Printable Nj Estate Form

Printable Nj Estate Form

| Fact Name | Description |

|---|---|

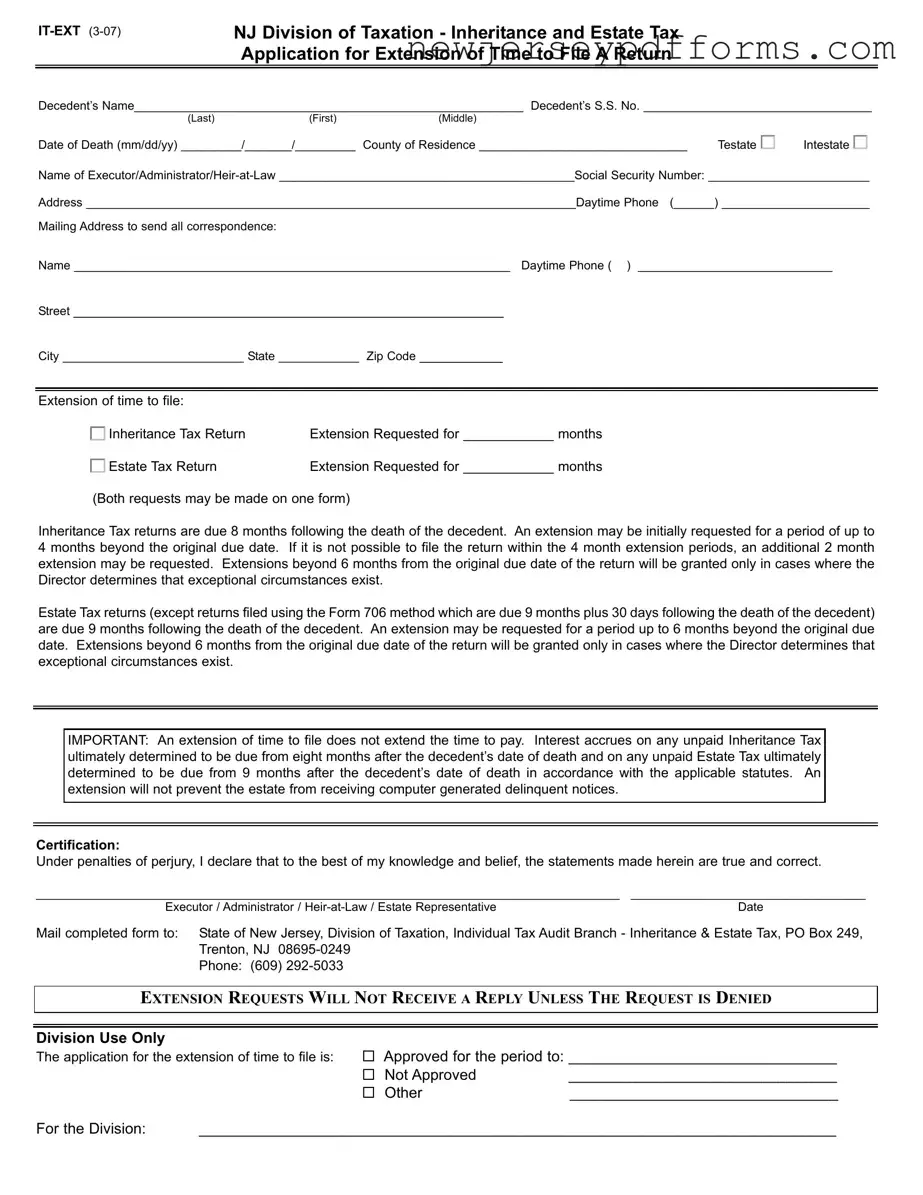

| Form Title | The form is officially titled "Inheritance and Estate Tax Application for Extension of Time to File A Return". |

| Governing Law | This form is governed by New Jersey Statutes Title 54, specifically related to inheritance and estate tax. |

| Decedent Information | The form requires the decedent's name, Social Security number, and date of death. |

| Executor Details | Information about the executor or administrator must be provided, including their name and Social Security number. |

| Filing Deadlines | Inheritance Tax returns are due 8 months after the decedent's death, while Estate Tax returns are due 9 months after. |

| Extension Periods | An initial extension of up to 4 months can be requested for Inheritance Tax returns, and up to 6 months for Estate Tax returns. |

| Interest Accrual | Interest on unpaid taxes begins accruing 8 months after the decedent's death for Inheritance Tax and 9 months for Estate Tax. |

| Certification Requirement | The form requires a certification statement under penalties of perjury, affirming the truthfulness of the information provided. |

Nj Certificate of Amendment Online - Each section of the form must be filled with precise information to avoid processing issues.

