Printable Nj 1065E Form

Printable Nj 1065E Form

| Fact Name | Details |

|---|---|

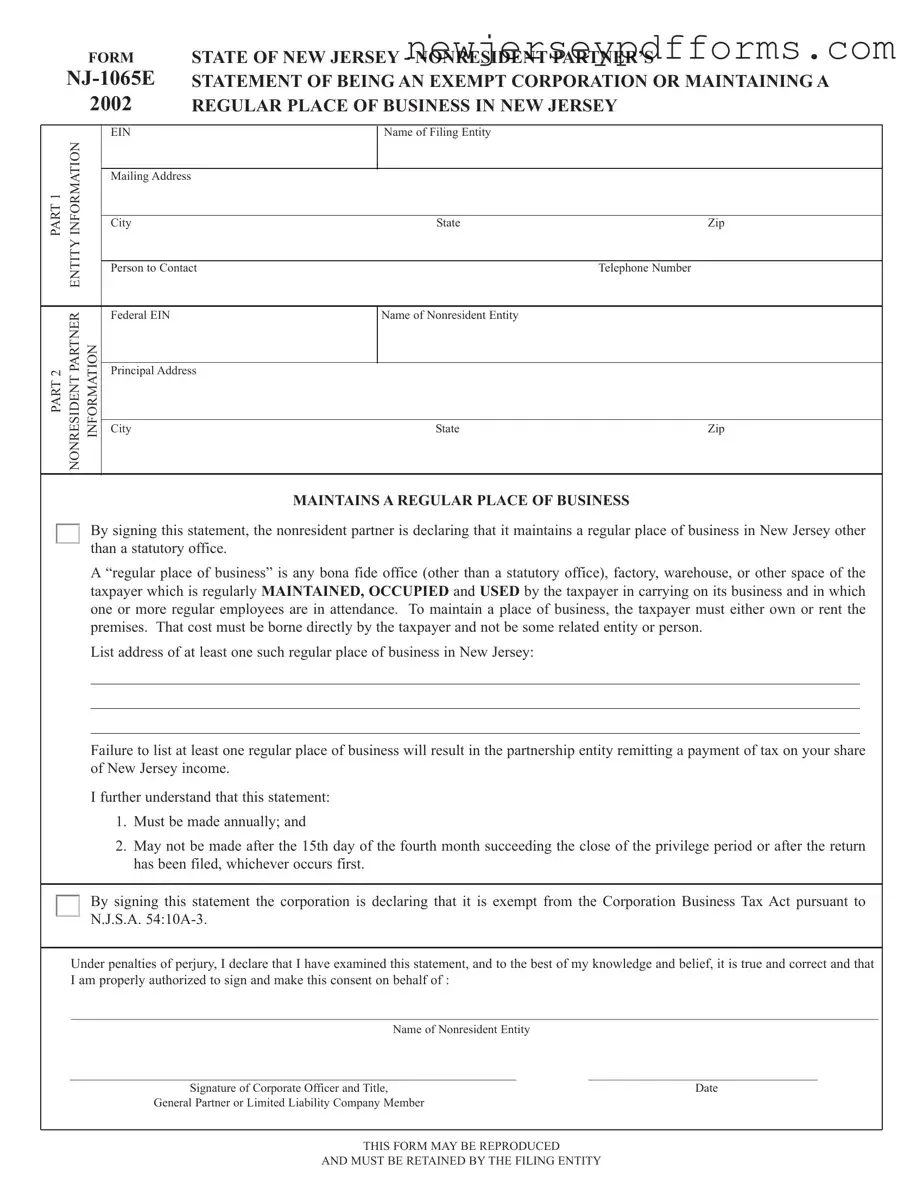

| Form Purpose | The NJ 1065E form is used by nonresident partners to declare their exempt status as a corporation or to confirm they maintain a regular place of business in New Jersey. |

| Filing Requirement | This statement must be filed annually and cannot be submitted after the 15th day of the fourth month following the close of the privilege period or after the tax return has been filed. |

| Regular Place of Business Definition | A "regular place of business" is defined as a bona fide office, factory, warehouse, or other space regularly maintained, occupied, and used by the taxpayer for business purposes. |

| Governing Law | The form is governed by the New Jersey Corporation Business Tax Act, specifically N.J.S.A. 54:10A-3, which outlines the exemptions applicable to certain corporations. |

| Consequences of Non-Compliance | Failure to list at least one regular place of business may result in the partnership entity being required to remit tax on the nonresident partner's share of New Jersey income. |

Creating a Job Application - Employment history must be accurately documented for the last five years for verification.

