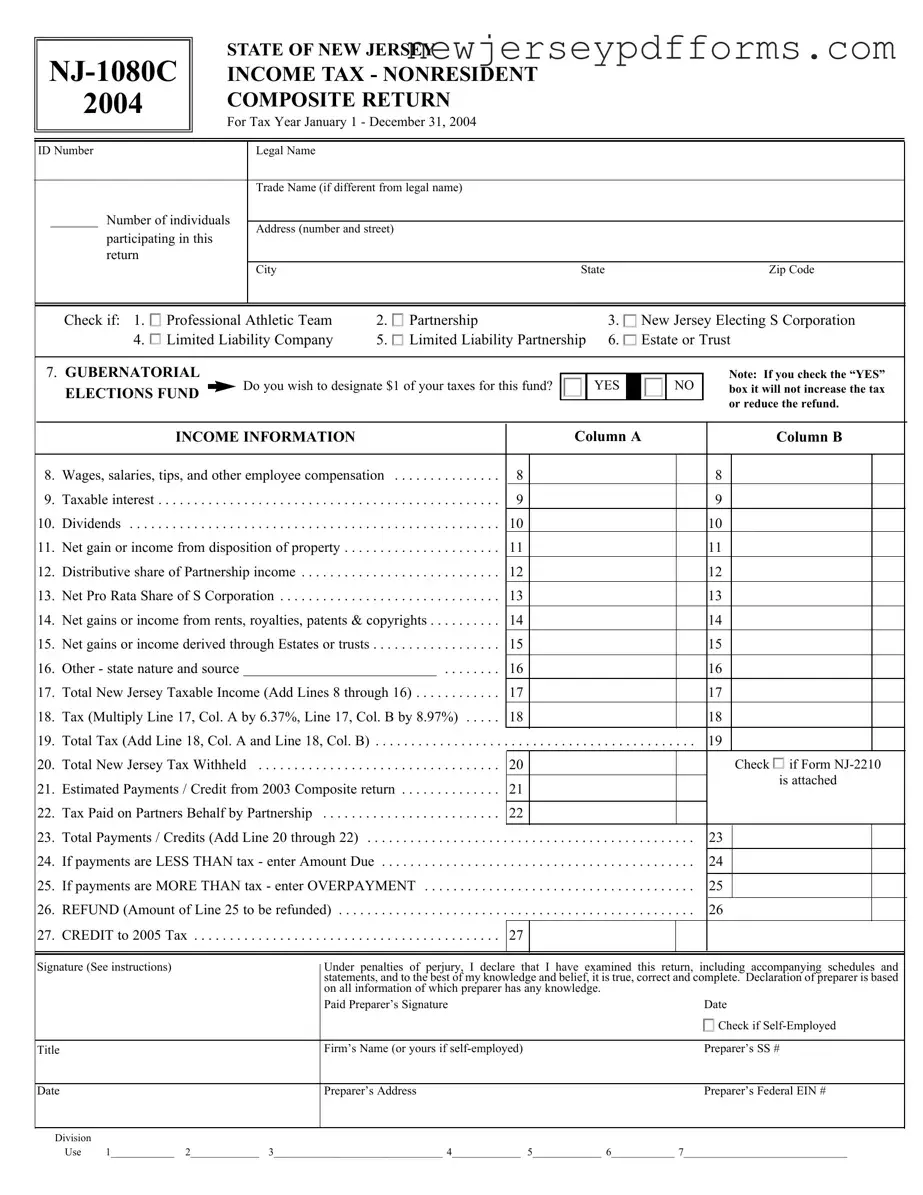

Printable Nj 1080C Form

Printable Nj 1080C Form

| Fact Name | Description |

|---|---|

| Form Purpose | The NJ-1080C form is used for filing a nonresident composite income tax return in New Jersey. |

| Eligibility | Qualified nonresident individuals from specific entities, like partnerships and S corporations, can participate in this return. |

| Tax Year | This form is specifically for the tax year running from January 1 to December 31, 2004. |

| Tax Rates | The form employs two tax rates: 6.37% for incomes under $250,000 and 8.97% for incomes of $250,000 or more. |

| Filing Deadline | Returns are due by April 15, 2005. Late submissions may incur penalties. |

| Election Requirement | Each participant must file Form NJ-1080-E annually to elect inclusion in the composite return. |

| Postmark Consideration | Returns postmarked by the due date are considered timely filed, regardless of when they are received. |

| Governing Law | The NJ-1080C form is governed by New Jersey income tax laws, specifically for nonresidents. |

New Jersey Employer Taxes - All relevant financial information should be documented directly on the form.

