Printable Nj 1080E Form

Printable Nj 1080E Form

| Fact Name | Details |

|---|---|

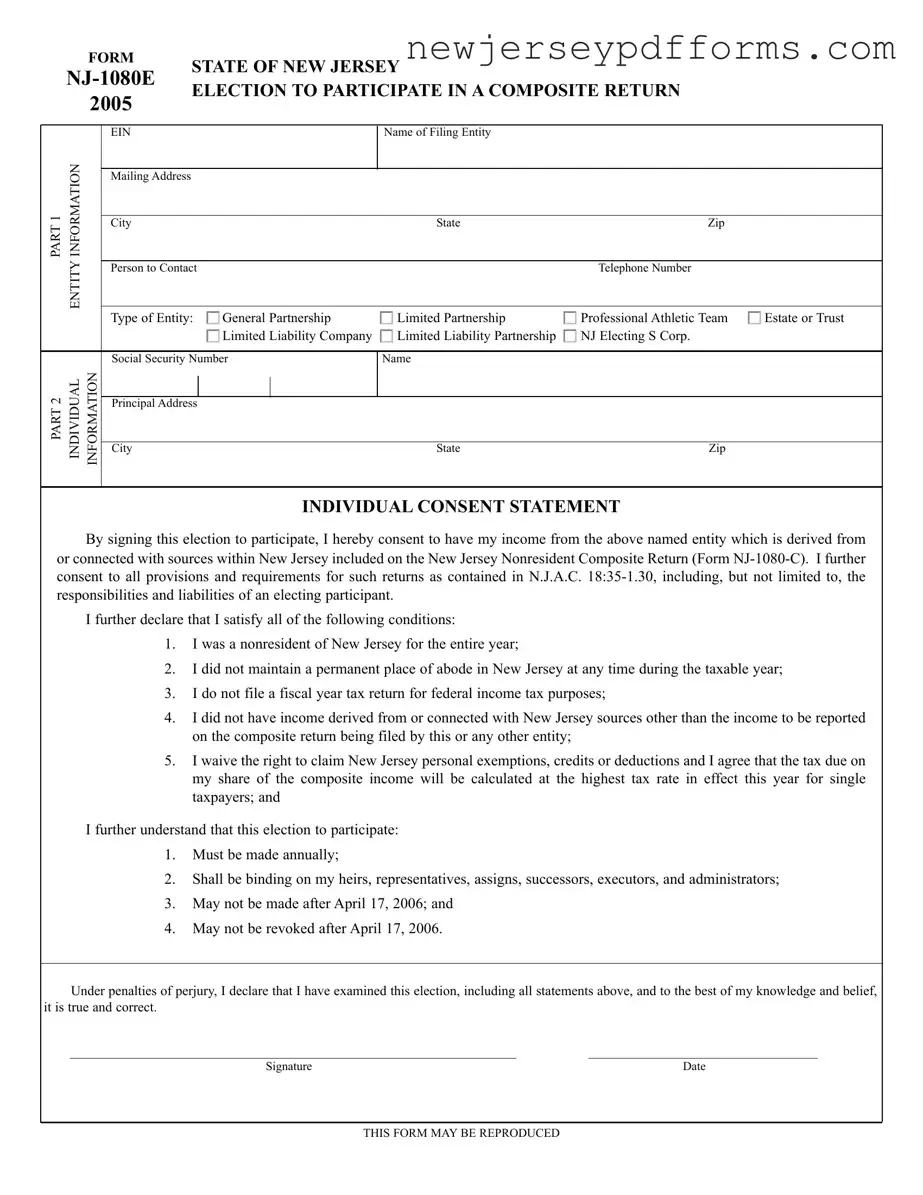

| Purpose of Form | The NJ-1080E form is used to elect participation in a composite return for nonresident individuals who have income derived from New Jersey sources. |

| Eligibility Requirements | To participate, individuals must be nonresidents for the entire year, not maintain a permanent abode in New Jersey, and meet other specified conditions outlined in N.J.A.C. 18:35-1.30. |

| Filing Deadline | The election must be made annually and cannot be submitted after April 17 of the tax year in question. |

| Governing Laws | The form is governed by New Jersey Administrative Code (N.J.A.C.) 18:35-1.30 and the Gross Income Tax Act (N.J.S.A. 54A:1-1 et seq.). |

| Binding Nature | Once submitted, the election is binding on the individual’s heirs and representatives, and it cannot be revoked after the filing deadline. |

| Tax Calculation | The tax due on the composite return is calculated at the highest rate for single taxpayers, without personal exemptions or credits. |

New Jersey Real Estate Contract - At closing, buyers must pay the remaining balance through accepted payment methods.

