Printable Nj 2440 Form

Printable Nj 2440 Form

| Fact Name | Description |

|---|---|

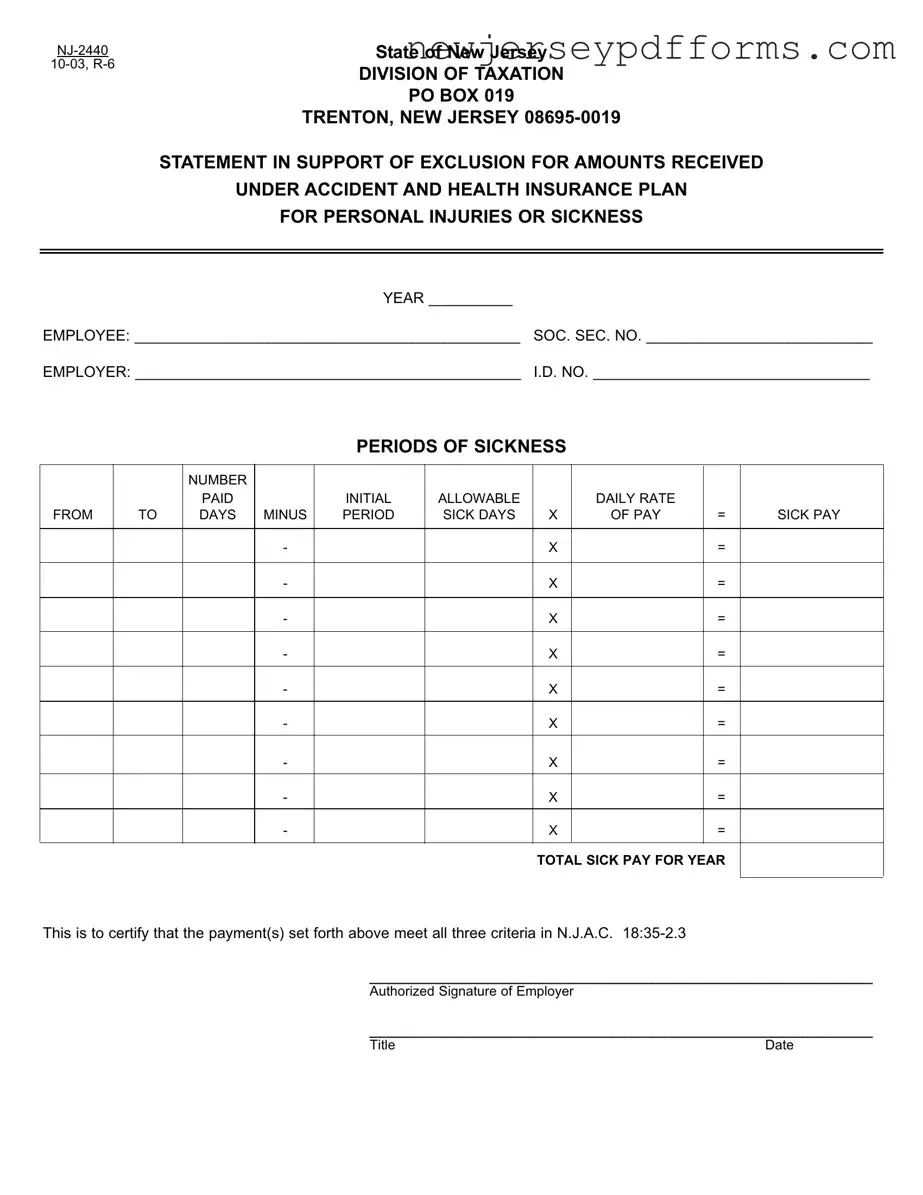

| Form Purpose | The NJ 2440 form is used to support the exclusion of amounts received under an accident and health insurance plan for personal injuries or sickness from taxable gross income. |

| Governing Law | This form is governed by New Jersey Administrative Code N.J.A.C. 18:35-2.3, which outlines the criteria for exclusion from taxable gross income. |

| Eligibility Criteria | Payments must meet three criteria: compensation for wage loss, an enforceable contractual obligation, and not relate to discretionary sick leave. |

| Tax Exclusion Scope | The exclusion applies to payments from both commercial insurance companies and self-insured employer plans, regardless of who pays the premiums. |

| Temporary Disability Payments | Payments made under the New Jersey Temporary Disability Law are also excluded from taxable gross income. |

| Withholding Requirements | Employers must withhold gross income tax on wage payments, even if they qualify for exclusion, except for specific temporary disability payments. |