Child Custody Application Form Nj - This packet is tailored for individuals representing themselves in court.

When completing the NJ 1065E form, individuals often make several common mistakes that can lead to complications. One frequent error is failing to provide the correct mailing address for the nonresident entity. It is essential to ensure that the address listed is accurate and complete, as any discrepancies may result in delays or miscommunication with tax authorities.

Another mistake involves not listing a regular place of business in New Jersey. The form explicitly requires the nonresident partner to declare a bona fide office or other business space. Omitting this information can lead to the partnership being liable for taxes on the individual’s share of New Jersey income. It is crucial to identify at least one location that meets the criteria outlined in the form.

In addition, individuals sometimes overlook the importance of signing the form. The declaration must be signed by an authorized corporate officer or a member of the limited liability company. Without this signature, the submission may be deemed incomplete, resulting in potential penalties or the form being rejected altogether.

Lastly, some filers fail to submit the form by the deadline. The NJ 1065E must be filed annually and cannot be submitted after the 15th day of the fourth month following the close of the privilege period. Missing this deadline can have financial repercussions, including the imposition of taxes that could have been avoided with timely filing.

What is the NJ 1065E form?

The NJ 1065E form is a statement for nonresident partners of partnerships in New Jersey. It is used to declare whether a nonresident partner maintains a regular place of business in New Jersey or is exempt from the Corporation Business Tax Act. This form must be filed annually.

Who needs to file the NJ 1065E form?

Nonresident partners of partnerships that either maintain a regular place of business in New Jersey or are claiming an exemption from the Corporation Business Tax must file this form. It is crucial for compliance with New Jersey tax regulations.

What does it mean to maintain a regular place of business?

A regular place of business is defined as any bona fide office, factory, warehouse, or other space that is regularly occupied and used by the taxpayer in conducting business. It must have one or more regular employees in attendance and the taxpayer must either own or rent the premises.

What happens if a nonresident partner does not list a regular place of business?

If a nonresident partner fails to list at least one regular place of business on the NJ 1065E form, the partnership entity will be required to pay tax on the partner's share of New Jersey income. This emphasizes the importance of accurate reporting.

When is the NJ 1065E form due?

The NJ 1065E form must be submitted annually and cannot be filed after the 15th day of the fourth month following the end of the privilege period. It also cannot be submitted after the partnership's tax return has been filed.

What is the significance of signing the NJ 1065E form?

By signing the NJ 1065E form, the nonresident partner is declaring the truthfulness of the information provided and confirming their authorization to file on behalf of the entity. This statement is made under penalties of perjury, highlighting its legal importance.

Can the NJ 1065E form be reproduced?

Yes, the NJ 1065E form may be reproduced. However, it is essential that the filing entity retains a copy for its records, ensuring compliance and ease of reference in future filings.

What are the exemptions listed under the Corporation Business Tax Act?

Exemptions include various types of corporations such as those assessed based on gross receipts, nonprofit organizations, and certain utility companies. Each exemption has specific criteria that must be met to qualify.

Who should be contacted for questions regarding the NJ 1065E form?

For questions related to the NJ 1065E form, it is advisable to contact the person listed on the form as the point of contact. This individual can provide specific guidance and clarification regarding the filing process.

Is there a filing fee associated with the NJ 1065E form?

No, there is no filing fee specifically for submitting the NJ 1065E form. However, partnerships may have other tax obligations, so it is essential to review all applicable regulations.

Understanding the NJ 1065E form can be challenging, and there are several misconceptions that often arise. Here are seven common misunderstandings about this important document:

This is not true. The form is specifically designed for nonresident partners who have a stake in a partnership that operates in New Jersey. Nonresidents must file this form to report their share of income earned in the state.