The Pennsylvania Motor Vehicle Bill of Sale form is a legal document that facilitates the transfer of ownership of a vehicle. This form serves as proof of purchase and includes essential information about the vehicle and the involved parties. For those seeking a reliable template, the PDF Document Service is an excellent resource. Completing this document correctly is vital to ensure a smooth transaction.

Free Annulment Forms - Each income source must be reported to establish a complete financial overview.

Filling out the NJ-1080C form can be a bit tricky, and mistakes can lead to delays or even penalties. One common error is failing to include all required participants. If you're filing a composite return, make sure to list every individual involved. Missing even one participant can complicate your return and may result in an incomplete filing.

Another frequent mistake is not checking the right box for the type of entity. Whether you're part of a professional athletic team, partnership, or another entity, selecting the correct option is crucial. Misclassification could lead to issues with your tax calculations.

People often overlook the income limits when categorizing participants. If a participant’s income is less than $250,000, they should be listed on Schedule A. Those with $250,000 or more belong on Schedule B. Mixing these up can result in incorrect tax calculations and potential penalties.

Additionally, many filers forget to carry totals from the participant directories to the main form. Ensure that the total taxable income from both Schedule A and Schedule B is accurately transferred to the appropriate lines on the NJ-1080C. This step is vital for an accurate tax calculation.

Another common mistake is not signing the form. A signature is required to validate your return. Without it, the return may be considered incomplete, leading to unnecessary delays.

People also tend to underestimate the importance of double-checking calculations. Simple arithmetic errors can lead to incorrect tax amounts owed or refunds due. Always review your numbers to avoid these mistakes.

Not attaching necessary forms is another pitfall. If you are claiming estimated payments or credits from the previous year, ensure that you include Form NJ-2210 if applicable. Failing to do so could result in complications with your tax return.

Some filers forget to indicate if they wish to designate $1 for the elections fund. While this does not affect your tax amount, it’s a small detail that should not be overlooked. Make sure to check the box if you want to contribute.

Lastly, be mindful of the filing deadline. The NJ-1080C for tax year 2004 was due on April 15, 2005. Late submissions can incur penalties and interest. Keep track of deadlines to ensure timely filing.

What is the NJ-1080C form and who needs to file it?

The NJ-1080C form is a nonresident composite income tax return for the state of New Jersey. It is specifically designed for qualified nonresident individuals who are members of certain entities such as partnerships, professional athletic teams, limited liability companies, and New Jersey electing S corporations. If you are a nonresident who meets the criteria and is part of one of these entities, you may need to file this form to report your income earned in New Jersey.

What are the eligibility requirements for participating in a composite return?

To participate in a composite return using the NJ-1080C form, several conditions must be met. First, you must be a nonresident for the entire taxable year and not maintain a permanent place of abode in New Jersey. Additionally, you should not be a fiscal year filer and must not have income from New Jersey sources other than what is reported on the composite return. You will also need to waive your right to claim any personal exemptions, credits, or deductions in New Jersey and must complete and submit Form NJ-1080-E to the filing entity to elect participation.

How is the tax calculated on the NJ-1080C form?

The tax on the NJ-1080C form is calculated based on the total New Jersey taxable income reported. For participants with income less than $250,000, the tax rate is 6.37%. For those with income of $250,000 or more, the tax rate is 8.97%. The total taxable income for each participant is summed and reported on the appropriate lines of the form, ensuring that the correct tax rate is applied based on the income thresholds.

When is the NJ-1080C form due, and what if I need an extension?

The NJ-1080C form for the tax year 2004 is due on April 15, 2005. If you require more time to file, you can request an extension using Form NJ-630. This request must be submitted by the original due date of the return. If at least 80% of the actual tax liability is paid by that date, a four-month extension will be granted. An additional two-month extension may be requested before the first extension expires, but it is crucial to adhere to these deadlines to avoid penalties and interest.

What information is required to complete the NJ-1080C form?

