Printable Nj Cbt 2553 R Form

Printable Nj Cbt 2553 R Form

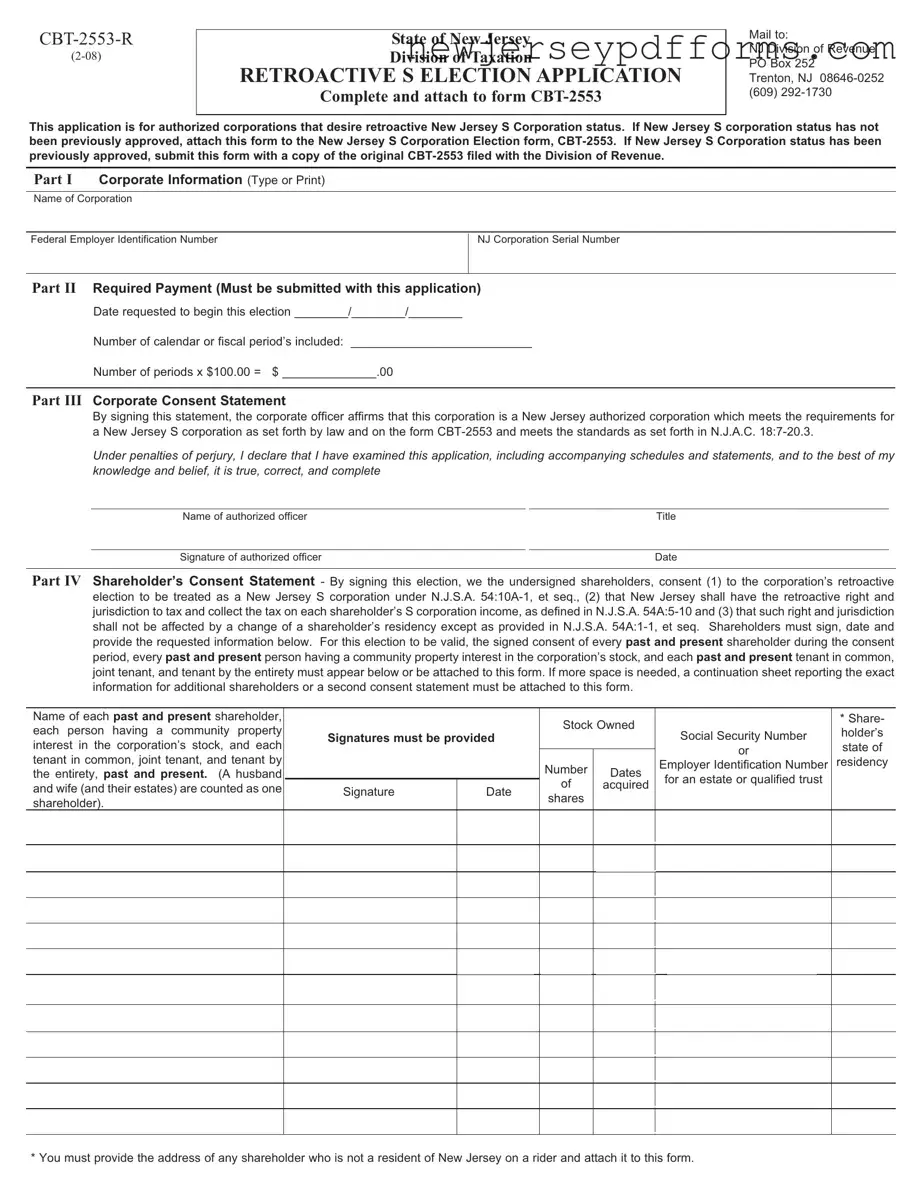

| Fact Name | Details |

|---|---|

| Form Purpose | This form is used by authorized corporations to apply for retroactive New Jersey S Corporation status. |

| Governing Law | The application is governed by N.J.S.A. 54:10A-1, et seq. and N.J.A.C. 18:7-20.3. |

| Filing Requirement | Corporations must attach CBT-2553 if New Jersey S Corporation status was not previously approved. |

| Payment Requirement | A non-refundable fee of $100 must accompany the application for each year affected. |

| Signature Requirement | The corporate officer must sign the application, affirming compliance with New Jersey S corporation requirements. |

| Shareholder Consent | All past and present shareholders must consent to the retroactive election for it to be valid. |

| Mailing Address | Completed forms should be mailed to NJ Division of Revenue, PO Box 252, Trenton, NJ 08646-0252. |

| Review Process | After submission, the taxpayer will be notified if the retroactive election is granted. |

| Eligibility Criteria | Corporations must have timely filed tax returns and paid taxes as if the S corporation election had been approved. |

Accuwage Online - Employers can find further details by contacting the New Jersey Division of Taxation.