Having a well-structured Operating Agreement is essential for limited liability companies (LLCs), as it not only defines the management structure and operating procedures but also acts as a tool for conflict resolution among members. To learn more about crafting this important document, you can visit topformsonline.com/operating-agreement, which provides valuable resources and insights into the requirements and best practices for developing an effective agreement.

1065 Return - All partners should review the form carefully to ensure all information is correct.

Filling out the NJ-1080E form can be straightforward, but many people make common mistakes that can lead to complications. One frequent error is not providing complete information about the entity. The form requires details such as the name of the filing entity, its mailing address, and the type of entity. Omitting any of this information can delay processing and may even result in rejection of the form.

Another mistake is failing to check the eligibility requirements. Participants must be nonresidents for the entire year and must not maintain a permanent place of abode in New Jersey. Some individuals mistakenly believe they qualify without meeting these conditions, which can lead to issues later on.

Many people also overlook the importance of signing the form. A signature is not just a formality; it confirms that the individual consents to have their income included in the composite return. Without a signature, the form is considered incomplete, and the election cannot be processed.

Additionally, individuals sometimes forget to submit the NJ-1080E form before the deadline. This form must be filed annually and cannot be submitted after April 17 of the tax year. Missing this deadline means losing the opportunity to participate in the composite return for that year.

Some participants mistakenly believe they can revoke their election after the deadline. However, the election is binding once made, and revocation is not permitted after the specified date. This misunderstanding can lead to unexpected tax liabilities.

Another common error is not understanding the implications of waiving personal exemptions, credits, or deductions. Participants agree to have their tax calculated at the highest rate without these benefits. This can result in a higher tax bill than anticipated if individuals are not aware of this provision.

Lastly, individuals sometimes fail to keep copies of the completed NJ-1080E form. Retaining a copy is essential, as the filing entity must provide it upon request from the Division of Taxation. Without a copy, participants may struggle to verify their participation if questions arise later.

What is the NJ-1080E form?

The NJ-1080E form is an election form used by nonresident individuals who wish to participate in a composite return filed by certain entities doing business in New Jersey. This form allows individuals to have their income from the entity included on the New Jersey Nonresident Composite Return (Form NJ-1080-C). By signing the form, individuals consent to the inclusion of their income and agree to the associated provisions and requirements outlined in New Jersey law.

Who can use the NJ-1080E form?

The NJ-1080E form can be utilized by qualified nonresident individuals who meet specific criteria. These individuals must have been nonresidents of New Jersey for the entire tax year, not maintained a permanent place of abode in New Jersey, and not filed a fiscal year tax return for federal income tax purposes. Additionally, they should not have other income derived from New Jersey sources, must waive certain exemptions and credits, and agree to have their tax calculated at the highest rate for single taxpayers.

When must the NJ-1080E form be submitted?

The NJ-1080E form must be submitted annually and should be completed and delivered to the filing entity before the composite return is filed. It is important to note that the election to participate in the composite return cannot be made after April 15 following the close of the taxable year. Once submitted, the election is binding and cannot be revoked after the deadline.

What are the responsibilities of individuals who sign the NJ-1080E form?

By signing the NJ-1080E form, individuals accept personal responsibility for the accuracy of the information provided. They agree to the terms set forth in the form, including the understanding that they will not claim New Jersey personal exemptions, credits, or deductions. Each participant is also liable for their share of the tax due based on the composite return and must ensure that all income is reported accurately.

What happens if an individual discovers additional income after filing the composite return?

If a participant discovers additional income derived from New Jersey sources after the composite return has been filed, they are required to file a separate Nonresident New Jersey Gross Income Tax Return (Form NJ-1040NR). This return must include all income sources, including the income reported on the composite return. Participants can claim a credit for the gross income tax paid on their behalf through the composite return when filing the NJ-1040NR.

Misconception 1: The NJ-1080E form is only for residents of New Jersey.

This form is specifically designed for nonresidents who wish to participate in a composite return. Nonresidents can elect to have their income from a New Jersey entity included in a composite return.

Misconception 2: Filing the NJ-1080E form guarantees a refund.

Submitting the NJ-1080E does not guarantee a refund. It simply allows for the inclusion of nonresident income in a composite return, which may or may not result in a refund depending on the individual's tax situation.

Misconception 3: Once I file the NJ-1080E, I can change my mind later.

The election made through the NJ-1080E is binding and cannot be revoked after the filing deadline. It must be completed annually and is effective only for that tax year.

Misconception 4: I can file the NJ-1080E at any time during the year.

The NJ-1080E must be submitted before the composite return is filed, typically by April 15 of the following year. Late submissions will not be accepted.