To complete the NJ-1080C form, you will need to provide various details, including your legal name, ID number, and the number of individuals participating in the return. You must also report income details such as wages, salaries, taxable interest, dividends, and other sources of income. The form includes sections for both participants with income less than $250,000 and those with income equal to or greater than that amount, ensuring that the correct tax calculations can be made based on the income reported.

Misconceptions about the NJ 1080C form can lead to confusion and potential errors in filing. Here are four common misunderstandings:

In reality, the NJ 1080C is specifically designed for nonresident individuals who are part of certain entities, such as partnerships or S corporations. It allows these individuals to file a composite return, simplifying the process for those who do not reside in New Jersey but earn income from it.

This is not true. Only specific types of income, such as wages, dividends, and partnership income, can be reported on the form. Nonresident individuals must ensure that their income qualifies under the guidelines set forth for the composite return.

Filing the NJ 1080C does not exempt individuals from paying taxes. Instead, it allows nonresidents to pay their New Jersey taxes collectively through the entity they are associated with. The tax rates applied can vary based on the income level reported.

This is incorrect. Each individual must make a written election to participate in the composite return annually by submitting Form NJ-1080-E. This ensures that all parties are aware of their participation and obligations for that tax year.

The NJ-1040 form is a personal income tax return used by New Jersey residents. Like the NJ-1080C, it requires taxpayers to report their income, deductions, and tax credits. However, the NJ-1040 is specifically for individuals, while the NJ-1080C is designed for nonresident composite returns. Both forms require detailed income information and allow for certain credits, but the NJ-1040 may include more personal exemptions and credits specific to residents.

The NJ-1065 form is used by partnerships to report income, gains, losses, deductions, and credits. Similar to the NJ-1080C, it allows for the reporting of multiple individuals' income in a single return. However, the NJ-1065 is intended for partnerships, while the NJ-1080C is for nonresident individuals participating in a composite return. Both forms require a detailed breakdown of income sources and distributions to partners or participants.

The NJ-1120S form serves as the tax return for New Jersey S corporations. It shares similarities with the NJ-1080C in that both forms deal with entities that pass income through to their members or shareholders. While the NJ-1080C is for nonresidents participating in a composite return, the NJ-1120S focuses on S corporations and their shareholders, reflecting the tax obligations specific to corporate structures.

The NJ-1040NR form is specifically for nonresidents who earn income in New Jersey. Like the NJ-1080C, it is designed for individuals who do not reside in the state but have New Jersey-sourced income. Both forms require reporting of income and tax calculations, but the NJ-1040NR is for individual taxpayers, while the NJ-1080C consolidates multiple nonresidents' income into a single return.

The NJ-630 form is used to request an extension for filing New Jersey income tax returns. It is similar to the NJ-1080C in that it can be filed by entities or individuals who need additional time to submit their tax returns. While the NJ-1080C is a return itself, the NJ-630 is a request for more time, which can apply to composite returns as well as individual filings.

In addition to understanding various tax forms used in New Jersey, it is essential to recognize the importance of the Georgia WC 100 form, a crucial document used to request settlement mediation in workers' compensation cases. This form not only formalizes requests to the Georgia State Board of Workers' Compensation but also facilitates mediation to reach a settlement, making it vital for employees, employers, and insurers. For more information on this subject, you can visit formsgeorgia.com.

The NJ-2210 form is used to calculate underpayment penalties for New Jersey income tax. It relates to the NJ-1080C in that both forms deal with tax liability calculations. While the NJ-1080C is a return reporting income and taxes owed, the NJ-2210 assesses whether sufficient tax payments were made throughout the year, potentially leading to penalties if underpayments are identified.

The NJ-1040X form is an amended New Jersey income tax return. It allows taxpayers to correct errors on previously filed returns, similar to how the NJ-1080C may need adjustments for composite returns. Both forms require detailed reporting of income and tax calculations, but the NJ-1040X is focused on amendments rather than original filings.

The NJ-CR form is a tax credit application used to claim various credits available to New Jersey taxpayers. It is similar to the NJ-1080C in that both forms can affect the overall tax liability. However, while the NJ-1080C consolidates income reporting for nonresident individuals, the NJ-CR focuses solely on claiming credits that can reduce tax owed, applicable to both residents and nonresidents.