Printable Nj 1065 Schedule Njk 1 Form

Printable Nj 1065 Schedule Njk 1 Form

| Fact Name | Description |

|---|---|

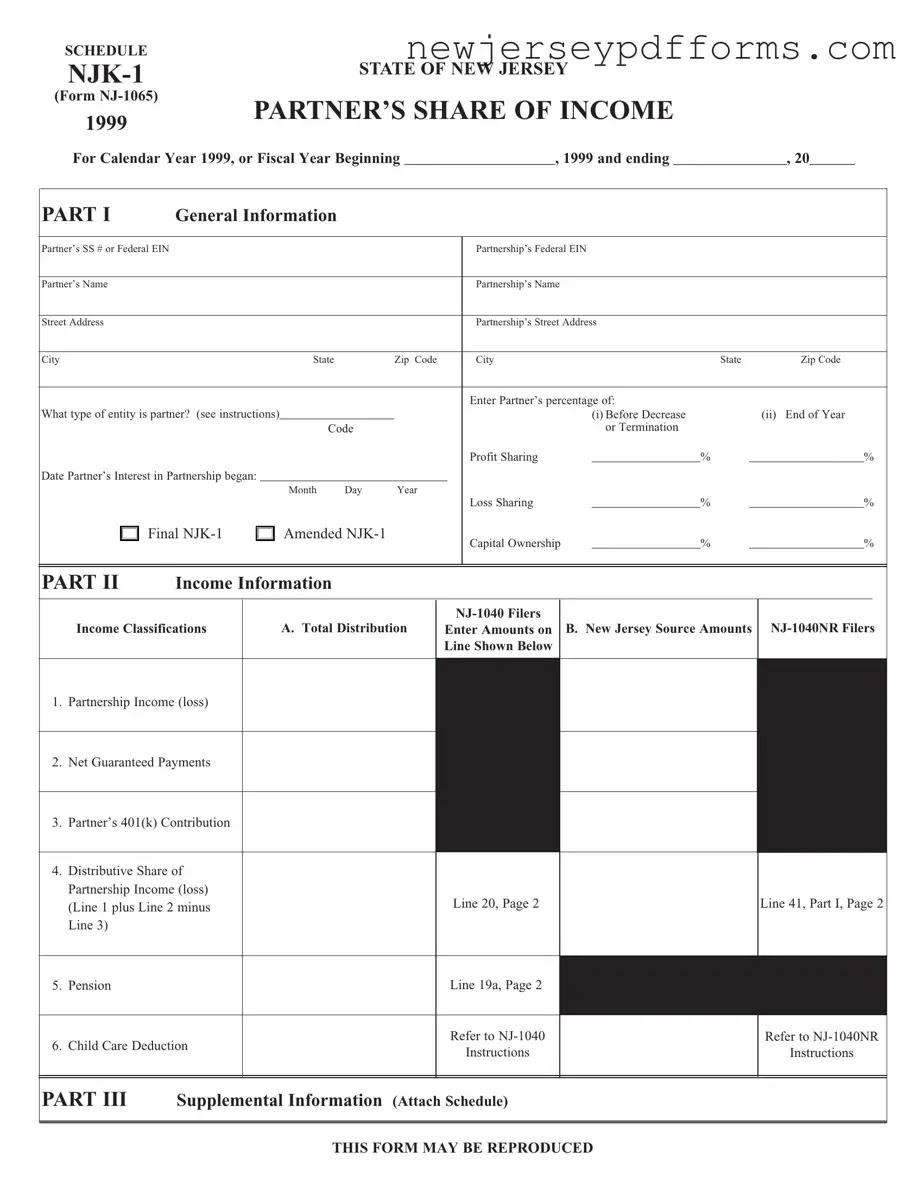

| Form Purpose | The NJK-1 form reports a partner's share of income from a partnership for tax purposes. |

| Governing Law | This form is governed by New Jersey tax laws, specifically the New Jersey Division of Taxation regulations. |

| Filing Requirement | Partners must receive a NJK-1 form if they are part of a partnership that generates income. |

| Information Included | The form includes details such as the partner’s SSN or EIN, partnership information, and income classifications. |

| Amendments | Partners can file an amended NJK-1 if corrections are needed after the initial submission. |

| Distribution Reporting | Partners must report their share of partnership income, guaranteed payments, and other distributions on the form. |

Nj Annulment Forms Pdf - The form requests previous employment details to assess financial stability.

Obtaining a Sample Tax Return Transcript can be made easier through resources like PDF Document Service, which provides guidance on how to access and utilize this important document effectively for various financial needs.

B6T Nj - Ensure the application is filled out completely for proper processing.

Filling out the NJ 1065 Schedule NJK-1 form can be a daunting task, and many people make mistakes that can lead to delays or complications. One common error is failing to provide accurate personal information. It is crucial to ensure that the partner's Social Security number or Federal Employer Identification Number (EIN) is correct. A simple typo can cause significant issues in processing the form.

Another frequent mistake involves not clearly indicating the type of entity for the partner. Each type of entity has different implications for tax purposes. Neglecting to specify this can lead to confusion and potential misclassification. Additionally, some individuals forget to include the partner's percentage of profit and loss sharing, which is essential for determining each partner's share of the partnership's income.

