Printable Nj 165 Form

Printable Nj 165 Form

| Fact Name | Details |

|---|---|

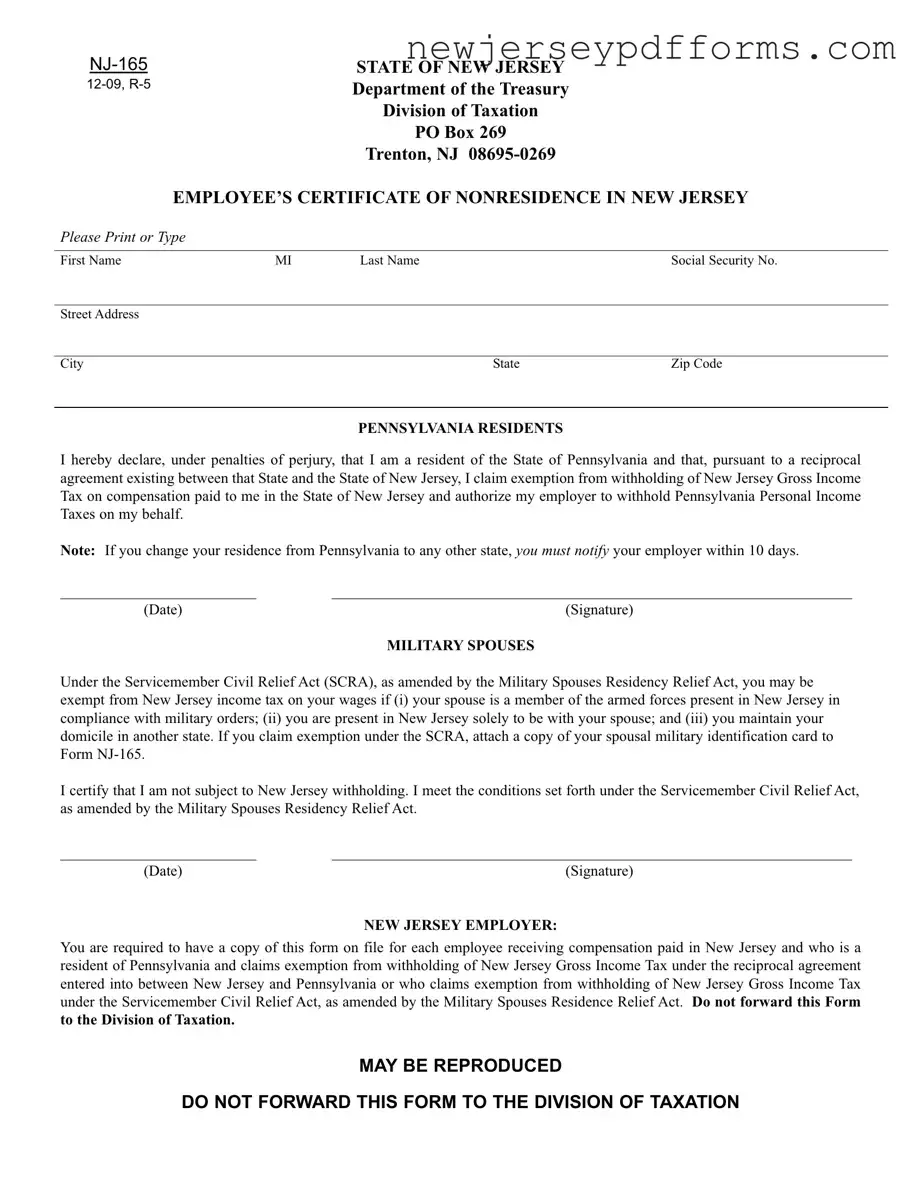

| Purpose | The NJ-165 form is used by employees who are residents of Pennsylvania to claim exemption from New Jersey Gross Income Tax withholding. |

| Governing Laws | This form is governed by the reciprocal tax agreement between New Jersey and Pennsylvania, as well as the Servicemember Civil Relief Act (SCRA) and the Military Spouses Residency Relief Act. |

| Filing Requirement | Employers in New Jersey must keep a copy of the NJ-165 form on file for each eligible employee who claims exemption from withholding. |

| Notification | If a Pennsylvania resident changes their residence to another state, they must inform their employer within 10 days. |

Ba 208 - The document serves as a timestamp for the transaction, noting the sale date.

