Printable Nj St 5 Form

Printable Nj St 5 Form

| Fact Name | Details |

|---|---|

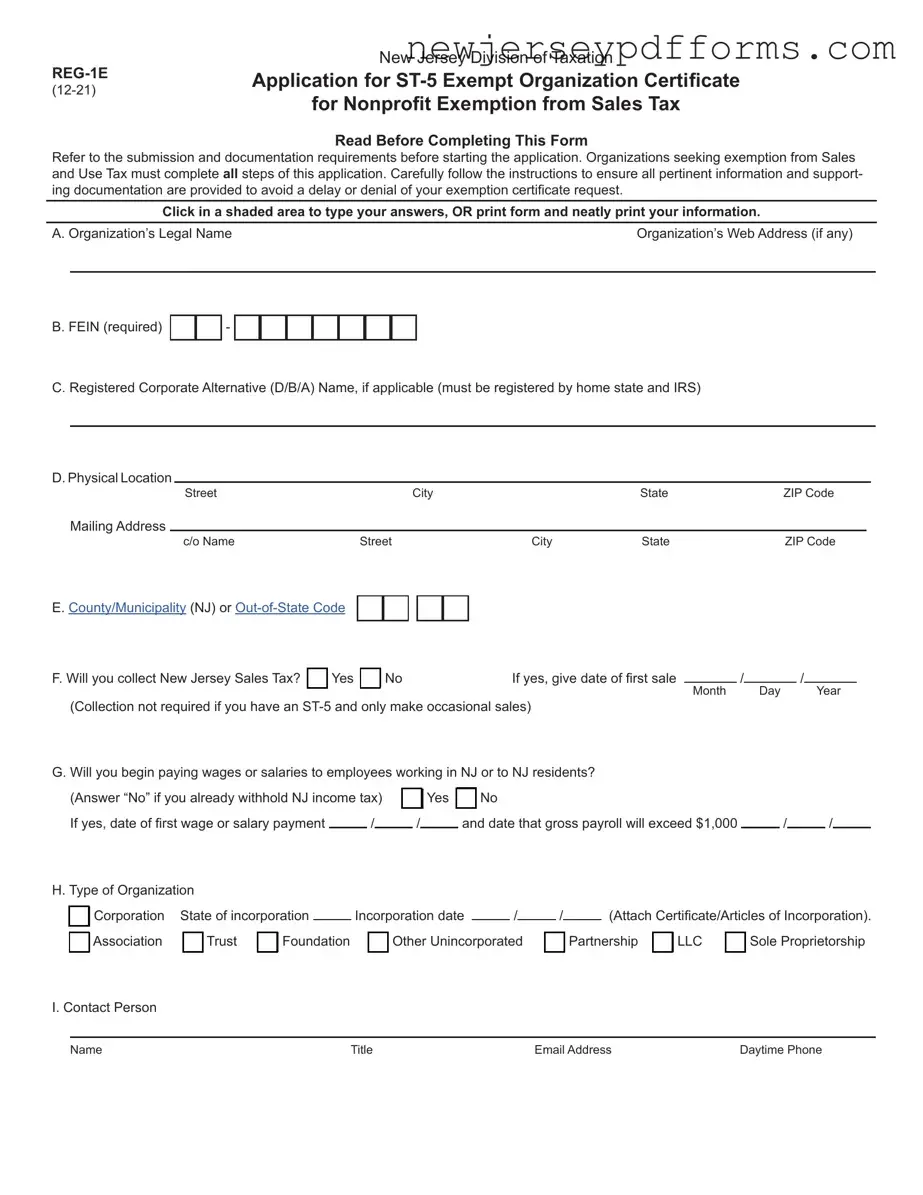

| Purpose of Form | The NJ ST-5 form is used to apply for an Exempt Organization Certificate for entities seeking sales tax exemption in New Jersey. |

| Governing Laws | This form is governed by the New Jersey Sales and Use Tax Act, specifically N.J.S.A. 54:32B-1 et seq. |

| Required Documentation | Applicants must submit a checklist of required documents along with the form to ensure processing. Missing documentation will delay the issuance of the ST-5 certificate. |

| Filing Instructions | To file, mail the completed form and all required documents to the New Jersey Division of Taxation. Allow at least three weeks for processing. |

Imm-7 - Ensuring every child is vaccinated contributes to herd immunity within the community.