Nj Taxpayer Id Number - Using a pre-printed form requires verification of the correct details before signing.

Fannie Mae Form 1103 - Timely submission of this form can help mitigate issues during audits.

This simple General Power of Attorney form guide can help you understand the process and requirements for designating someone to manage your affairs effectively.

Nj Pension Exclusion - Failure to provide the required attachments can delay or deny the refund claim.

Filling out the NJ-2440 form can be a straightforward process, but there are common mistakes that people often make. One frequent error is failing to provide accurate information about the employee's Social Security number. This number is crucial for identifying the individual and ensuring that the tax records are correctly matched. If the Social Security number is incorrect, it can lead to delays or complications in processing the form.

Another mistake involves not clearly specifying the periods of sickness. The form requires precise dates to determine the duration of the absence. Omitting or inaccurately reporting these dates can result in miscalculations of sick pay, which may affect the exclusion from taxable gross income. It's essential to double-check that the periods listed align with the sick days taken.

Many individuals also overlook the requirement to provide a total sick pay amount for the year. This figure should reflect the sum of all allowable sick pay received. Failing to include this total can lead to confusion during the review process and may ultimately result in a denial of the exclusion claim.

Additionally, some people mistakenly assume that all payments for sick leave qualify for exclusion under the health insurance plan. However, payments that are discretionary, such as those made during the initial days of absence, do not qualify. Understanding the criteria for exclusion is vital to avoid unnecessary tax liabilities.

Lastly, not obtaining the necessary authorized signature from the employer is a common oversight. This signature is required to validate the information provided on the form. Without it, the form may be deemed incomplete, leading to further complications. Always ensure that the form is signed and dated by an authorized representative of the employer before submission.

What is the NJ-2440 form used for?

The NJ-2440 form is a statement that supports the exclusion of amounts received by employees under accident and health insurance plans for personal injuries or sickness from taxable gross income in New Jersey. It is essential for employees who have received such payments to ensure they are not taxed on these amounts, provided they meet specific criteria outlined by the state.

Who needs to fill out the NJ-2440 form?

Employees who have received payments through an accident or health insurance plan for personal injuries or sickness should fill out the NJ-2440 form. This includes those who have been absent from work due to injury or illness and have received compensation for wage loss under a qualifying insurance plan.

What criteria must be met for the exclusion from taxable gross income?

To qualify for the exclusion, the payments must meet three criteria: they must compensate for wage loss due to absence from work caused by injury or sickness, they must be under an enforceable contractual obligation, and they must not relate to sick leave that is discretionary. Payments made for the first seven days of absence may not qualify if they are at the employer's discretion.

Are there any exceptions to the withholding of gross income tax on these payments?

Yes, there are exceptions. Payments required under the State's temporary disability benefit plan, as well as those made under a private plan approved by the state, are exempt from gross income tax withholding. Additionally, payments from commercial insurance companies for personal injuries or sickness are also excluded from withholding.

What should employees do with the NJ-2440 form once completed?

Once the NJ-2440 form is completed, employees must file it with their annual New Jersey Gross Income Tax Return. This ensures that the amounts received under the accident or health insurance plan are officially recognized for exclusion from taxable gross income.

What happens if the criteria for exclusion are not met?

If the criteria for exclusion are not met, the payments received will be subject to tax as wages and salaries. Employers are required to withhold gross income tax on such payments. It is crucial for employees to understand these criteria to avoid unexpected tax liabilities.

