Printable Nj A 3128 Form

Printable Nj A 3128 Form

| Fact Name | Description |

|---|---|

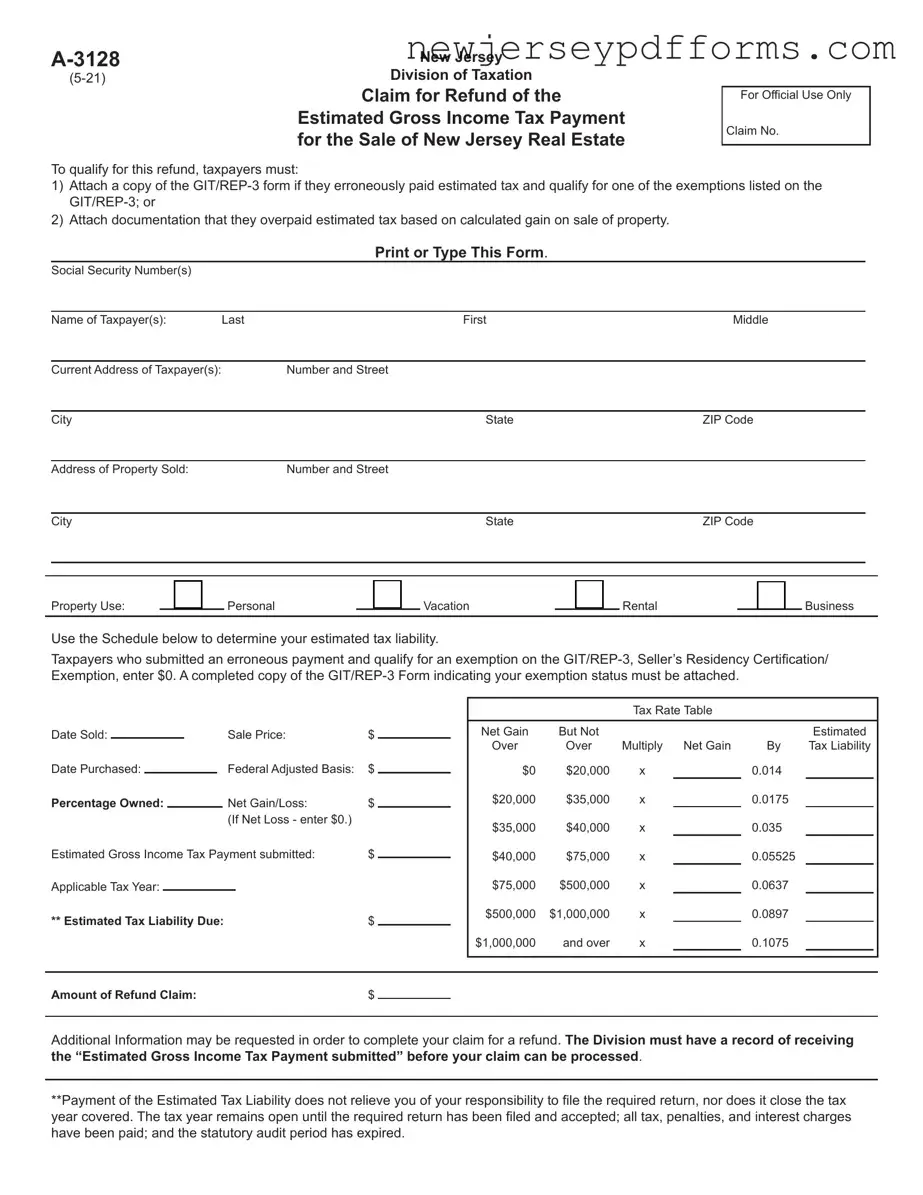

| Purpose | The NJ A-3128 form is used to claim a refund for the estimated Gross Income Tax payment made during the sale of New Jersey real estate. |

| Eligibility | Taxpayers must attach the GIT/REP-3 form if they mistakenly paid estimated tax or provide proof of overpayment based on the gain from the property sale. |

| Governing Law | This form is governed by New Jersey Statutes Annotated (N.J.S.A.) 54A:8-8 through 54A:8-10, which outline the regulations for estimated tax payments and refunds. |

| Submission Requirements | To complete the claim, include your current address, property details, sale information, and the estimated tax liability calculated using the provided tax rate table. |

| Processing Time | The Division of Taxation must have a record of the estimated tax payment before processing the refund claim. Incomplete claims will be returned. |

| Agent Representation | If someone other than the taxpayer prepares the form, an Appointment of Taxpayer Representative must be included to authorize that individual. |

How to File for Child Support New Jersey - The option to release the form to WIC is also available for families who need nutrition assistance.