Many filers overlook the importance of accurately reporting the dates related to the partner's interest in the partnership. This includes the start date of their interest, which must be filled out correctly to avoid discrepancies. Furthermore, people sometimes fail to check whether they are submitting a final or amended NJK-1. Marking the wrong option can lead to unnecessary complications.

In the income information section, it is vital to ensure that all amounts are entered correctly. For instance, some individuals miscalculate the partnership income or guaranteed payments. This can significantly affect the overall tax liability. It's also important to remember to include the distributive share of partnership income accurately, as this is a key figure for tax reporting.

Another mistake is neglecting to attach the necessary supplemental information or schedules that may be required. Failing to provide this documentation can result in delays or rejections of the form. Lastly, many people do not review the form before submission. Taking a moment to double-check all entries can prevent many of these common errors and ensure that the form is processed smoothly.

What is the NJ 1065 Schedule NJK-1 form used for?

The NJ 1065 Schedule NJK-1 form is used to report a partner's share of income, deductions, and credits from a partnership in New Jersey. This form is essential for both the partnership and the individual partners, as it provides the necessary information for partners to accurately file their state income tax returns. It details the financial performance of the partnership and the individual partner's share of that performance for the specified tax year.

Who needs to file the NJ 1065 Schedule NJK-1 form?

What information is included on the NJ 1065 Schedule NJK-1 form?

The NJK-1 form includes several key pieces of information. It provides the partner's Social Security number or Federal Employer Identification Number, the partnership's Federal EIN, and the names and addresses of both the partner and the partnership. Additionally, it details the partner's percentage of profit, loss, and capital ownership, as well as specific income classifications such as partnership income, net guaranteed payments, and distributive shares of income or loss.

How do I report the information from the NJK-1 on my tax return?

When filing your New Jersey tax return, you will need to report the information from the NJK-1 form on your NJ-1040 or NJ-1040NR. Each income classification listed on the NJK-1 should be entered in the corresponding sections of your tax return. Be sure to follow the instructions provided for the NJ-1040 or NJ-1040NR to ensure accurate reporting and compliance with state tax laws.

Can the NJ 1065 Schedule NJK-1 form be amended?

Yes, the NJK-1 form can be amended if there are changes to the partnership's financial information or if errors are discovered after the initial filing. If you need to amend a NJK-1, you should check the box indicating that it is an amended NJK-1 and provide the corrected information. It’s important to ensure that all partners receive updated forms to reflect any changes, as this will affect their individual tax filings.

Misconceptions about the NJ 1065 Schedule NJK-1 form can lead to confusion and errors in tax reporting. Understanding the truth behind these misconceptions is essential for accurate compliance. Below are eight common misconceptions, along with explanations to clarify each point.

Addressing these misconceptions can help ensure that partnerships and their partners navigate the complexities of tax reporting more effectively. Accurate information is vital for compliance and for making informed decisions regarding tax obligations.

The NJ 1065 Schedule NJK-1 form is similar to the IRS Form K-1, which is used for reporting income, deductions, and credits from partnerships. Both forms provide a detailed breakdown of a partner’s share of income, losses, and other tax-related information. The IRS Form K-1 is essential for federal tax purposes, while the NJK-1 serves a similar function for state tax filings in New Jersey. Each form includes sections for identifying the partner and the partnership, as well as specific income classifications that need to be reported by the partner on their individual tax returns.

Another document comparable to the NJK-1 is the Schedule E (Form 1040), which is used by individual taxpayers to report income or loss from partnerships, S corporations, estates, trusts, and real estate. Like the NJK-1, Schedule E requires detailed reporting of income and losses associated with partnerships. The information from the NJK-1 is often transferred to Schedule E to ensure that partners accurately report their earnings on their federal tax returns. This connection underscores the importance of both forms in providing a comprehensive view of a partner’s financial involvement in a partnership.

The Form 1065, U.S. Return of Partnership Income, is also similar to the NJK-1. This federal form is filed by partnerships to report their income, deductions, gains, and losses. The information provided on Form 1065 directly impacts the NJK-1, as the partnership must first complete this form to determine how much income or loss each partner will receive. Essentially, the NJK-1 acts as a pass-through document that conveys the results of the Form 1065 to individual partners, ensuring they have the necessary information to file their own tax returns accurately.

Additionally, the New Jersey Division of Taxation’s NJ-1040 form bears similarities to the NJK-1. The NJ-1040 is the individual income tax return for residents of New Jersey, where taxpayers report their income, deductions, and credits. Information from the NJK-1 is used to fill out the NJ-1040, particularly in reporting partnership income. This relationship highlights how the NJK-1 serves as a critical link between partnership income reporting and individual tax obligations in New Jersey.

Lastly, the NJ-1040NR form, which is the non-resident income tax return for New Jersey, is also akin to the NJK-1. Non-residents who receive income from New Jersey partnerships must report this income on the NJ-1040NR. The NJK-1 provides essential details about the income earned from the partnership, which must be accurately reported on the non-resident tax return. This ensures that non-resident partners fulfill their tax responsibilities while also benefiting from the information provided in the NJK-1.