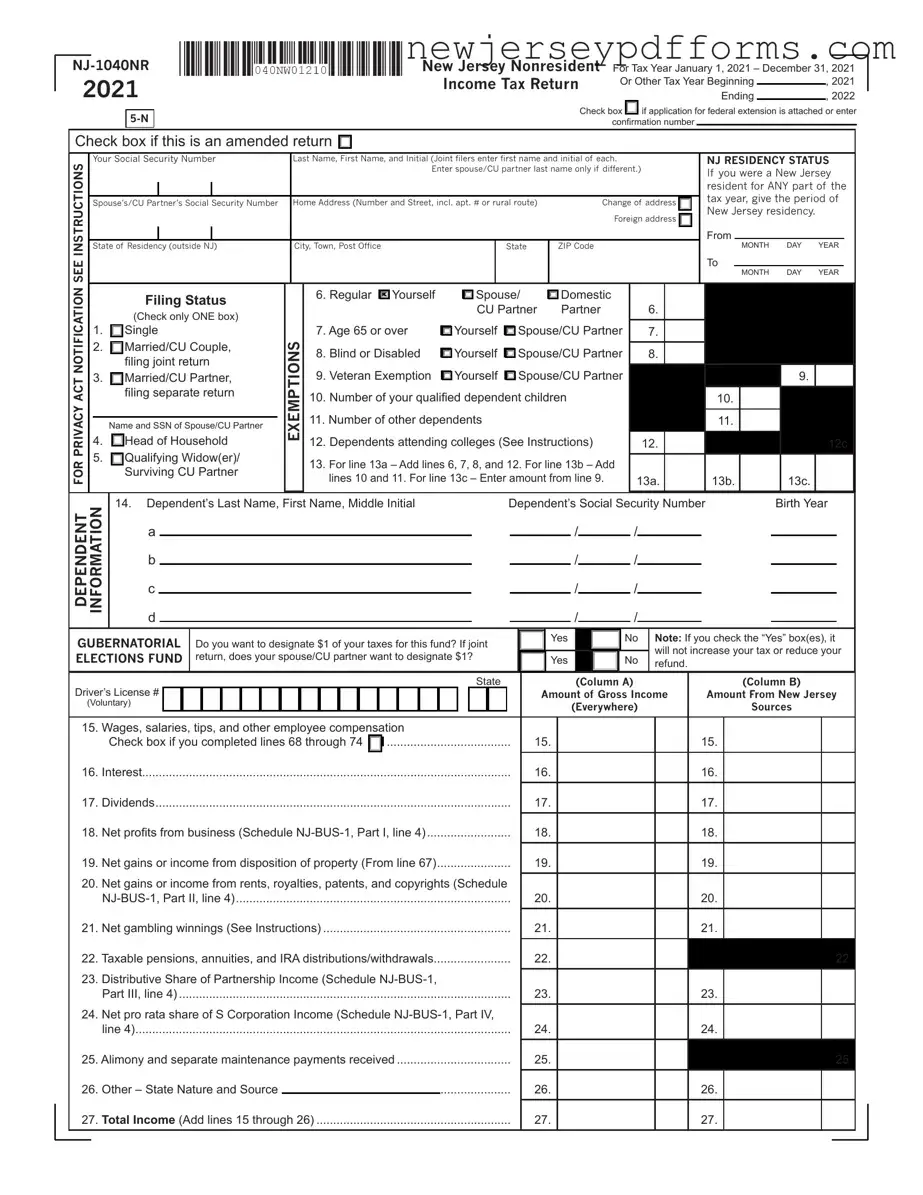

| Purpose | The NJ-1040NR form is used for filing New Jersey income tax returns by nonresidents for the tax year 2021. |

| Eligibility | This form is specifically for individuals who earned income in New Jersey but were not residents of the state during the tax year. |

| Filing Deadline | The deadline to file the NJ-1040NR is typically April 15 of the year following the tax year, unless an extension is requested. |

| Governing Law | The NJ-1040NR is governed by the New Jersey Division of Taxation regulations under the New Jersey Gross Income Tax Act. |

| Income Reporting | Taxpayers must report all income earned from New Jersey sources, including wages, dividends, and business income. |

| Exemptions and Deductions | Taxpayers can claim various exemptions and deductions, such as those for dependents, medical expenses, and retirement income. |

| Tax Calculation | The tax owed is calculated based on the taxable income after applying deductions and exemptions, following the tax table provided by the state. |

Nj Tax Forms 2023 - The form provides a section for reporting tax withheld from wages to ensure accurate tax payments.