To learn more about how this document can facilitate your wishes, consider referring to the guide on the important aspects of a General Power of Attorney.

School Choice Nj - Include necessary documentation to avoid delays in the renewal process.

Completing the NJ-165 form accurately is essential for Pennsylvania residents claiming exemption from New Jersey income tax withholding. However, several common mistakes can hinder the process. One frequent error is failing to provide complete personal information. The form requires the first name, middle initial, last name, social security number, and full address. Omitting any of these details can lead to delays or rejections.

Another mistake involves incorrectly claiming residency. Some individuals may misunderstand their residency status, leading to inaccurate declarations. It is crucial to ensure that the declaration of being a Pennsylvania resident is truthful and supported by appropriate documentation. Misrepresentation can result in penalties.

Many people also overlook the requirement to notify their employer of any changes in residency. If a resident moves from Pennsylvania to another state, they must inform their employer within ten days. Failing to do so can result in improper withholding of taxes, complicating future tax filings.

Additionally, individuals claiming exemptions under the Servicemember Civil Relief Act often forget to attach the necessary documentation. A copy of the spousal military identification card must accompany the form if one is claiming this exemption. Without this attachment, the claim may be invalidated.

Another common oversight is not signing and dating the form. Both the date and signature are critical components of the NJ-165. A missing signature or date can render the form incomplete, leading to further complications in processing.

Lastly, some individuals mistakenly believe they need to submit the NJ-165 form to the Division of Taxation. This form is meant to be kept on file by the employer, not forwarded to the state. Understanding this requirement is vital to avoid unnecessary paperwork and confusion.

What is the NJ-165 form?

The NJ-165 form is an Employee’s Certificate of Nonresidence in New Jersey. It is used by individuals who are residents of Pennsylvania to claim exemption from New Jersey Gross Income Tax withholding. This form is particularly relevant for employees who work in New Jersey but reside in Pennsylvania due to a reciprocal tax agreement between the two states.

Who needs to fill out the NJ-165 form?

Individuals who are residents of Pennsylvania and work in New Jersey should complete the NJ-165 form. This includes employees who want to claim exemption from New Jersey's Gross Income Tax withholding. Additionally, military spouses who meet specific criteria under the Servicemember Civil Relief Act may also use this form to claim exemption.

What information is required on the NJ-165 form?

The form requires basic personal information, including your first name, middle initial, last name, Social Security number, street address, city, state, and zip code. If you are a military spouse claiming exemption, you will also need to provide a copy of your spousal military identification card.

How does the reciprocal agreement between New Jersey and Pennsylvania work?

The reciprocal agreement allows residents of Pennsylvania to work in New Jersey without having New Jersey Gross Income Tax withheld from their paychecks. Instead, employers will withhold Pennsylvania Personal Income Taxes. This agreement simplifies tax obligations for individuals who live in one state and work in another.

What should I do if I move from Pennsylvania to another state?

If you change your residence from Pennsylvania to another state, it is important to notify your employer within 10 days. This ensures that your tax withholding is adjusted according to your new residency status.

What are the criteria for military spouses to claim exemption?

Military spouses can claim exemption from New Jersey income tax if three conditions are met: their spouse must be a member of the armed forces stationed in New Jersey, they must be in New Jersey solely to be with their spouse, and they must maintain their domicile in another state. Proof of military status is required when claiming this exemption.

Do I need to submit the NJ-165 form to the Division of Taxation?

No, you do not need to send the NJ-165 form to the Division of Taxation. Instead, your employer is required to keep a copy of the form on file for each employee who claims exemption from New Jersey Gross Income Tax under the applicable provisions.

