Printable Nj 927 W Form

Printable Nj 927 W Form

| Fact Name | Details |

|---|---|

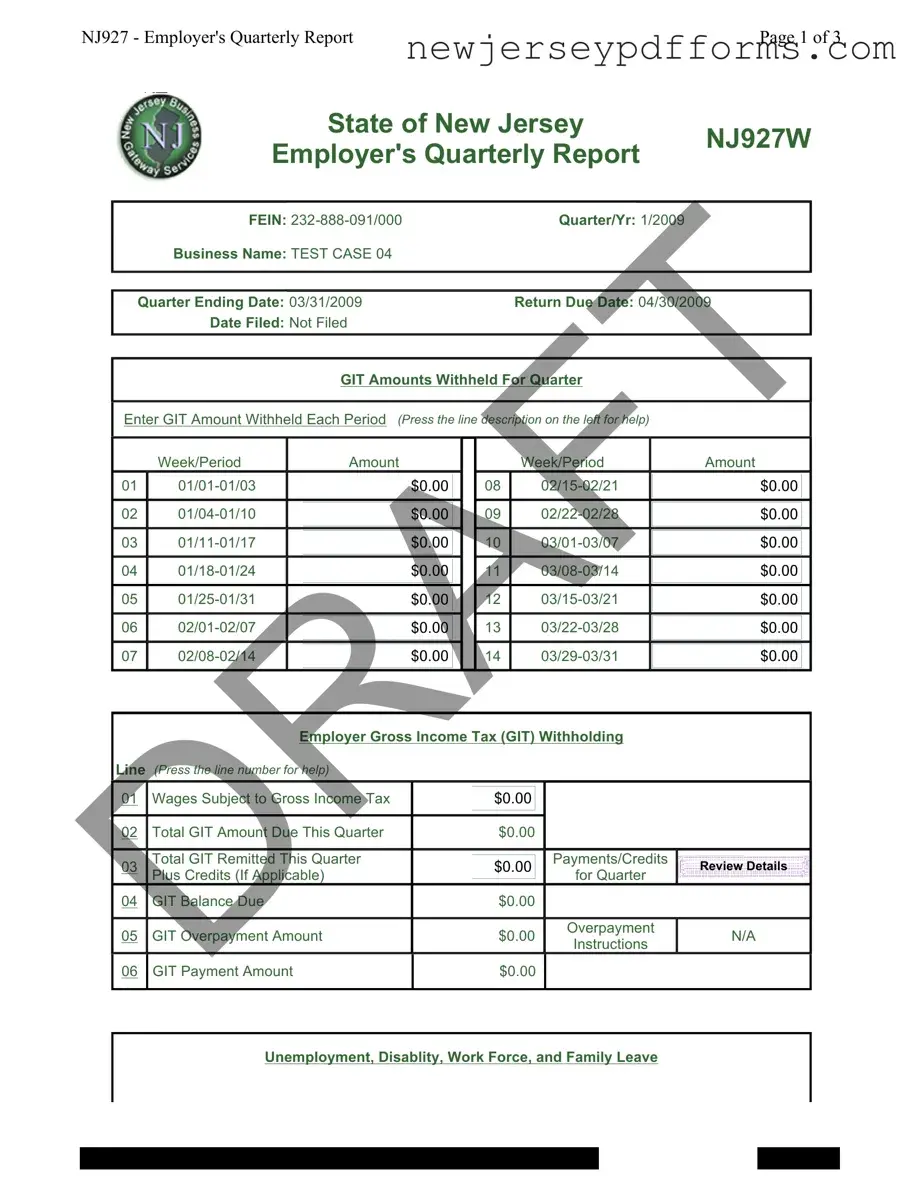

| Form Purpose | The NJ927W form is used for reporting employer's quarterly gross income tax withholding in New Jersey. |

| Filing Frequency | Employers must file this form quarterly, covering all employees for the specified quarter. |

| Due Date | The return is due on the last day of the month following the end of the quarter. |

| GIT Withholding | Employers report the Gross Income Tax (GIT) withheld from employee wages on this form. |

| Employer Identification | Each form includes the Federal Employer Identification Number (FEIN) for accurate identification. |

| Quarterly Reporting | The form requires reporting for each week of the quarter, detailing amounts withheld. |

| Governing Law | This form is governed by the New Jersey Gross Income Tax Act. |

| Payment Information | Employers must indicate any payments made towards GIT and other contributions on the form. |

| Employee Count | The form requires the count of full-time and part-time workers covered during the reporting period. |

| Overpayment Handling | If applicable, the form allows for reporting of GIT overpayments and requesting refunds. |

Nj-500 - Any amendments to the Lease require both parties' consent to be valid.

Dba in Nj - The form can be submitted either by mail or via fax for expedited processing.

A Release of Liability form is a legal document that helps protect an organization or individual from claims resulting from accidents or injuries that may occur during a specific activity. By signing this form, participants acknowledge the inherent risks involved and relinquish their right to hold the facilitator responsible. Understanding this form is crucial for anyone engaged in activities where accidents are a possibility, and you can find a useful template at PDF Document Service.

What Is a Sales Agreement - Closing dates can be adjusted as needed, especially with financing stipulations.

Filling out the NJ 927 W form can be a daunting task for many employers. One common mistake is failing to accurately report the amounts withheld for each pay period. Employers may overlook or miscalculate the amounts, leading to discrepancies that can result in penalties. It is essential to ensure that the amounts reported match the payroll records for each week or period.