To streamline the application process, using a template can be highly beneficial, and one such resource is the PDF Document Service, which provides a easily accessible format for landlords and tenants alike.

Njdep Site Remediation - Include all known details about the well for a thorough search.

Universal Physical Form - Physicians must disclose any other names they have used and their associated years.

Filling out the NJ-1040NR form can be a complex task, and many individuals make mistakes that could affect their tax obligations. One common error is failing to report all sources of income. It is essential to include every source of income earned, both within and outside of New Jersey. Missing income can lead to penalties or a larger tax bill later on.

Another frequent mistake is incorrect residency status. Taxpayers must accurately indicate their residency status for the entire tax year. If someone lived in New Jersey for part of the year, they need to specify the exact dates of residency. Misreporting this information can result in incorrect tax calculations and potential audits.

Many filers also overlook the importance of claiming eligible exemptions and deductions. For instance, taxpayers may not realize they qualify for certain deductions related to medical expenses or alimony payments. Not taking full advantage of these opportunities can lead to a higher taxable income than necessary.

Additionally, individuals often make errors in basic personal information, such as Social Security numbers or names. These mistakes can delay processing or lead to complications with the IRS. Double-checking this information before submission is crucial to avoid unnecessary issues.

Finally, failing to sign the form or include necessary attachments is a common oversight. A missing signature can render the return invalid, and not including required documents may lead to processing delays. Ensuring that all sections are complete and all required attachments are included is vital for a smooth filing experience.

What is the NJ-1040NR form?

The NJ-1040NR form is the New Jersey Nonresident Income Tax Return. It is used by individuals who earned income in New Jersey but are not residents of the state. This form allows nonresidents to report their income and calculate their tax liability for the tax year.

Who needs to file the NJ-1040NR?

What is the tax year for the NJ-1040NR?

The NJ-1040NR form for the tax year 2021 covers income earned from January 1, 2021, to December 31, 2021. Taxpayers must report their income for this specific period when filing the form.

How do I determine my residency status for the NJ-1040NR?

What types of income should I report on the NJ-1040NR?

Are there any exemptions or deductions available on the NJ-1040NR?

What if I owe taxes after filing the NJ-1040NR?

How can I check the status of my NJ-1040NR refund?

What should I do if I made an error on my NJ-1040NR?

Understanding the NJ-1040NR form can be challenging, and several misconceptions can lead to confusion. Here are seven common misunderstandings about this tax form:

Being aware of these misconceptions can help ensure that you file your taxes correctly and avoid unnecessary penalties or complications. Always consider consulting a tax professional if you have questions about your specific situation.

The NJ-1040NR form shares similarities with the IRS Form 1040NR, which is the U.S. Nonresident Alien Income Tax Return. Both forms are designed for individuals who are not residents of the state or country but still have income sourced from there. The NJ-1040NR specifically addresses New Jersey tax obligations, while the IRS Form 1040NR handles federal tax liabilities. Each form requires detailed reporting of income, deductions, and credits applicable to nonresidents, ensuring that the taxpayer complies with the respective tax laws of New Jersey and the federal government.

Another document that parallels the NJ-1040NR is the New Jersey Resident Income Tax Return, known as the NJ-1040. While the NJ-1040 is for full-year residents, it shares structural elements with the NJ-1040NR, such as sections for income reporting, deductions, and exemptions. Both forms require taxpayers to disclose personal information, including Social Security numbers and residency status. The primary distinction lies in residency classification, with the NJ-1040NR catering to those who earn income in New Jersey but reside elsewhere.

The NJ-1040NR also resembles the IRS Form 8862, which is used to claim the Earned Income Credit after disallowance. Both forms require documentation of income and exemptions, though their purposes differ. The NJ-1040NR focuses on state income tax obligations, while Form 8862 is specifically aimed at federal tax credits. Each document necessitates careful attention to detail and accuracy to ensure compliance with tax regulations and to maximize potential credits or refunds.

Lastly, the NJ-1040NR has similarities with the New Jersey Corporation Business Tax Return, known as the CBT-100. Both forms are used to report income generated within New Jersey, although the NJ-1040NR pertains to individual nonresidents, while the CBT-100 is for corporations. Each form requires a breakdown of income sources and applicable deductions. They both aim to ensure that all entities, whether individuals or corporations, fulfill their tax responsibilities to the state of New Jersey based on the income earned within its borders.