Printable Nj 630 Form

Printable Nj 630 Form

| Fact Name | Details |

|---|---|

| Form Title | NJ-630 Application for Extension of Time to File |

| Governing Law | New Jersey Gross Income Tax Law |

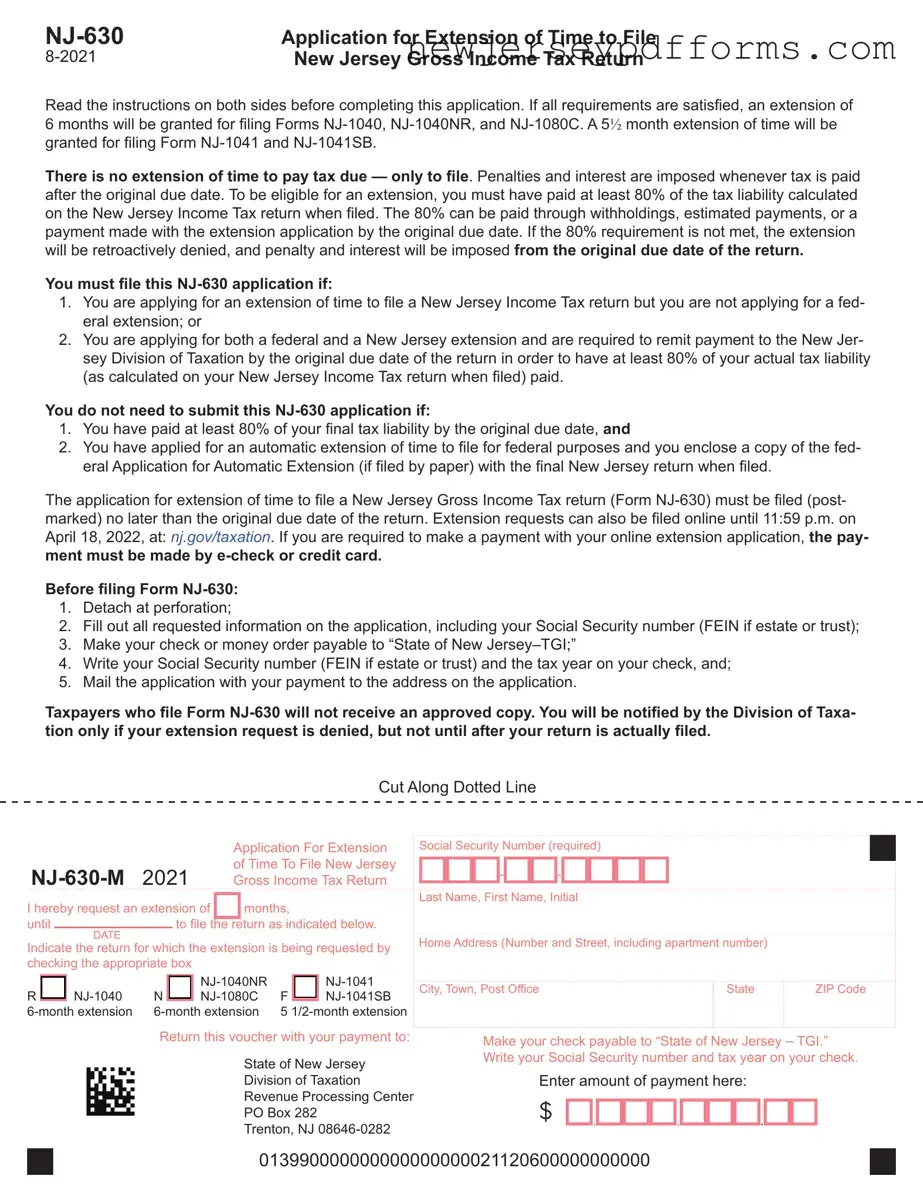

| Extension Duration | 6 months for Forms NJ-1040, NJ-1040NR, NJ-1080C; 5½ months for Forms NJ-1041 and NJ-1041SB. |

| Payment Requirement | Must pay at least 80% of the tax liability by the original due date to qualify for an extension. |

| Filing Deadline | Application must be postmarked by the original due date of the return. |

| Online Filing | Requests can be filed online until 11:59 p.m. on April 15, 2021. |

| Payment Methods | Payments can be made via e-check or credit card for online applications. |

| Notification of Approval | No approved copy will be sent; only denied requests will be notified. |

| Late Penalties | Penalties include 5% per month for late filing, up to 25%, and late payment penalties of 5% on any balance due. |

| Special Provisions | Military personnel may receive a 6-month extension by submitting a statement with their return. |

New Jersey Rules of Professional Conduct - In-kind contributions must be accounted for separately from monetary contributions for clarity.

