Printable Nj 1065 Schedule A Form

Printable Nj 1065 Schedule A Form

| Fact Name | Fact Description |

|---|---|

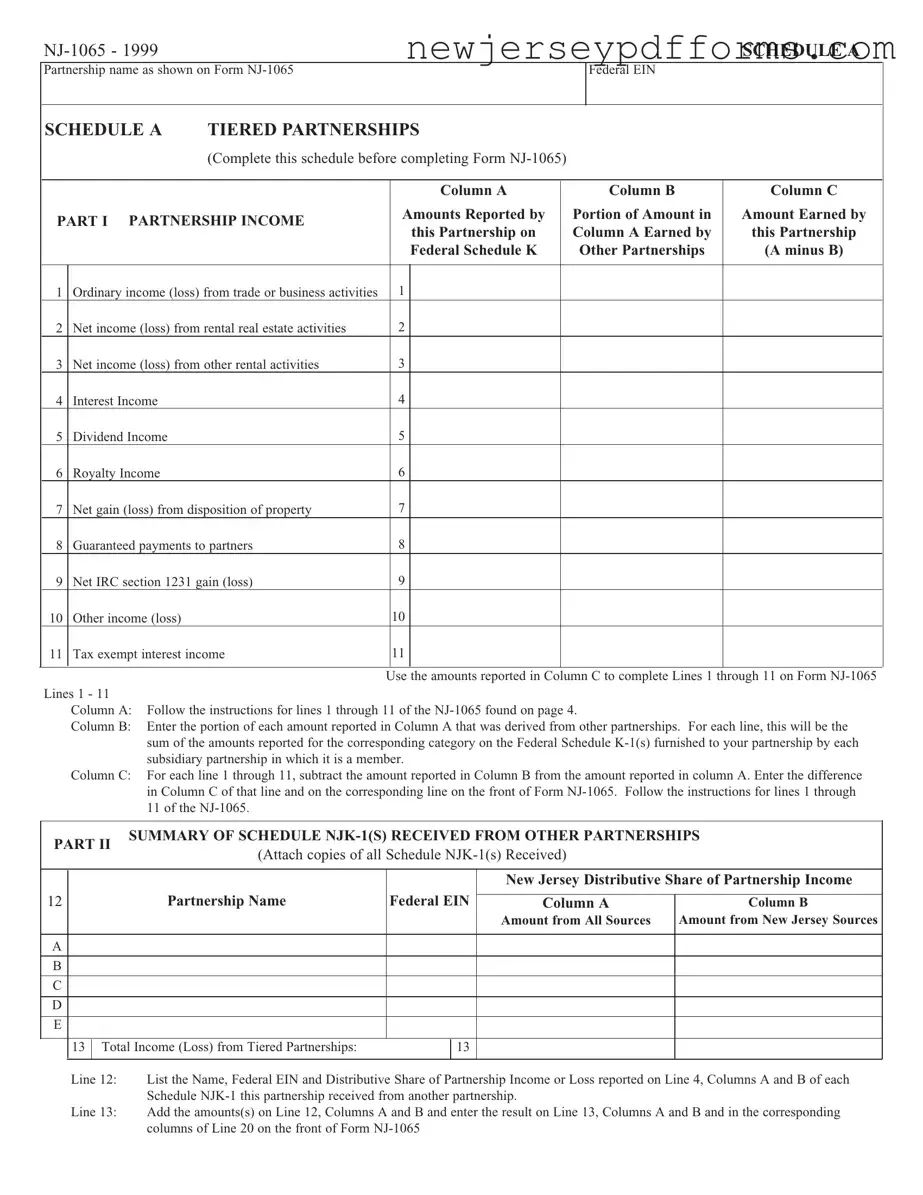

| Form Purpose | The NJ 1065 Schedule A is used by partnerships to report income and losses from tiered partnerships in New Jersey. |

| Governing Law | This form is governed by New Jersey tax law, specifically the New Jersey Division of Taxation regulations. |

| Partnership Information | Partnerships must provide their name and Federal Employer Identification Number (EIN) on the form. |

| Income Categories | Schedule A includes various income categories such as ordinary income, rental income, interest, dividends, and royalties. |

| Column A Reporting | Column A requires partnerships to report the total amounts earned as indicated on the Federal Schedule K. |

| Column B Reporting | In Column B, partnerships must enter the portion of each amount reported in Column A that comes from other partnerships. |

| Column C Calculation | Column C is calculated by subtracting the amount in Column B from Column A for each income category. |

| Schedule NJK-1 Requirement | Partnerships must attach copies of all Schedule NJK-1(s) received from other partnerships to complete this schedule. |

Nj Milk License - A Federal Tax ID or Social Security Number must be included with the application.

New Jersey D 3 - Participants in the electoral process must prioritize timely and accurate submissions.

When filling out the NJ 1065 Schedule A form, many people make common mistakes that can lead to errors in their tax filings. Understanding these pitfalls can help ensure accuracy and avoid potential issues with the New Jersey Division of Taxation.

One frequent mistake is failing to accurately report the partnership name and Federal EIN as shown on Form NJ-1065. This information is crucial for identifying the partnership correctly. If this information is incorrect, it can cause delays or complications in processing the tax return.

Another common error occurs in Column B, where individuals often miscalculate the portion of amounts reported that were derived from other partnerships. This column requires careful attention to detail. If the figures are not accurately summed from the Federal Schedule K-1(s), it can lead to significant discrepancies in the final amounts reported.

Many filers also overlook the importance of Column C, which requires subtracting the amount in Column B from Column A. This calculation is essential for determining the correct income earned by the partnership. Failing to perform this step or making errors in the arithmetic can result in reporting incorrect income figures.