The Profit and Loss form is crucial for businesses, as it offers a comprehensive overview of income and expenditures within a defined timeframe. By utilizing essential tools like the PDF Document Service, companies can efficiently track their financial performance, enabling them to make well-informed decisions and strategize for future growth.

New Jersey Ppt 6 B - A well-completed form can pave the way for smoother operations and cost savings in petroleum dealings.

Imm-7 - Exemptions for the influenza vaccine may be granted based on medical or religious grounds.

Filling out the NJ Estate form can be a complex process, and mistakes can lead to delays or complications. Here are nine common errors people make when completing this form.

First, many individuals forget to include the decedent's full name and Social Security number. This information is crucial for identification purposes. Omitting it can result in the form being rejected or delayed.

Second, the date of death is often incorrectly formatted. The form requires a specific mm/dd/yy format. Failing to follow this format can create confusion and may lead to processing issues.

Another frequent mistake is not specifying whether the decedent was testate or intestate. This distinction is important for the estate's legal proceedings. Leaving this section blank can cause unnecessary complications.

People also sometimes neglect to provide the correct county of residence. This detail is necessary for tax jurisdiction and can affect how the estate is managed.

Additionally, the executor or administrator's information is sometimes incomplete. Not providing the full name, Social Security number, or contact information can hinder communication with the tax division.

Another common oversight is failing to indicate the correct length of the extension requested. The form allows for specific months to be filled in, and inaccuracies here can result in insufficient time being granted to file the necessary returns.

Some individuals mistakenly believe that an extension to file also extends the time to pay taxes owed. However, this is not the case. It is essential to understand that interest will accrue on unpaid taxes, regardless of the extension.

Moreover, many people do not keep a copy of the completed form for their records. This can be problematic if there are any disputes or questions about the submission in the future.

Finally, failing to sign and date the form can lead to automatic rejection. The certification section is vital, as it confirms the accuracy of the information provided.

By being aware of these common mistakes, individuals can better navigate the NJ Estate form process and ensure a smoother experience.

What is the NJ Estate form IT-EXT used for?

The NJ Estate form IT-EXT is an application for an extension of time to file inheritance and estate tax returns. It allows the executor, administrator, or heir-at-law to request additional time beyond the original due date to submit these tax returns following a decedent's death.

What are the due dates for inheritance and estate tax returns in New Jersey?

Inheritance tax returns are due 8 months after the decedent's date of death. Estate tax returns are generally due 9 months after the date of death. However, if the estate tax return is filed using the Form 706 method, it is due 9 months plus 30 days after the decedent's death.

How long can I request an extension for filing these tax returns?

For inheritance tax returns, you can request an initial extension of up to 4 months. If you still need more time, an additional 2-month extension may be requested, totaling a maximum of 6 months. For estate tax returns, you can request an extension of up to 6 months. Extensions beyond these periods are only granted in exceptional circumstances as determined by the Director.

Does requesting an extension change the deadline for paying taxes owed?

No, requesting an extension to file does not extend the time to pay any taxes owed. Interest begins to accrue on any unpaid inheritance tax 8 months after the decedent's death and on estate tax 9 months after the death. It is crucial to pay any taxes owed by these deadlines to avoid penalties.

What happens if I do not file the extension request on time?

If the extension request is not filed on time, you may be subject to penalties and interest on any unpaid taxes. It is essential to submit the request by the original due date to ensure that you can benefit from the extension provisions.

How do I submit the NJ Estate form IT-EXT?

The completed form should be mailed to the State of New Jersey, Division of Taxation, Individual Tax Audit Branch - Inheritance & Estate Tax, PO Box 249, Trenton, NJ 08695-0249. Make sure to include all required information to avoid delays in processing your request.

Will I receive a confirmation once my extension request is submitted?