Misconceptions about the NJ 2440 form can lead to confusion and potential tax issues. Understanding these misconceptions is crucial for both employees and employers. Here are eight common misunderstandings:

By dispelling these misconceptions, employees and employers can better navigate the complexities of the NJ 2440 form and ensure compliance with New Jersey tax laws.

The NJ-2440 form shares similarities with the W-2 form, which is used by employers to report wages paid to employees and the taxes withheld from those wages. Both documents serve as crucial components in the tax reporting process. The NJ-2440 focuses specifically on amounts received under accident and health insurance plans for personal injuries or sickness, while the W-2 provides a broader overview of an employee's earnings and tax withholdings. Both documents ensure that employees accurately report their income and understand the tax implications of their earnings.

Another document comparable to the NJ-2440 is the 1099 form, which reports income received by independent contractors and freelancers. While the NJ-2440 pertains to specific payments related to health insurance, the 1099 form captures various types of income outside of traditional employment. Both forms are essential for tax purposes, allowing individuals to report income correctly and claim any applicable exclusions or deductions, ensuring compliance with tax laws.

The NJ-2440 form is also similar to the IRS Form 8853, which is used to report Health Savings Accounts (HSAs). Both documents deal with health-related financial matters, but the NJ-2440 focuses on income received from insurance for personal injuries or sickness, while Form 8853 pertains to contributions and distributions from HSAs. Each form helps taxpayers navigate the complexities of health-related financial benefits and their tax implications.

In addition, the NJ-2440 bears resemblance to the Short-Term Disability Claim Form, which employees use to request benefits during a temporary disability. Both documents require detailed information about the employee's condition and the duration of the absence. While the NJ-2440 emphasizes tax exclusions for received payments, the Short-Term Disability Claim Form focuses on the approval and disbursement of benefits, ensuring employees receive the necessary financial support during their recovery.

To ensure a proper transfer of ownership during vehicle transactions, it's essential to have all relevant documentation in order, including a valid bill of sale. The Pennsylvania Motor Vehicle Bill of Sale form serves as a key document in this process, acting as proof of purchase and containing vital details about the vehicle and the parties involved. For those looking for a reliable template, the PDF Document Service offers an accessible solution that simplifies the drafting of this important legal document.

The NJ-2440 form is akin to the FMLA Certification of Health Care Provider form. This form is used to certify the need for leave under the Family and Medical Leave Act. Both documents require verification of a medical condition, but the NJ-2440 centers on income exclusions related to health insurance payments. They both aim to protect employees' rights, ensuring they receive the benefits they are entitled to during times of illness or injury.

Another document that parallels the NJ-2440 is the State Disability Insurance (SDI) claim form. This form is used to apply for state disability benefits when an employee is unable to work due to a medical condition. Like the NJ-2440, the SDI claim form addresses the financial impact of health issues on employees. Both forms facilitate access to benefits that help alleviate the economic burden caused by illness or injury.

The NJ-2440 is also similar to the Employer's Quarterly Federal Tax Return (Form 941). This document is filed by employers to report income taxes, Social Security tax, and Medicare tax withheld from employee wages. While the NJ-2440 focuses on specific exclusions for health-related payments, both forms are integral to the overall tax compliance framework, ensuring that both employers and employees fulfill their tax obligations.

Additionally, the NJ-2440 has similarities with the COBRA Continuation Coverage Election Notice. This document informs employees about their rights to continue health insurance coverage after leaving employment. While the NJ-2440 deals with tax exclusions for health insurance payments, both documents address the importance of maintaining health coverage during periods of transition, ensuring employees remain informed about their options.

Lastly, the NJ-2440 can be compared to the Tax Return Preparation Checklist, which assists individuals in gathering necessary documents for filing their taxes. Both documents emphasize the importance of accurate reporting and provide guidance on what information is needed to comply with tax laws. While the NJ-2440 focuses on specific exclusions related to health insurance, the checklist serves as a comprehensive tool to ensure all relevant tax documents are prepared for filing.