New Jersey D 3 - Committee address, telephone numbers, and county municipality must be provided.

In order to effectively safeguard against potential legal claims, utilizing a Release of Liability form is essential for organizations and individuals alike. This document not only clarifies the risks associated with specific activities but also ensures that participants are aware of these risks and agree not to hold the facilitator responsible for any accidents or injuries. For further assistance in creating such documents, you can refer to PDF Document Service, which offers templates and guidance on this matter.

Bcbs Medical Claim Form - Ensure that all required fields are filled to avoid delays in processing.

Filling out the NJ CBT 2553 R form can be a complex task, and mistakes are common. One frequent error is not including the correct Federal Employer Identification Number (FEIN). This number is crucial for identifying the corporation and must match the one assigned by the Internal Revenue Service. Any discrepancies can lead to delays or even denials of the application.

Another common mistake involves the payment requirement. Each year or privilege period for which retroactive status is requested requires a non-refundable payment of $100. Failing to include this payment or miscalculating the total can result in the application being rejected outright. It is essential to double-check the number of periods being requested and ensure the correct payment is submitted.

In Part III of the form, the Corporate Consent Statement must be signed by an authorized corporate officer. A mistake often made is having a different officer sign the CBT-2553 and the CBT 2553 R forms. Both documents must be signed by the same individual to avoid complications.

Another oversight occurs in Part IV, where all shareholders must consent to the retroactive election. Many applicants forget to include signatures from all past and present shareholders, which is a requirement for the election to be valid. If any shareholder is missing, the application may be deemed incomplete.

Additionally, some people fail to provide the necessary information regarding shareholders who are not residents of New Jersey. The form specifically states that an address for non-resident shareholders must be attached. Neglecting this requirement can lead to processing delays.

Another mistake is not following the instructions carefully, particularly regarding the name of the corporation. The name must be typed or printed exactly as it appears on other official documents, such as form NJ-REG. Any variations can cause confusion and may result in the rejection of the application.

Some applicants also overlook the importance of including a copy of the original CBT-2553 if New Jersey S Corporation status was previously approved. This omission can lead to unnecessary complications and delays in processing the application.

Moreover, failing to provide the correct date for when the retroactive election is requested can lead to issues. The date must be clearly indicated, and any ambiguity can cause confusion during the review process.

Lastly, many individuals do not take the time to review the entire application for accuracy before submission. Simple typographical errors or missing information can lead to significant setbacks. Thoroughly reviewing the form can help catch these mistakes before they become problems.

What is the purpose of the NJ CBT 2553 R form?

The NJ CBT 2553 R form is an application for corporations in New Jersey that wish to obtain retroactive S Corporation status. This form is essential for those corporations that either have not previously been approved for S Corporation status or need to amend their status retroactively. By completing this form, corporations can align their tax treatment with their intended classification, allowing them to benefit from the advantages associated with S Corporations in New Jersey.

Who is eligible to file the NJ CBT 2553 R form?

Only authorized corporations that are registered to do business in New Jersey can file this form. To qualify, the corporation must have filed New Jersey tax returns as an S Corporation in the past but failed to submit a timely election request. Additionally, all shareholders must consent to the retroactive election, which means that every past and present shareholder must sign the form or provide consent on an attached sheet.

What information is required on the NJ CBT 2553 R form?

The form requires several key pieces of information. Corporations must provide their name, Federal Employer Identification Number (FEIN), and New Jersey Corporation Serial Number. Additionally, they must indicate the desired effective date for the election and include the number of periods affected by the retroactive election, along with the appropriate payment. A corporate officer must also sign a consent statement affirming the corporation's eligibility for S Corporation status.

What is the payment requirement associated with the NJ CBT 2553 R form?

When submitting the NJ CBT 2553 R form, a non-refundable payment of $100 is required for each tax year or privilege period for which retroactive status is being requested. This payment must accompany the application to ensure that it is processed. Failure to include the payment may result in the application being deemed incomplete and not considered.

What happens after submitting the NJ CBT 2553 R form?

Once the completed form and payment are submitted to the New Jersey Division of Revenue, the application will be reviewed. The corporation will receive notification regarding the approval or denial of the retroactive election. If the election is granted, the corporation will be recognized as an S Corporation retroactively to the requested date, impacting the tax treatment of the corporation and its shareholders.

Are there any conditions that could prevent the approval of the NJ CBT 2553 R form?