New Jersey Department of the Treasury Division of Revenue and Enterprise Services - The form requires input of the city, state, and ZIP code.

In addition to understanding the importance of a Release of Liability form, individuals and organizations can benefit from accessing templates and guidance on how to create effective documents. Resources like PDF Document Service provide valuable tools to ensure that liability is appropriately addressed in various contexts, further safeguarding all parties involved.

Work in Nj Live in Pa Taxes - This form demonstrates your residency status and qualifies you for necessary exemptions.

Filling out the NJ-630 form can be straightforward, but many people make common mistakes that can lead to complications. One frequent error is failing to read the instructions carefully. The form includes essential guidelines on eligibility and payment requirements. Ignoring these instructions can result in a denied extension.

Another mistake is not paying the required 80% of the tax liability by the original due date. This is crucial for obtaining an extension. If this threshold is not met, the extension will be retroactively denied, and penalties will apply. It’s vital to ensure that your payment reflects this requirement.

Some individuals overlook the need to submit the NJ-630 application when applying for both federal and New Jersey extensions. If you are applying for a federal extension, you still need to file the NJ-630 if you have not paid at least 80% of your New Jersey tax liability. Failure to do so can complicate your tax situation.

Many people also forget to include their Social Security number or Federal Employer Identification Number (FEIN) on the form. This information is required and must be accurately provided to process the application. Omitting it can lead to delays or rejections.

Improper payment methods are another common pitfall. Payments must be made via check or money order, and they should be payable to “State of New Jersey–TGI.” Failing to follow these guidelines can result in processing issues.

Additionally, not mailing the application to the correct address can cause significant delays. Always double-check the mailing address listed on the form. Sending it to the wrong location can mean that your application is not received on time.

Another mistake involves not detaching the application at the perforation. This step is important for ensuring that your submission is processed correctly. Neglecting this can lead to confusion and possible rejection of your application.

Some taxpayers also misunderstand the timeline for filing. The NJ-630 must be postmarked by the original due date of the return. Missing this deadline means losing the opportunity for an extension, which can lead to penalties.

Lastly, individuals often overlook the fact that they will not receive an approved copy of the NJ-630 form. The Division of Taxation will only notify you if your request is denied. This can lead to uncertainty, so it’s crucial to keep your records organized and monitor your tax status after filing.

What is the NJ-630 form?

The NJ-630 form is an application for an extension of time to file a New Jersey Gross Income Tax Return. It allows taxpayers to request an extension of up to six months for certain tax forms, such as NJ-1040, NJ-1040NR, and NJ-1080C, and a 5½ month extension for Forms NJ-1041 and NJ-1041SB.

Who needs to file the NJ-630 form?

You need to file the NJ-630 form if you are applying for an extension to file a New Jersey Income Tax return without also applying for a federal extension. Additionally, if you are applying for both federal and New Jersey extensions, you must remit payment to the New Jersey Division of Taxation to ensure at least 80% of your tax liability is paid by the original due date.

What are the eligibility requirements for an extension?

To be eligible for an extension, you must pay at least 80% of your calculated tax liability by the original due date. This payment can be made through withholdings, estimated payments, or a payment included with your NJ-630 application. If you do not meet the 80% requirement, the extension will be denied retroactively, and penalties and interest will apply from the original due date.

When must the NJ-630 form be filed?

The NJ-630 form must be filed by the original due date of your New Jersey Income Tax return. This means it should be postmarked by that date. Alternatively, you can file online until 11:59 p.m. on the due date at www.njtaxation.org.

What payment methods are accepted with the NJ-630 form?

If you are submitting your NJ-630 application online, payments must be made via e-check or credit card. For paper submissions, you should include a check or money order made out to “State of New Jersey–TGI.” Ensure that your Social Security number and the tax year are written on the payment.

Will I receive confirmation of my extension request?