What should I do if my extension request is denied?

If your extension request is denied, you will need to file the tax return by the original due date to avoid penalties. It may also be beneficial to consult a tax professional for guidance on how to proceed in this situation.

Here are eight common misconceptions about the NJ Estate form:

The NJ Estate form shares similarities with the IRS Form 706, the United States Estate (and Generation-Skipping Transfer) Tax Return. Both forms are used to report the value of a decedent's estate and calculate any taxes owed. While the NJ form focuses on state-specific inheritance and estate taxes, Form 706 serves a federal purpose. The deadlines for filing and extensions differ, with the IRS allowing for a longer initial extension period compared to New Jersey. However, both forms require detailed information about the decedent's assets and liabilities, ensuring that all taxable elements are accounted for.

Another comparable document is the IRS Form 1041, the U.S. Income Tax Return for Estates and Trusts. This form is filed by the estate to report income generated during the period of administration. Like the NJ Estate form, it requires specific information about the decedent and the estate's financial activities. While the NJ form addresses tax obligations at the time of death, Form 1041 focuses on ongoing income tax responsibilities. Both documents are essential for ensuring compliance with tax laws, albeit at different stages of the estate's lifecycle.

The NJ Estate form also bears resemblance to the probate court petition for letters testamentary or letters of administration. This document initiates the legal process of administering an estate. Both forms require identification of the decedent and the appointed executor or administrator. While the NJ form is concerned with tax extensions, the probate petition is about granting authority to manage the estate. Each document plays a crucial role in the overall estate administration process, ensuring that the decedent's wishes are honored and legal obligations met.

A Pennsylvania Bill of Sale form is crucial in documenting the sale and transfer of personal property, clearly listing the involved parties, item specifics, and sale amount. This ensures clarity and legal protection for both buyer and seller, helping to avert future disagreements. For detailed guidance on obtaining this essential document, visit topformsonline.com/pennsylvania-bill-of-sale.

Additionally, the NJ Estate form is similar to the IRS Form 8822, which is used to notify the IRS of a change of address. Although it serves a different purpose, both documents require accurate identification of the decedent or the estate representative. Keeping the IRS informed of address changes is essential for ensuring that tax correspondence reaches the appropriate parties. Similarly, the NJ Estate form ensures that the state is aware of the executor's contact information for tax-related communications.

The NJ Estate form is also akin to the final income tax return for the decedent, often filed using IRS Form 1040. This return accounts for the decedent's income up to the date of death. Both documents require comprehensive financial information and must be filed within specific timeframes. While the NJ Estate form deals with estate taxes, the final income tax return focuses on income tax obligations. Each form is vital in ensuring that all tax liabilities are settled appropriately.

Another related document is the NJ Inheritance Tax Return, which is specifically designed to report and calculate the inheritance tax owed by beneficiaries. Similar to the NJ Estate form, this document requires detailed information about the decedent's estate and the beneficiaries. Both forms are interconnected, as the inheritance tax return is often filed in conjunction with the estate tax return. They ensure that the state collects the appropriate taxes based on the decedent's assets and the beneficiaries' inheritances.

The NJ Estate form is also comparable to the Certificate of Death, which serves as official documentation of the decedent's passing. While the NJ form focuses on tax obligations, the Certificate of Death is crucial for initiating various legal processes, including probate. Both documents require accurate identification of the decedent and play significant roles in the administration of the estate. The Certificate of Death is often a prerequisite for filing the NJ Estate form, linking the two processes.

Moreover, the NJ Estate form is similar to a trust accounting document, which details the income and expenses of a trust during its administration. Both documents require transparency and accuracy in reporting financial information. While the NJ Estate form is concerned with tax obligations following a death, trust accounting focuses on the ongoing management of trust assets. Each document serves to protect the interests of beneficiaries and ensure compliance with legal standards.

Finally, the NJ Estate form can be compared to a property transfer deed, which is used to transfer ownership of real estate following a decedent's death. Both documents require detailed information about the property and the decedent. While the NJ form addresses tax obligations, the property transfer deed facilitates the actual transfer of assets to heirs or beneficiaries. Each document is essential in the overall process of settling an estate and ensuring that the decedent's wishes are fulfilled.