Additionally, some people neglect to attach copies of all Schedule NJK-1(s) received from other partnerships. This documentation is necessary for validating the income reported. Without these attachments, the tax return may be considered incomplete, leading to potential audits or requests for further information.

Another mistake involves not following the specific instructions for lines 1 through 11 on the NJ-1065. Each line corresponds to different types of income or losses, and misunderstanding these categories can lead to misreporting. It’s important to carefully read and follow the guidelines provided.

Some individuals also fail to double-check their total income or loss from tiered partnerships. This total must be accurately calculated and reported on Line 13. Errors in this calculation can significantly impact the overall tax liability of the partnership.

Finally, a lack of attention to detail can lead to typographical errors or omissions, which can complicate the filing process. Simple mistakes, such as incorrect numerical entries or missing information, can lead to delays or rejections of the tax return. Taking the time to review the form thoroughly can help mitigate these issues.

By being aware of these common mistakes, individuals can better prepare their NJ 1065 Schedule A forms, ensuring a smoother filing process and reducing the risk of complications down the road.

What is the NJ 1065 Schedule A form used for?

The NJ 1065 Schedule A form is used by partnerships in New Jersey to report income and losses from various sources. This form details the partnership's income earned from trade or business activities, rental activities, interest, dividends, royalties, and other income. It is essential for partnerships that receive income from other partnerships, as it helps in calculating the distributive share of partnership income or loss.

How do I fill out the columns on Schedule A?

Schedule A consists of three columns: Column A, Column B, and Column C. In Column A, report the total amounts of income or loss from various activities as shown on the Federal Schedule K. Column B should reflect the portion of each amount that comes from other partnerships. This information is gathered from the Schedule K-1(s) provided by subsidiary partnerships. Finally, in Column C, subtract the amount in Column B from Column A to determine the income or loss earned directly by your partnership.

What should I do with the NJK-1(s) received from other partnerships?

When you receive NJK-1(s) from other partnerships, it is crucial to attach copies of these schedules to your NJ 1065 Schedule A. These documents provide details about your partnership's distributive share of income or loss from the tiered partnerships. Make sure to list the name and Federal EIN of each partnership, along with the total income or loss from both all sources and New Jersey sources, as required on the form.

How does Schedule A affect my overall NJ-1065 filing?

The information you report on Schedule A is directly used to complete the NJ-1065 form. The amounts calculated in Column C of Schedule A will be transferred to the corresponding lines on the front of the NJ-1065. This ensures that your partnership's income and losses are accurately reflected in your overall tax filing, impacting your tax obligations in New Jersey.

Misconceptions about the NJ 1065 Schedule A form can lead to confusion and errors in reporting partnership income. Here are ten common misunderstandings:

Understanding these misconceptions can help ensure accurate reporting and compliance with New Jersey tax laws.

The NJ-1065 Schedule A form is similar to the IRS Form 1065. Both documents serve to report the income, deductions, gains, and losses of a partnership. While the NJ-1065 Schedule A focuses on New Jersey-specific regulations and income derived from partnerships, the IRS Form 1065 is a federal form used to report the same types of financial information to the Internal Revenue Service. Both forms require detailed breakdowns of income sources and distributions to partners, ensuring that both state and federal authorities have accurate information regarding partnership earnings.

Another similar document is the IRS Schedule K-1 (Form 1065). This form is used to report each partner's share of the partnership's income, deductions, and credits. Just like the NJ-1065 Schedule A, the K-1 provides a breakdown of the income earned by the partnership and how it is distributed among partners. The K-1 is essential for partners to accurately report their individual income on their tax returns, reflecting the partnership's financial activities.

The NJ 1065 Schedule A form, while primarily focused on partnership income, has implications for those also seeking rental properties. For individuals navigating the rental application process, utilizing resources like the PDF Document Service can streamline the preparation of necessary documents, ensuring that all pertinent information is accurately recorded. This parallel highlights the importance of thorough documentation whether applying for rental properties or reporting income for partnerships.

The New Jersey Partnership Return (Form NJ-1065) itself is closely related to the Schedule A. This form is the primary document used to report the overall financial status of the partnership to the state. While the Schedule A provides specific details about tiered partnerships and income distributions, the NJ-1065 encompasses the entire partnership's financial picture, including total income, deductions, and tax liability calculations.

Form NJ-K-1 is another document that aligns with the NJ-1065 Schedule A. This form is issued to each partner by the partnership and reports the partner's share of income, deductions, and credits from the partnership. Similar to the IRS K-1, the NJ-K-1 is crucial for partners to report their earnings to the New Jersey Division of Taxation. The NJ-K-1 ensures that each partner can accurately reflect their share of partnership income on their personal tax returns.

The IRS Form 1120-S, while primarily for S Corporations, shares similarities with the NJ-1065 Schedule A in how it reports income and distributions to shareholders. Both forms require detailed reporting of income sources and distributions, although the NJ-1065 focuses on partnerships specifically. This similarity in structure helps ensure that both types of entities provide clear and comprehensive financial information to tax authorities.

The New Jersey Corporation Business Tax Return (Form CBT-100) is another relevant document. While it is designed for corporations rather than partnerships, it shares a common goal of reporting income and tax liabilities to the state. Like the NJ-1065 Schedule A, the CBT-100 requires detailed reporting of income sources, deductions, and tax calculations, ensuring transparency in financial reporting for both partnerships and corporations.

Lastly, the IRS Form 990 is relevant for tax-exempt organizations and shares a commonality with the NJ-1065 Schedule A in that both require detailed financial reporting. Although the Form 990 is for non-profit organizations, it still demands a breakdown of income sources and expenditures. This level of detail is essential for maintaining transparency and accountability in financial reporting, which is a principle upheld by both forms.