Nj Medical License Renewal Fee - Be diligent in ensuring your documents are prepared for submission by the deadlines.

In order to establish a clear framework for your LLC, it is important to consider the importance of an Operating Agreement, which serves as a foundational document outlining the management structure and operating procedures. This agreement not only details the rights and responsibilities of its members but also ensures that all parties are aligned with the business's goals. For further insights on crafting this essential document, you can visit https://topformsonline.com/operating-agreement/.

Free Annulment Forms - Sample forms for filing a motion in the Civil Part are also available online.

Filling out the New Jersey ST-5 form can be a straightforward process, but many individuals make mistakes that can delay their application or even result in denial. One common error is failing to include the required documentation. The checklist on the first page is crucial. If you don’t check off each item and submit the necessary documents, your application will not be processed. This oversight can lead to significant delays, as you may have to start the process all over again.

Another frequent mistake is providing incorrect or incomplete information. Every detail matters, from the name of the organization to the physical address. If there are discrepancies or missing information, it can raise red flags during the review process. It’s essential to double-check all entries for accuracy. A simple typo could mean the difference between approval and rejection.

Many applicants also overlook the importance of signatures. The form requires a signature certifying that all information provided is correct. Skipping this step is a common mistake that can halt the processing of your application. Ensure that the signature is not only present but also matches the name printed on the form. This attention to detail can prevent unnecessary complications.

Lastly, timing is crucial. Some individuals fail to account for processing times. The New Jersey Division of Taxation advises allowing at least three weeks for processing after submission. If you submit your application close to a deadline without considering this timeframe, you might find yourself in a bind. Planning ahead and submitting your application early can help avoid last-minute issues.

What is the NJ ST-5 form?

The NJ ST-5 form is an application for the Exempt Organization Certificate issued by the New Jersey Division of Taxation. This certificate allows qualifying organizations, such as nonprofits, to claim exemption from sales tax on certain purchases. It's essential for organizations that operate for charitable, educational, or religious purposes and wish to benefit from tax exemptions.

Who is eligible to file the NJ ST-5 form?

Organizations that can file the NJ ST-5 form include religious, charitable, scientific, and educational entities. Additionally, volunteer emergency organizations and certain nonprofit organizations that provide specific services may also qualify. It's important to ensure that your organization meets the criteria set by the New Jersey Division of Taxation before applying.

What documentation is required to submit with the NJ ST-5 form?

When submitting the NJ ST-5 form, organizations must include a completed REG-1E form along with a checklist of required documents. This may include proof of the organization’s tax-exempt status, articles of incorporation, and other supporting materials that demonstrate eligibility for exemption. If any required documentation is missing, the application may be delayed or denied.

How much does it cost to file the NJ ST-5 form?

There is no filing fee associated with the NJ ST-5 form. However, organizations should be aware of potential costs related to gathering required documentation or any legal assistance they may seek during the application process.

Where should the NJ ST-5 form be filed?

The completed NJ ST-5 form and accompanying documents should be mailed to the New Jersey Division of Taxation. It’s advisable to send the application to the specific address provided for the Exempt Organization Certificate to ensure proper processing.

How long does it take to process the NJ ST-5 form?

Organizations should allow at least three weeks for the New Jersey Division of Taxation to process a completed NJ ST-5 application. This timeframe can vary depending on the volume of applications received and whether all required documentation has been submitted correctly.

What should organizations do if they are not eligible to file the NJ ST-5 form?

If an organization does not meet the eligibility criteria for the NJ ST-5 form, it should refrain from submitting the application. Instead, organizations may need to explore other tax-exempt options or consult with a tax professional for guidance on their specific situation.

Can organizations amend their NJ ST-5 application after submission?

Yes, if an organization realizes that it has made an error or needs to update information after submitting the NJ ST-5 application, it should contact the New Jersey Division of Taxation directly. They can provide guidance on how to correct the application or submit additional information if necessary.

Understanding the NJ ST-5 form can be challenging, and there are several misconceptions that people often have. Here’s a list of ten common misunderstandings, along with clarifications to help you navigate the process more effectively.

By understanding these misconceptions, organizations can better prepare for the application process and ensure they meet all necessary requirements. Proper preparation can make a significant difference in successfully obtaining tax-exempt status.