In reality, filing this form is mandatory for nonresident partners if they maintain a regular place of business in New Jersey. Failing to do so can result in the partnership being liable for tax payments on the nonresident's share of income.

This is incorrect. The form must be submitted annually and cannot be filed after the 15th day of the fourth month following the end of the partnership's tax year. Timeliness is crucial to avoid penalties.

Actually, it is a critical requirement. The form mandates that nonresident partners must provide the address of at least one bona fide office, factory, or other space used for business in New Jersey. Without this information, the partnership may incur additional tax liabilities.

This is misleading. Only partnerships with nonresident partners who have a regular place of business in New Jersey are required to file this form. If there are no nonresident partners or if they do not maintain a business location in the state, the form is not necessary.

While the form allows nonresident partners to declare their exemption from the Corporation Business Tax Act, it does not exempt them from other taxes that may apply. It is important to understand the specific exemptions and obligations that exist.

This is a significant oversight. The form must be signed by an authorized corporate officer or a member of the limited liability company. Filing without proper authorization can lead to legal complications.

By clarifying these misconceptions, individuals can better navigate the requirements associated with the NJ 1065E form and ensure compliance with New Jersey tax laws.

The NJ 1065E form is similar to the IRS Form 1065, which is used by partnerships to report income, deductions, gains, and losses from their operations. Both forms serve the purpose of providing information about the partnership's financial activities, but the NJ 1065E focuses specifically on nonresident partners and their exemption status in New Jersey. While Form 1065 is filed at the federal level, the NJ 1065E is tailored to meet state requirements, ensuring that nonresident partners comply with New Jersey tax laws. Both forms require detailed information about the partnership and its partners, but the NJ 1065E emphasizes the necessity of maintaining a regular place of business within the state.

Another document similar to the NJ 1065E is the New Jersey Corporation Business Tax (CBT) return, known as Form CBT-100. This form is used by corporations operating in New Jersey to report their income and calculate their tax liability. Like the NJ 1065E, the CBT-100 requires detailed financial information and is essential for compliance with state tax laws. However, while the NJ 1065E addresses partnerships and their nonresident partners, the CBT-100 focuses solely on corporations, highlighting the differences in tax treatment between various business structures. Both forms are critical for ensuring that entities operating in New Jersey fulfill their tax obligations.

The NJ 1040 form, used by individual taxpayers in New Jersey, also shares similarities with the NJ 1065E. Both forms require the reporting of income earned within the state and are designed to ensure compliance with New Jersey tax regulations. While the NJ 1065E is specifically for partnerships and their nonresident partners, the NJ 1040 is for individual residents and nonresidents who earn income in New Jersey. Both forms necessitate the disclosure of income sources and may involve deductions or exemptions, making them essential for accurate tax reporting in the state.

Form NJ-1065 is comparable to the IRS Form 8865, which is used by U.S. persons who own an interest in a foreign partnership. Both forms require information about the partnership's operations and the partners involved. However, while Form 8865 focuses on international partnerships and their U.S. partners, the NJ 1065E is tailored to New Jersey's specific tax requirements for nonresident partners. Each form addresses the unique needs of its respective jurisdiction, ensuring that all relevant income and tax obligations are reported appropriately.

In navigating the complexities of tax documentation, understanding the importance of obtaining a PDF Document Service for your Sample Tax Return Transcript can streamline your process significantly, ensuring that you have access to a formatted and accurate record of your tax information when needed.

Lastly, the NJ 1065E can be likened to the New Jersey Partnership Return (Form NJ-1065), which is used to report the income, deductions, and credits of partnerships operating in the state. Both forms are essential for partnerships to comply with New Jersey tax laws, but the NJ 1065E specifically addresses the exemption status of nonresident partners. While the NJ-1065 provides a comprehensive overview of the partnership's financial activities, the NJ 1065E focuses on the obligations of nonresident partners and their need to maintain a regular place of business in New Jersey. Both forms are crucial for accurate reporting and compliance within the state's tax framework.