What happens if I do not submit the NJ-165 form?

If you do not submit the NJ-165 form and you are eligible for the exemption, your employer may withhold New Jersey Gross Income Tax from your paycheck. This could lead to unnecessary tax payments that you may need to reclaim later.

Can the NJ-165 form be reproduced?

Yes, the NJ-165 form may be reproduced for your use. However, it should not be forwarded to the Division of Taxation. Keep the completed form with your employer's records.

Here are 10 common misconceptions about the NJ 165 form, along with clarifications for each:

The NJ-165 form, known as the Employee’s Certificate of Nonresidence in New Jersey, shares similarities with the W-4 form, which is used by employees to indicate their tax situation to employers. Like the NJ-165, the W-4 allows employees to claim exemptions from withholding, although it is primarily focused on federal income tax. Both forms require personal information, such as the employee's name and Social Security number, and must be submitted to the employer. The W-4 is essential for determining how much federal tax should be withheld from an employee's paycheck, while the NJ-165 specifically addresses state tax obligations for residents of Pennsylvania working in New Jersey.

The Pennsylvania Motor Vehicle Bill of Sale form is a legal document that facilitates the transfer of ownership of a vehicle. This form serves as proof of purchase and includes essential information about the vehicle and the involved parties. Completing this document correctly is vital to ensure a smooth transaction; for those seeking a comprehensive template, the PDF Document Service provides a reliable resource.

Another document comparable to the NJ-165 is the 1099 form, which is used to report income received by independent contractors and freelancers. While the NJ-165 certifies nonresidency for tax withholding purposes, the 1099 form serves to inform the IRS about income earned. Both documents play crucial roles in tax compliance, but they cater to different employment situations. The NJ-165 is focused on withholding exemptions for employees, whereas the 1099 form is used to report income for those not classified as employees.

The NJ-165 also resembles the IRS Form 8833, which is used by taxpayers to disclose treaty-based return positions. Similar to the NJ-165, Form 8833 allows individuals to claim exemptions based on specific agreements—in this case, tax treaties between the U.S. and other countries. Both forms require detailed information about the taxpayer’s residency status and the basis for claiming an exemption, ensuring compliance with tax laws while allowing for certain benefits.

Additionally, the NJ-165 can be compared to the IRS Form 1040, which is the standard individual income tax return form. While the NJ-165 is primarily concerned with withholding exemptions for state taxes, the 1040 is used to report total income and calculate tax liability. Both forms necessitate accurate personal information and are essential for tax compliance, but they serve different purposes in the overall tax process.

The NJ-165 is similar to the Certificate of Residency, which individuals may use to establish residency in a state for tax purposes. Like the NJ-165, this certificate helps taxpayers claim exemptions from certain taxes based on their residency status. Both documents require proof of residency and are submitted to employers or tax authorities to ensure proper tax treatment.

Another related document is the IRS Form 4868, which is an application for an automatic extension of time to file a federal tax return. Although the NJ-165 does not extend deadlines, both documents require timely submission to avoid penalties. The NJ-165 must be submitted to the employer to ensure proper withholding, while Form 4868 grants taxpayers additional time to file their returns, reflecting the importance of maintaining compliance with tax obligations.

The NJ-165 also has similarities with the State Tax Exemption Certificate, which allows taxpayers to claim exemptions from state sales tax. Both documents serve to certify an individual's eligibility for tax exemptions based on specific criteria. While the NJ-165 focuses on income tax withholding, the State Tax Exemption Certificate addresses sales tax, but both require careful documentation and adherence to state regulations.

Lastly, the NJ-165 can be likened to the Residency Affidavit, which is often used by students or individuals to establish residency for tuition or other benefits. Similar to the NJ-165, the Residency Affidavit requires personal information and proof of residency. Both forms are essential in determining eligibility for specific exemptions, ensuring that individuals are taxed appropriately based on their residency status.