To ensure that the transfer of ownership is documented correctly, it is advisable to use a thorough Horse Bill of Sale document that delineates all necessary details of the transaction. For more information, visit the comprehensive Horse Bill of Sale guide.

Nj Sales Tax Certificate of Authority - This form helps sellers verify that buyers are allowed to make tax-exempt purchases for resale purposes.

Filling out the New Jersey A-3128 form can be a straightforward process, but there are common mistakes that can lead to delays or rejections. One frequent error is failing to attach the necessary documentation. Taxpayers must include a copy of the GIT/REP-3 form if they qualify for an exemption or provide proof of overpayment based on the sale's calculated gain. Omitting these documents can cause the claim to be deemed incomplete.

Another mistake involves incorrect or missing information in the taxpayer's details. It is essential to provide accurate names, Social Security numbers, and current addresses. Any discrepancies can lead to confusion and may result in the claim being returned. Additionally, not specifying the property address or the amount of the refund being requested can also hinder the processing of the claim.

Many people overlook the importance of calculating the estimated tax liability correctly. The form includes a tax rate table to assist in this calculation. If the estimated tax liability is not computed accurately, it could lead to incorrect refund amounts. This mistake not only affects the claim but may also complicate future tax filings.

Another common oversight is not signing the form. Under penalties of perjury, the taxpayer must declare that the information provided is true and complete. Without a signature, the claim cannot be processed. This requirement emphasizes the importance of reviewing the form before submission.

Lastly, some individuals fail to mail the claim to the correct address or do not include the required Settlement Statement or Closing Disclosure form. Sending the claim to the wrong location can delay the refund process significantly. It is crucial to double-check the mailing address and ensure all necessary documents are included to avoid unnecessary complications.

What is the NJ A-3128 form used for?

The NJ A-3128 form is used to claim a refund of the estimated Gross Income Tax payment made for the sale of New Jersey real estate. Taxpayers, including nonresident individuals, estates, or trusts, can use this form to request a refund if they have overpaid their estimated tax based on the gain from the sale of property.

Who is eligible to file the NJ A-3128 form?

Eligibility to file the NJ A-3128 form includes nonresident individuals, estates, or trusts that have made an estimated Gross Income Tax payment when selling New Jersey real estate. To qualify for a refund, taxpayers must either attach a GIT/REP-3 form showing an exemption or provide documentation that demonstrates an overpayment based on the calculated gain from the sale.

What documentation must be submitted with the NJ A-3128 form?

When submitting the NJ A-3128 form, taxpayers must include a copy of the GIT/REP-3 form if they qualify for an exemption. Alternatively, they must provide documentation that supports their claim of overpayment based on the gain from the property sale. Additionally, a Settlement Statement (HUD-1) or Closing Disclosure form must be attached.

How is the estimated tax liability calculated on the NJ A-3128 form?

Taxpayers must use the tax rate table provided on the form to calculate their estimated tax liability. This involves determining the net gain or loss from the sale of the property and applying the appropriate tax rate based on the amount of gain. Taxpayers who qualify for an exemption should enter $0 for their estimated tax liability.

What should be done if the form is prepared by someone other than the taxpayer?

If the NJ A-3128 form is prepared by an individual other than the taxpayer, an Appointment of Taxpayer Representative must be included. This document authorizes the representative to act on behalf of the taxpayer in matters related to the claim for a refund.

What happens if the form is incomplete or lacks required documentation?

Incomplete claims or those lacking required documentation will be rejected. The New Jersey Division of Taxation will return such claims. It is crucial to ensure that all required lines on the form are filled out and that necessary documentation is attached to avoid delays in processing the refund.

Where should the completed NJ A-3128 form be mailed?

The completed NJ A-3128 form, along with the required attachments, should be mailed to the New Jersey Division of Taxation, Taxpayer Accounting Branch, P.O. Box 046, Trenton, NJ 08646-0046. Timely submission is important to ensure the claim is processed efficiently.

Does submitting the NJ A-3128 form eliminate the need to file a tax return?

No, submitting the NJ A-3128 form does not eliminate the requirement to file the necessary tax return. Taxpayers remain responsible for filing the required return, and the tax year will remain open until the return is filed and accepted, all taxes and penalties are paid, and the statutory audit period has expired.

The NJ A-3128 form is a critical document for taxpayers seeking a refund of estimated gross income tax payments related to the sale of New Jersey real estate. However, several misconceptions can lead to confusion and potential errors in the filing process. Below are five common misconceptions regarding this form.

This is incorrect. The form can be filed by nonresident individuals, estates, or trusts. Homeownership is not a prerequisite for submitting a claim.

This is misleading. Taxpayers must attach a copy of the GIT/REP-3 form if they qualify for an exemption or provide documentation showing an overpayment of estimated tax based on the sale of the property.