Misconception 5: All types of income can be included in the composite return.

Only income derived from or connected with New Jersey sources and reported on the composite return can be included. Other sources of income require a separate filing.

Misconception 6: Filing a composite return means I don't have to file anything else.

Participants in a composite return may still need to file a separate NJ-1040NR if they have additional income from New Jersey sources not reported in the composite return.

Misconception 7: The NJ-1080E form is not necessary if my entity files a composite return.

The NJ-1080E is essential for each nonresident participant to consent to be included in the composite return. Without it, the individual cannot be included.

The NJ-1040NR form is the Nonresident New Jersey Gross Income Tax Return. It is similar to the NJ-1080E form in that both are used by individuals who earn income connected to New Jersey but do not reside in the state. While the NJ-1080E allows nonresidents to elect to participate in a composite return filed by an entity, the NJ-1040NR is for individuals who do not participate in such a return and must report all income from New Jersey sources. Both forms require personal information, including Social Security numbers and income details, but the NJ-1040NR is more comprehensive in capturing all income sources, not just those related to a specific entity.

Understanding the intricacies of the Power of Attorney form can be highly beneficial, particularly for those navigating legal documentation and ensuring decisions align with their intentions even when they cannot act directly. For those seeking a reliable template to create such a document, resources like PDF Document Service can provide essential guidance and support in drafting a thorough and legally sound Power of Attorney form.

The NJ-1065 form serves as the Partnership Return for New Jersey Income Tax. This document is similar to the NJ-1080E in that it is filed by partnerships, which can include nonresident partners. The NJ-1065 outlines the income, deductions, and credits of the partnership and provides a Schedule NJK-1 for each partner. Like the NJ-1080E, it facilitates the reporting of income derived from New Jersey sources, although the NJ-1065 is focused on the entity level while the NJ-1080E pertains to individual elections to be included in a composite return.

The NJ-1065S form is the New Jersey S Corporation Return. This document is similar to the NJ-1080E in that it allows S corporations to report income while providing information for shareholders, including nonresidents. Each shareholder receives a Schedule NJ-K-1, which details their share of income. The NJ-1065S captures the income of the S corporation, while the NJ-1080E allows individuals to consent to have their income reported on a composite return, emphasizing the collaborative nature of tax reporting for nonresidents.

The NJ-1040 form is the standard New Jersey Resident Income Tax Return. It shares similarities with the NJ-1080E in that both forms require individuals to report income and calculate tax liabilities. However, the NJ-1040 is specifically for residents, while the NJ-1080E is for nonresidents electing to participate in a composite return. Both forms require personal identification and income details, but the NJ-1040 allows for exemptions and deductions that are not available to participants of the NJ-1080E.

The NJ-630 form is the Application for Extension of Time to File New Jersey Income Tax Returns. This document is similar to the NJ-1080E in that it can be used by entities that are filing composite returns. While the NJ-630 allows for an extension of time to file, the NJ-1080E is focused on the election to participate in a composite return. Both forms are essential for ensuring compliance with New Jersey tax obligations, particularly for those involved in partnerships or corporate entities.

The W-2 form, Wage and Tax Statement, is another relevant document. It is similar to the NJ-1080E in that it reports income earned by individuals, including nonresidents. Employers provide W-2 forms to employees, detailing wages and taxes withheld. While the NJ-1080E allows individuals to consent to have their income included in a composite return, the W-2 serves as a record of earned income that may also be reported on various tax forms, including the NJ-1040NR or NJ-1080-C.

The K-1 form, which is used for partnerships and S corporations, also has similarities with the NJ-1080E. Each partner or shareholder receives a K-1 that reports their share of income, deductions, and credits from the entity. While the NJ-1080E is used by nonresidents to elect to participate in a composite return, the K-1 provides the necessary information for individuals to report their income from partnerships or S corporations on their tax returns, including the NJ-1040NR.

The NJ-1040ES form is the Estimated Tax Payment Voucher for Individuals. This document is similar to the NJ-1080E in that it is utilized by individuals who may owe taxes on income derived from New Jersey sources. While the NJ-1080E allows for participation in a composite return, the NJ-1040ES is focused on making estimated tax payments to avoid penalties. Both forms are essential for individuals managing their tax responsibilities in relation to New Jersey income.

The NJ-PTA form, or Property Tax Reimbursement Application, is another document that shares some similarities with the NJ-1080E. While primarily aimed at homeowners and renters seeking reimbursement for property taxes, it also requires individuals to report income. The NJ-1080E focuses on nonresident income derived from specific entities, while the NJ-PTA addresses property tax relief for eligible individuals, highlighting different aspects of New Jersey tax obligations.