Yes, several conditions could lead to the denial of the retroactive election. For example, if the corporation has not filed all required business tax returns on time or has not paid the appropriate taxes, the application may be rejected. Additionally, if an assessment against the corporation becomes final before the election request is received, it will not be granted. Shareholders must also have filed their tax returns correctly for the retroactive period; otherwise, the election may not be approved.

How can shareholders show their consent for the retroactive election?

Shareholders must sign the consent statement included in Part IV of the NJ CBT 2553 R form. This section requires the names, signatures, and other identifying information of all past and present shareholders, as well as those with community property interests in the corporation's stock. Each shareholder's consent is crucial for the application to be valid, and if more space is needed, a continuation sheet can be attached to provide the necessary information.

Understanding the NJ CBT 2553 R form can be challenging due to various misconceptions that circulate among corporations seeking retroactive S Corporation status in New Jersey. Here are some common misunderstandings, along with clarifications for each:

In reality, the NJ CBT 2553 R form must be submitted before an assessment becomes final. Timeliness is crucial to ensure the retroactive election is considered.

This form is designed for currently authorized corporations that have previously filed for S Corporation status but missed the deadline. It applies to those seeking retroactive recognition.

The fee is non-refundable, regardless of whether the retroactive election is granted or denied. It is important to be prepared for this expense when filing.

All shareholders, past and present, must sign the consent statement in Part IV for the election to be valid. This includes anyone with a community property interest in the corporation’s stock.

If New Jersey S Corporation status has not been previously approved, the NJ CBT 2553 must be submitted along with the CBT 2553 R form. This ensures that the application is complete and meets all necessary requirements.

Filing does not guarantee approval. The application will be reviewed, and the taxpayer will be notified if the retroactive election is granted based on compliance with all requirements.

To qualify for the retroactive election, all appropriate corporation business tax returns must have been filed timely and taxes paid as if the election had been previously approved.

The residency of shareholders is important. Non-resident shareholders must provide their addresses on a rider attached to the form to ensure proper processing.

By addressing these misconceptions, corporations can better navigate the complexities of the NJ CBT 2553 R form and enhance their chances of successfully obtaining retroactive S Corporation status.

The IRS Form 2553 is one of the primary documents similar to the NJ CBT-2553 R form. This federal form allows eligible corporations to elect S corporation status for federal tax purposes. Like the NJ CBT-2553 R, which is used for retroactive election in New Jersey, the IRS Form 2553 must be filed within a specific timeframe to ensure the election is effective for the desired tax year. Both forms require consent from shareholders, emphasizing the collaborative nature of corporate governance. The critical difference lies in jurisdiction; while the IRS form pertains to federal tax status, the NJ form focuses on state-level recognition and taxation.

Another related document is the New Jersey S Corporation Election form, CBT-2553. This form is used to initially elect S corporation status in New Jersey, similar to how the CBT-2553 R form serves to request retroactive status. Both forms require detailed corporate information and shareholder consent. However, the CBT-2553 is submitted when a corporation is seeking to establish its S corporation status for the first time, while the CBT-2553 R is specifically for those seeking to backdate that status to a prior date.

The IRS Form 1120S is another important document that shares similarities with the NJ CBT-2553 R. Form 1120S is the annual tax return that S corporations file with the IRS. Just as the CBT-2553 R is crucial for establishing a corporation's tax status retroactively, Form 1120S is essential for reporting income, deductions, and credits for the S corporation. Both forms are integral to ensuring compliance with tax obligations, albeit at different stages of the corporate tax process.

For those looking to clarify their future healthcare decisions, consider a comprehensive Living Will that details your choices. This document is essential for ensuring your healthcare preferences are honored when you cannot communicate them yourself. Learn more about this important process by visiting our Living Will form resources.

The New Jersey Corporation Business Tax Return, CBT-100S, is also closely related to the NJ CBT-2553 R. This form is used by S corporations to report their income and calculate the state taxes owed. The CBT-2553 R is necessary for establishing S corporation status retroactively, while the CBT-100S is used to fulfill tax reporting obligations once that status is granted. Both documents reflect the importance of accurate reporting and compliance with state tax laws.

Lastly, the Consent of Shareholders form is similar in function to the shareholder consent section of the NJ CBT-2553 R. This standalone document is often required when a corporation is making significant decisions that affect its structure or tax status. It ensures that all shareholders are in agreement, similar to how the NJ CBT-2553 R requires consent for the retroactive election. Both emphasize the need for transparency and agreement among shareholders when it comes to corporate governance and tax matters.