Printable Nj L 8 Form

Printable Nj L 8 Form

| Fact Name | Description |

|---|---|

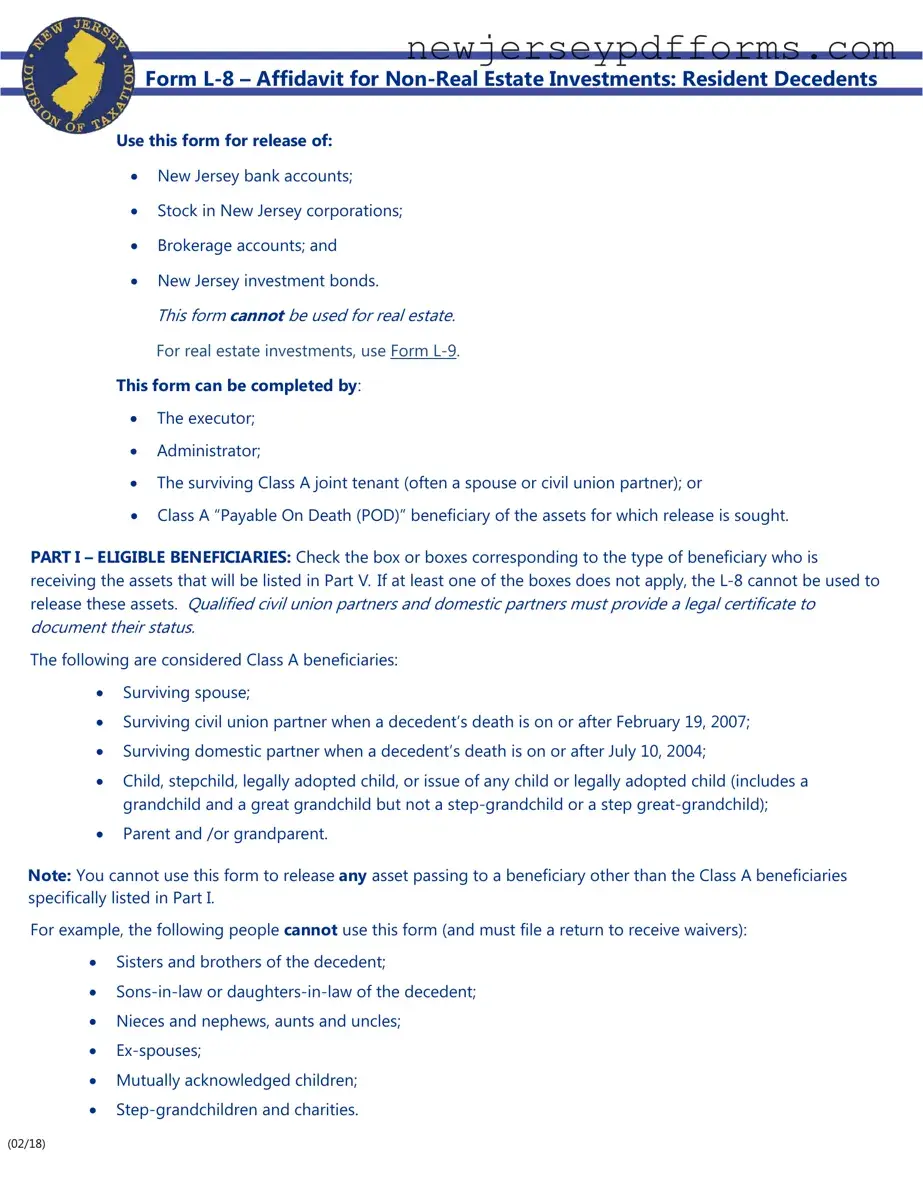

| Purpose | The NJ L-8 form is used to release New Jersey bank accounts, stock in New Jersey corporations, brokerage accounts, and New Jersey investment bonds for resident decedents. |

| Exclusions | This form cannot be used for real estate assets. For such assets, the NJ L-9 form must be utilized. |

| Eligible Filers | The form can be completed by the executor, administrator, surviving Class A joint tenant, or Class A Payable On Death (POD) beneficiary. |

| Class A Beneficiaries | Class A beneficiaries include the surviving spouse, civil union partner, domestic partner, children, stepchildren, legally adopted children, parents, and grandparents. |

| Trusts and Disclaimers | If any assets pass into or through a trust, the L-8 form cannot be used. A complete return must be filed in such cases. |

| Estate Tax Requirements | To qualify for using the L-8 form, the estate must meet specific tax thresholds based on the date of death, with no estate tax applicable for deaths on or after January 1, 2018. |

| Submission Instructions | The completed form should be taken or sent directly to the bank or financial institution holding the funds. It should not be mailed to the Division of Taxation. |