Another frequent error involves the incomplete reporting of employee wages. Employers sometimes forget to include all wages subject to Gross Income Tax, or they may misclassify certain payments. This can lead to underreporting, which may trigger audits or additional tax liabilities. Accurate reporting of all wages is crucial for compliance.

Many employers also struggle with the timeliness of filing. The due date for the NJ 927 W form is often overlooked, leading to late submissions. Late filings can incur penalties and interest charges. It is advisable to set reminders well in advance of the due date to ensure timely submission.

Additionally, some employers make the mistake of not reviewing the instructions carefully. The NJ 927 W form comes with specific guidelines that must be followed. Ignoring these instructions can lead to errors that complicate the filing process. Taking the time to read and understand the instructions can save employers from unnecessary headaches.

Finally, a lack of attention to payment information can cause issues. Employers may incorrectly report payment amounts or fail to account for credits and overpayments. This can create confusion regarding the actual balance due. Ensuring that all payment details are accurate is vital for maintaining good standing with tax authorities.

What is the NJ 927 W form?

The NJ 927 W form, also known as the Employer's Quarterly Report, is a document that employers in New Jersey must file to report wages paid to employees and the associated taxes withheld. This form is crucial for ensuring compliance with state tax laws, including the Gross Income Tax (GIT) and other contributions related to unemployment and disability insurance. It provides a summary of the employer's payroll activities for a specific quarter.

When is the NJ 927 W form due?

The NJ 927 W form is due on the last day of the month following the end of the quarter. For example, if the quarter ends on March 31, the form must be filed by April 30. Timely submission is essential to avoid penalties and interest on any unpaid taxes.

How do I complete the NJ 927 W form?

To complete the NJ 927 W form, employers must provide information about the wages paid during the quarter, the number of employees, and the taxes withheld. Each line of the form corresponds to specific data that needs to be filled out. Employers should ensure accuracy by double-checking figures and ensuring that all required sections are completed. Guidance is often available on the form itself, providing assistance for each line item.

What happens if I do not file the NJ 927 W form on time?

If the NJ 927 W form is not filed by the due date, employers may face penalties and interest on any outstanding tax amounts. The state may also take enforcement actions, which could include withholding future tax refunds or taking legal action to recover unpaid taxes. It is always best to file on time or to contact the state for assistance if there are difficulties in meeting the deadline.

Can I amend my NJ 927 W form after it has been filed?

Yes, if an employer discovers an error after filing the NJ 927 W form, it is possible to amend the form. This can typically be done by submitting a corrected form to the state, along with an explanation of the changes. It is important to address any discrepancies as soon as possible to avoid potential penalties or issues with tax compliance.

Where can I find assistance with the NJ 927 W form?

Assistance with the NJ 927 W form can be found through the New Jersey Division of Taxation's website. They provide resources, including guides and contact information for customer service. Additionally, employers may seek help from tax professionals who are familiar with state tax regulations to ensure accurate completion and compliance.

The NJ 927 W form is essential for employers in New Jersey to report their Gross Income Tax (GIT) withholdings. However, several misconceptions surround this form. Below are ten common misunderstandings, along with clarifications to help you navigate the requirements effectively.

Understanding these misconceptions can help ensure compliance and avoid potential issues with the New Jersey Division of Taxation. Always consult with a tax professional if you have specific questions or concerns regarding your obligations.

The NJ-927W form is closely related to the IRS Form 941, which is used by employers to report income taxes withheld from employee wages and the employer's portion of Social Security and Medicare taxes. Both forms serve as crucial quarterly reports for employers, detailing the amounts withheld from employees' paychecks. While the NJ-927W focuses on New Jersey's Gross Income Tax, Form 941 addresses federal income tax withholding. Employers must file both forms to ensure compliance with state and federal tax laws, making them essential tools for accurate payroll reporting.

A Pennsylvania Bill of Sale form is crucial for documenting the transfer of ownership of personal property, ensuring both the buyer and seller are protected during transactions. This form outlines important details such as the identities of involved parties, a description of the item sold, and the agreed sale price. For those seeking a reliable template to facilitate this process, visit topformsonline.com/pennsylvania-bill-of-sale for a comprehensive resource.

Another document similar to the NJ-927W is the NJ-1080C, the New Jersey Employer's Annual Report of Wages Paid. While the NJ-927W is a quarterly report, the NJ-1080C is filed annually and summarizes the total wages paid to employees throughout the year. Both documents require employers to provide information about wages and taxes withheld, ensuring that the state has an accurate record of employee compensation. This annual report complements the quarterly filings, allowing for a comprehensive view of an employer’s payroll obligations over time.

The NJ-927W also shares similarities with the IRS Form 940, which is the Employer's Annual Federal Unemployment (FUTA) Tax Return. Like the NJ-927W, Form 940 requires employers to report specific tax amounts related to their employees. While the NJ-927W deals with state-level taxes, Form 940 focuses on federal unemployment taxes. Employers must file both forms to remain compliant with their tax responsibilities, ensuring that they are contributing appropriately to unemployment insurance programs at both state and federal levels.

Lastly, the NJ-927W can be compared to the W-2 form, which reports annual wages and tax withholdings for individual employees. While the NJ-927W provides a broader overview of an employer’s tax obligations for a specific quarter, the W-2 form is more focused on individual employee earnings and taxes withheld. Both documents are vital for accurate tax reporting, as the information from the NJ-927W ultimately feeds into the annual W-2 forms that employers provide to their employees for tax filing purposes. Together, they help maintain transparency and compliance in the employer-employee tax relationship.