No, taxpayers who file the NJ-630 form will not receive an approved copy. The New Jersey Division of Taxation will only notify you if your extension request is denied, and this notification will occur after your return has been filed.

What happens if I do not file my return by the extended due date?

If your final return is not received by the extended due date, penalties and interest will be applied as if the extension had not been granted. Late filing penalties can reach up to 25% of the tax due, and interest will accrue at a rate of 3 percentage points above the prime rate for each month the tax remains unpaid.

Are there special provisions for military personnel regarding the NJ-630 form?

Yes, individuals in active service with the Armed Forces of the United States who are unable to file due to distance, injury, or hospitalization will automatically receive a six-month extension. They must include a statement explaining the reason for the extension with their return.

Misconceptions about the NJ-630 Form

The NJ-630 form serves as an application for an extension of time to file a New Jersey Gross Income Tax return. Similarly, the IRS Form 4868 allows taxpayers to request an automatic extension for filing their federal income tax returns. Both forms require taxpayers to estimate their tax liability and pay a portion by the original due date to qualify for the extension. While the NJ-630 grants a six-month extension for state returns, the IRS form typically allows for a six-month extension for federal returns as well. However, just like the NJ-630, the federal extension does not apply to the payment of taxes due, which must still be paid by the original deadline to avoid penalties and interest.

Another document that is comparable is the New Jersey Form NJ-1040, which is the actual income tax return form for residents. While the NJ-630 is solely for requesting an extension, the NJ-1040 is where taxpayers report their income, deductions, and calculate their tax liability. Both forms are interconnected; if a taxpayer files an NJ-630 to extend their filing deadline, they will ultimately need to complete and submit the NJ-1040 by the extended due date. This relationship highlights the importance of understanding both forms in the context of New Jersey tax obligations.

The IRS Form 7004 is another document that parallels the NJ-630 form, as it is used to request an extension for certain business tax returns. Just like the NJ-630, Form 7004 requires the taxpayer to pay a portion of their estimated tax liability by the original due date. Both forms serve to provide additional time for taxpayers to file their returns, but they cater to different types of taxpayers—individuals for NJ-630 and businesses for Form 7004. This distinction emphasizes the need for business owners to be aware of their specific requirements when it comes to filing extensions.

For those navigating healthcare decisions, understanding the importance of a Living Will form for healthcare decisions can provide vital guidance in ensuring your medical preferences are honored when you cannot communicate them yourself.

The New Jersey Form NJ-1041 is also similar to the NJ-630, as it pertains to fiduciary income tax returns for estates and trusts. Taxpayers can apply for an extension using the NJ-630 if they need more time to file the NJ-1041. Both forms include provisions for the payment of estimated tax liabilities, and both require that a certain percentage of tax be paid by the original due date to avoid penalties. Understanding the connection between these forms is crucial for trustees and executors managing tax responsibilities for estates.

Form NJ-1041SB, which is specifically for New Jersey S corporations, is another document that shares similarities with the NJ-630. Just like the NJ-1041, the NJ-1041SB can also be extended using the NJ-630 form. Both forms require that a significant portion of the estimated tax liability be paid by the original due date to qualify for the extension. This relationship is particularly important for business owners who must navigate both corporate and personal tax obligations.

The IRS Form 8868 is similar to the NJ-630 in that it allows for an extension of time to file certain tax-exempt organization returns. Both forms require the payment of estimated tax liabilities to qualify for the extension. While the NJ-630 is focused on individual and fiduciary tax returns in New Jersey, Form 8868 specifically caters to organizations, highlighting the different contexts in which extensions can be applied for but maintaining the same underlying principles regarding tax payments.

Form NJ-1080C, which is used for New Jersey's gross income tax for non-residents, is another relevant document. Like the NJ-630, the NJ-1080C can be extended using the same application process. Both forms require the payment of estimated tax by the original due date to avoid penalties. This similarity is crucial for non-residents who may have different tax obligations but still need to adhere to the same principles of timely payment and filing.

Lastly, the IRS Form 1040-ES is related to the NJ-630 as it is used for estimating and paying quarterly taxes for individuals. While it serves a different purpose—primarily for estimated tax payments rather than extensions—both forms emphasize the importance of timely payment to avoid penalties. Understanding how these forms interact can help taxpayers manage their financial responsibilities effectively, ensuring compliance with both state and federal tax laws.