This is false. Payment of the estimated tax liability does not close the tax year. The tax year remains open until all required returns are filed, accepted, and all tax obligations are settled.

This is incorrect. Separate forms must be used for each taxpayer, except for married couples filing jointly. This ensures that each claim is processed accurately.

This is misleading. A completed GIT/REP-3 form indicating exemption status must be attached if you are claiming an exemption. Failure to do so may result in the claim being rejected.

Understanding these misconceptions is crucial for ensuring a smooth and successful filing process for the NJ A-3128 form. Taxpayers should take the time to review the requirements carefully and gather all necessary documentation to avoid delays or rejections of their claims.

The New Jersey GIT/REP-3 form is closely related to the NJ A-3128 form. It serves as a Seller’s Residency Certification/Exemption, allowing sellers to certify their residency status when selling real estate in New Jersey. Taxpayers who qualify for exemptions listed on the GIT/REP-3 can use this form to avoid unnecessary estimated gross income tax payments. The GIT/REP-3 must be attached to the A-3128 form when claiming a refund for overpaid estimated taxes, ensuring a streamlined process for those eligible for a refund based on their residency status.

The IRS Form 1040, U.S. Individual Income Tax Return, is another document that shares similarities with the NJ A-3128 form. While the A-3128 focuses specifically on claiming a refund for estimated gross income tax payments related to real estate transactions, the Form 1040 is a comprehensive tax return used by individuals to report their annual income. Both forms require taxpayers to provide detailed financial information, including income and deductions, to calculate tax liabilities. This connection highlights the importance of accurately reporting financial data for tax purposes.

The IRS Form 1099-S, Proceeds from Real Estate Transactions, is also relevant to the NJ A-3128 form. This form is issued to report the proceeds from the sale of real estate, which is crucial for determining any capital gains or losses. When completing the NJ A-3128, taxpayers may need to refer to the information on their 1099-S to accurately report the sale price and calculate their net gain or loss. The relationship between these forms underscores the need for transparency in real estate transactions.

The New Jersey GIT/REP-4 form is another document that bears resemblance to the NJ A-3128 form. This form is used to claim a refund of the gross income tax for nonresidents who sold property in New Jersey. However, it is important to note that the GIT/REP-4 should not be used to claim a refund in conjunction with the A-3128. The distinction between these two forms is critical, as using the wrong form can lead to complications in the refund process.

The New Jersey Property Tax Reimbursement Application (Form PTR-1) also relates to the NJ A-3128 form in the context of property ownership. While the A-3128 focuses on refunds related to income tax from property sales, the PTR-1 is designed for senior citizens and disabled persons to claim reimbursement for property taxes paid. Both forms require detailed information about property ownership and financial circumstances, emphasizing the importance of accurate documentation in tax-related matters.

The New Jersey Division of Taxation’s Form NJ-1040NR is relevant for nonresidents who earn income in New Jersey. Similar to the NJ A-3128, this form is used by individuals who are not residents but have tax obligations due to income generated within the state. Both forms require careful calculations of income and potential tax liabilities, illustrating the complexities of tax obligations for nonresidents.

The IRS Form 8949, Sales and Other Dispositions of Capital Assets, is another document that shares similarities with the NJ A-3128 form. This form is used to report capital gains and losses from the sale of assets, including real estate. Taxpayers must accurately report their net gain or loss from property sales on both the A-3128 and Form 8949, ensuring consistency in their financial reporting across state and federal levels.

The New Jersey Division of Taxation's Form NJ-1040 is also similar to the NJ A-3128 form, as both forms are used by New Jersey taxpayers to report income and calculate tax liabilities. While the NJ A-3128 specifically addresses refunds for estimated gross income tax payments related to real estate transactions, the NJ-1040 encompasses a broader scope of income reporting. Both forms require taxpayers to provide detailed financial information, reinforcing the importance of accurate reporting in tax compliance.

When dealing with legal and financial matters, having the right documents is crucial, especially when it comes to delegating authority through tools like a Power of Attorney. This form not only empowers someone to make decisions on your behalf but also ensures that your specific wishes are followed in your absence. For those looking to understand and utilize this document effectively, resources such as PDF Document Service can provide valuable templates and guidance.

Lastly, the New Jersey Division of Taxation's Form NJ-1065 is relevant for partnerships and multi-member LLCs. This form is used to report income, deductions, and credits for partnerships operating in New Jersey. While the NJ A-3128 is focused on individual taxpayers claiming refunds for overpaid estimated taxes, both forms necessitate precise financial reporting and compliance with state tax regulations. Understanding the connections between these forms can help taxpayers navigate their obligations more effectively.