Nj Medical License Renewal Fee - Eligible businesses can benefit significantly from maintaining their active registration status.

Utilizing a well-structured form is essential, and to assist with this, landlords can refer to the PDF Document Service to find a reliable template, streamlining the process of gathering necessary details from prospective tenants.

Dba in Nj - The C-150G also includes a statement of intent to use the alternate name in New Jersey.

Filling out the New Jersey L-8 form can be a straightforward process, but many people make common mistakes that can lead to delays or complications. One frequent error occurs in Part I, where beneficiaries are identified. Some individuals fail to check at least one box, which is essential. If no boxes are checked, the form cannot be used, and an Inheritance Tax return must be filed instead. It is crucial to ensure that the beneficiaries listed are indeed Class A beneficiaries, as outlined in the form.

Another mistake often seen is in Part II, where individuals indicate how the assets are passed. Some people check the wrong box, which can invalidate the form. For instance, if assets are passed through a will but the appropriate box is not checked, the form cannot be processed. Always double-check that the selected option accurately reflects the situation regarding the assets.

In Part III, the issue of trusts can confuse many. If any assets listed on the L-8 form pass into or through a trust, the form cannot be used. Some people mistakenly believe that a minor’s bequest held in trust qualifies under this form. This misconception can lead to further complications, as a full return must then be filed with the Inheritance Tax Branch.

Another common error arises in Part IV, related to estate tax qualifications. Individuals sometimes miscalculate or misunderstand the estate tax thresholds. If the decedent's estate exceeds the specified limits, the L-8 form cannot be used. It is important to understand the estate tax laws relevant to the date of death and ensure that all conditions are met before proceeding.

In Part V, people often neglect to list all assets accurately. Each asset must be detailed separately, and failing to do so can lead to delays. For example, if a bank account is not listed or is incorrectly categorized, it could result in the rejection of the form. Properly documenting each asset ensures that the process moves smoothly.

Additionally, in Part VI, the relationships of beneficiaries to the decedent must be clearly stated. Many individuals mistakenly use terms like "Executor" or "Estate," which are not acceptable. Only relationships such as "Child," "Spouse," or "Grandchild" are valid. This oversight can lead to confusion and may require resubmission of the form.

Finally, the signature section often presents issues. The form must be signed by the appropriate parties, and the signature must be notarized. If these steps are skipped or done incorrectly, the form will not be accepted. Ensuring that all signatures are in place and properly notarized is essential for the form's validity.

What is the NJ L-8 form used for?

The NJ L-8 form, also known as the Affidavit for Non-Real Estate Investments, is used to request the release of certain assets following the death of a resident decedent. These assets may include New Jersey bank accounts, stock in New Jersey corporations, brokerage accounts, and New Jersey investment bonds. It is important to note that this form cannot be used for real estate assets; for those, the NJ L-9 form should be utilized.

Who is eligible to complete the NJ L-8 form?

The form can be completed by several parties, including the executor or administrator of the estate, the surviving Class A joint tenant (often a spouse or civil union partner), or a Class A Payable On Death (POD) beneficiary of the assets in question. It is crucial that the person completing the form is authorized to do so under New Jersey law.

What are Class A beneficiaries?

Class A beneficiaries are individuals who are eligible to receive assets without the need for further legal documentation. This group includes the surviving spouse, surviving civil union partner (if the decedent died on or after February 19, 2007), surviving domestic partner (if the decedent died on or after July 1, 2004), children, stepchildren, legally adopted children, parents, and grandparents. Other relatives, such as siblings or in-laws, do not qualify under this designation.

What should be included in Part V of the NJ L-8 form?