The IRS Form 1023, Application for Recognition of Exemption Under Section 501(c)(3) of the Internal Revenue Code, is similar to the NJ ST-5 form in that both documents are used by organizations seeking tax-exempt status. Form 1023 is specifically for organizations that qualify under section 501(c)(3), which includes charitable, religious, educational, and scientific organizations. Like the NJ ST-5, the IRS form requires detailed information about the organization’s structure, purpose, and activities, as well as supporting documentation to substantiate the claims made in the application.

The IRS Form 990, Return of Organization Exempt from Income Tax, shares similarities with the NJ ST-5 form as both serve to provide transparency and accountability for tax-exempt organizations. While the NJ ST-5 is an application for exemption, Form 990 is an annual reporting return that provides information on the organization’s financial status, governance, and compliance with tax regulations. Both forms require organizations to disclose financial information, including revenue and expenses, which helps the state and federal authorities monitor compliance with tax laws.

The IRS Form 1024, Application for Recognition of Exemption Under Section 501(a), is another document akin to the NJ ST-5. This form is utilized by organizations seeking exemption under various sections of the Internal Revenue Code, not just 501(c)(3). Similar to the NJ ST-5, Form 1024 requires the organization to provide a description of its activities and purposes, along with supporting documentation to justify its request for tax-exempt status.

The New Jersey Division of Taxation’s REG-1E form is closely related to the NJ ST-5. The REG-1E is the application for a sales tax exemption certificate for nonprofit organizations. Both forms require organizations to demonstrate their eligibility for tax exemptions, and the REG-1E must be submitted along with the NJ ST-5 to initiate the exemption process. The documentation required for both forms ensures that the organization meets the necessary criteria for tax-exempt status.

The Form 990-N, e-Postcard, is a simplified version of the Form 990, designed for small tax-exempt organizations with gross receipts of $50,000 or less. While it is not directly comparable to the NJ ST-5, both documents serve to maintain the tax-exempt status of organizations by requiring them to report their financial activities. The Form 990-N is an easy way for small organizations to comply with federal reporting requirements, similar to how the NJ ST-5 facilitates state-level compliance.

The New Jersey Nonprofit Corporation Annual Report is another document similar to the NJ ST-5. This report must be filed annually by nonprofit organizations registered in New Jersey. Like the NJ ST-5, it requires organizations to provide information about their activities, governance, and financial status. Both forms are essential for maintaining compliance with state regulations and ensuring that organizations remain in good standing.

For anyone navigating the complexities of divorce in California, the key Divorce Settlement Agreement details can provide crucial guidance. This document outlines the necessary terms and helps ensure a smoother process by addressing important aspects like property division and spousal support. Having a clear understanding of these elements is vital for both parties involved.

The IRS Form 990-T, Exempt Organization Business Income Tax Return, is relevant as it addresses the taxation of unrelated business income for tax-exempt organizations. While the NJ ST-5 focuses on obtaining tax-exempt status, the 990-T ensures that organizations report and pay taxes on income generated from activities not substantially related to their exempt purpose. Both forms reflect the broader regulatory framework governing tax-exempt organizations.

The New Jersey Charitable Registration and Investigation Act registration form is similar to the NJ ST-5 in that it requires charitable organizations to register with the state before soliciting donations. Both documents aim to ensure that organizations operate transparently and in compliance with state laws. The registration form requires organizations to provide information about their mission, governance, and financial practices, similar to the information required in the NJ ST-5.

The New Jersey Division of Taxation’s ST-4 Exempt Use Certificate is akin to the NJ ST-5 as both relate to tax exemptions. The ST-4 is used by organizations to claim exemption from sales tax on purchases made for exempt purposes. Like the NJ ST-5, the ST-4 requires organizations to provide evidence of their tax-exempt status and ensure compliance with state tax regulations.

Lastly, the New Jersey Sales Tax Exempt Organization Certificate (ST-5) is similar to the ST-5 form in that it is issued to organizations that qualify for sales tax exemption. Both forms require organizations to provide documentation proving their eligibility for tax-exempt status. The ST-5 serves as a certificate that organizations can present to vendors to make tax-exempt purchases, reinforcing the relationship between the two documents.