In Part V, individuals must list all the assets for which they are requesting a release. Each bank account or asset should be listed separately, including details such as the type of asset, how it is held or registered, and its value as of the date of death. Proper documentation is necessary to ensure that the financial institution can process the request without delays.

How does the estate tax affect the use of the NJ L-8 form?

The estate tax plays a significant role in determining eligibility to use the NJ L-8 form. If the decedent died on or after January 1, 2018, there is no estate tax, and the form can be used freely. However, if the decedent died between January 1, 2017, and January 1, 2018, their taxable estate must be under $2 million. For those who died before January 1, 2017, the taxable estate must be under $675,000. If the estate exceeds these limits, a full estate tax return must be filed instead.

What happens if the assets are held in a trust?

If any of the assets listed on the NJ L-8 form pass into or through a trust, the form cannot be used. In such cases, a complete return must be filed with the Inheritance Tax Branch. Trusts can complicate the distribution of assets, and it is essential to understand the specific terms of the trust to determine the correct filing procedures.

How should the completed NJ L-8 form be submitted?

The completed NJ L-8 form should be taken or sent directly to the financial institution holding the assets. It is important not to mail the form to the Division of Taxation, as doing so will not result in a waiver. The financial institution will verify the information and proceed with the release of the assets if everything is in order.

This is incorrect. The L-8 form is specifically designed for non-real estate investments such as bank accounts, stocks, and bonds. For real estate, you must use Form L-9.

Only specific individuals are authorized to complete this form. Eligible parties include the executor, administrator, surviving Class A joint tenant, or Class A Payable On Death (POD) beneficiary.

The form is limited to Class A beneficiaries. Individuals such as siblings, ex-spouses, and charities do not qualify and must file a different return.

In fact, qualified civil union partners and domestic partners must provide a legal certificate to confirm their status when using the L-8 form.

This is true only if the assets were jointly held or designated as POD. If the will specifies beneficiaries for the assets, a copy must be attached to the L-8 form.

Assets that pass into or through a trust cannot be released using the L-8 form. A full return must be filed instead.

It is essential to confirm that the estate qualifies under the estate tax criteria. If the estate exceeds certain limits, the L-8 form cannot be used.

This is incorrect. The completed form should be taken or sent directly to the financial institution holding the funds, not mailed to the Division of Taxation.

It is crucial to specify the exact relationship, such as Child or Spouse, rather than using terms like Executor or Beneficiary, which are not acceptable.

The L-8 form is an affidavit and must be signed in the presence of a notary public to be valid.

The New Jersey Form L-9 is a counterpart to the L-8, specifically designed for real estate assets. While the L-8 focuses on non-real estate investments like bank accounts and stocks, the L-9 is utilized when dealing with properties such as homes or land. Similar to the L-8, the L-9 can be completed by the executor or administrator, and it also requires the identification of beneficiaries. However, the L-9 emphasizes the need for a complete property description and may require additional documentation, such as a deed, to validate the transfer of real estate assets.

Form L-10 serves a similar purpose as the L-8 in that it is used for the release of assets held in a trust. While the L-8 cannot be used when assets pass through a trust, the L-10 is specifically tailored for those situations. Both forms require the identification of beneficiaries and the declaration of asset types. However, the L-10 includes additional sections to address the complexities of trust distributions and may require the inclusion of trust documents to ensure compliance with legal requirements.

The New Jersey Inheritance Tax Return (Form IT-R) is another document that shares similarities with the L-8. While the L-8 is used for a streamlined release of certain assets to Class A beneficiaries, the IT-R is a comprehensive form that reports all assets of the decedent's estate. It is necessary when the estate exceeds certain thresholds or when the beneficiaries do not qualify under the L-8. Both forms require detailed information about the decedent's assets and beneficiaries, but the IT-R demands a broader scope of disclosure and may involve tax implications that the L-8 does not.

Form L-6 is also related to the L-8 in that it deals with the release of assets but is specifically for non-resident decedents. Like the L-8, the L-6 allows for the release of certain financial accounts and securities, but it is tailored for individuals who were not residents of New Jersey at the time of their death. Both forms require the executor or administrator to verify the eligibility of beneficiaries, but the L-6 includes additional steps to confirm the decedent's residency status and may involve different tax considerations based on the decedent's estate location.