Printable Nj Ttd Form

Printable Nj Ttd Form

| Fact Name | Fact Description |

|---|---|

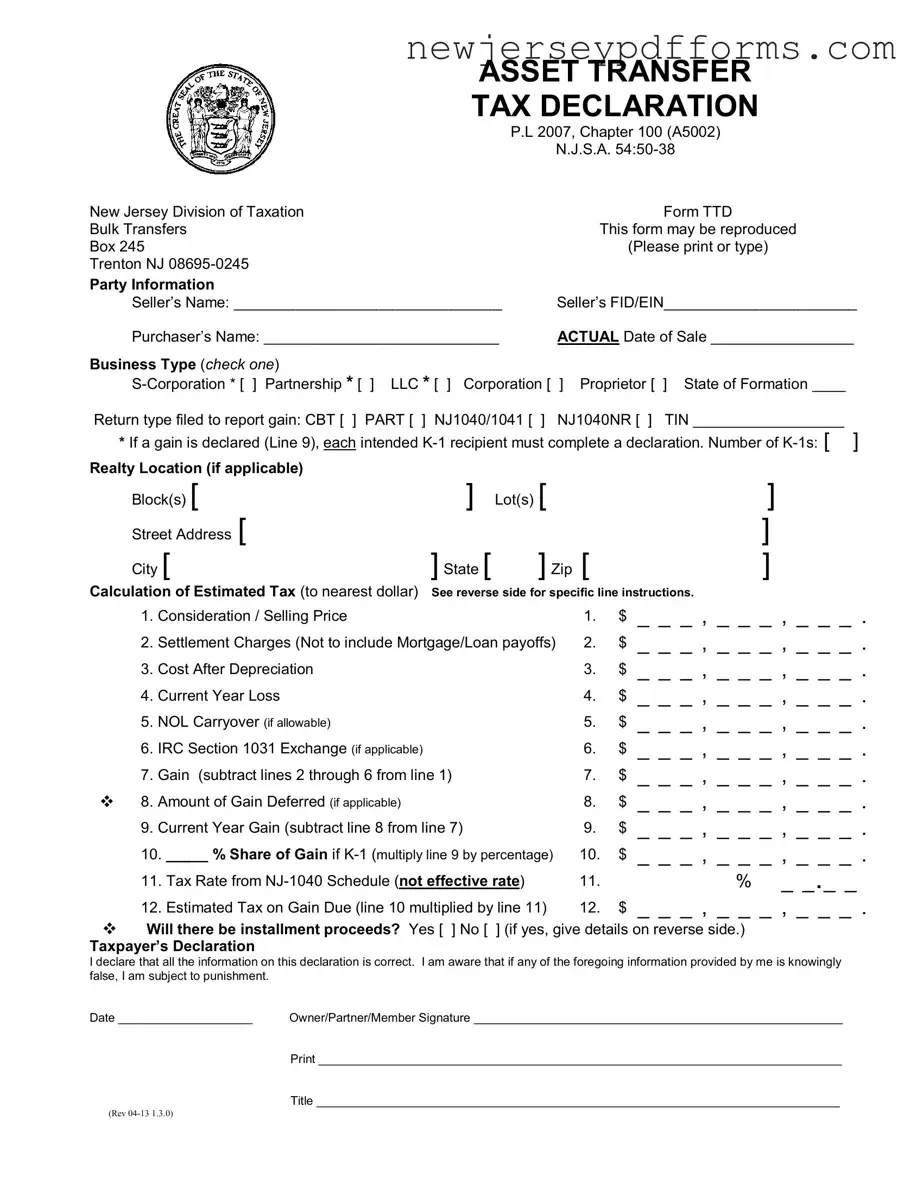

| Form Title | The form is officially titled "Asset Transfer Tax Declaration". |

| Governing Law | This form is governed by P.L. 2007, Chapter 100 (A5002) and N.J.S.A. 54:50-38. |

| Issuing Authority | The New Jersey Division of Taxation issues this form. |

| Purpose | This form is used to declare the estimated tax on the gain from the transfer of business assets. |

| Seller Information | It requires the seller's name and Federal Identification Number (FID/EIN). |

| Purchaser Information | The purchaser's name must also be provided on the form. |

| Business Types | Various business types can be indicated, including S-Corporation, Partnership, LLC, and Corporation. |

| Tax Calculation | Estimated tax is calculated based on the gain from the sale of assets. |

| K-1 Requirement | If a gain is declared, each intended K-1 recipient must complete a declaration. |

| Submission Process | Upon completion, the form must be submitted to the Division for review and processing. |

Amend Nj Business Registration - Possible reasons for filing this form include name changes, agent changes, or structural changes.

For those looking to create a Pennsylvania Bill of Sale form, it is important to utilize a reliable source to ensure all necessary details are accurately included; you can find a comprehensive template at topformsonline.com/pennsylvania-bill-of-sale, which simplifies the process and ensures compliance with local regulations.

How Do I Get a Copy of My Nj Sales Tax Certificate - The form serves as a protective measure for the purchaser regarding tax liabilities.

When completing the New Jersey TTD form, individuals often make mistakes that can lead to complications. One common error is failing to provide accurate information in the Party Information section. This includes the seller's and purchaser's names, as well as their respective FID/EIN numbers. Inaccurate or incomplete entries can result in delays or even rejection of the form.

Another frequent mistake involves the Calculation of Estimated Tax section. Many people overlook the importance of correctly entering figures for the selling price, settlement charges, and other relevant calculations. For instance, omitting necessary deductions or incorrectly calculating the gain can lead to an inaccurate tax estimate, which may affect the final tax obligations.

Additionally, individuals sometimes neglect to check the appropriate boxes regarding the business type and return type filed. This oversight can create confusion for the Division of Taxation, as they rely on this information to process the form correctly. Ensuring that all selections are made clearly is crucial for a smooth review process.

Lastly, some filers forget to sign and date the declaration. This step is essential, as the signature certifies that the information provided is accurate and complete. Without a signature, the form may be deemed invalid, causing further delays in the processing of the transaction.

What is the NJ TTD form?

The NJ TTD form, or Asset Transfer Tax Declaration, is a document required by the New Jersey Division of Taxation. It is used to report the transfer of business assets and calculate any estimated tax due on the gain from the sale. This form ensures that the state is aware of potential tax liabilities associated with the transfer.

Who needs to fill out the NJ TTD form?

The seller of business assets must complete the NJ TTD form. This includes various business structures such as corporations, partnerships, LLCs, and sole proprietorships. If the seller is transferring assets, they are responsible for reporting the transaction using this form.

What information is required on the NJ TTD form?

The form requires details such as the seller's and purchaser's names, the date of sale, business type, and financial figures related to the transaction. This includes the selling price, settlement charges, cost after depreciation, and any losses or gains. Accurate information is crucial for calculating estimated taxes.

How is the estimated tax calculated on the NJ TTD form?

The estimated tax is calculated based on the gain from the sale of the assets. This involves subtracting certain costs, like settlement charges and depreciation, from the total selling price. The result determines the taxable gain, which is then multiplied by the applicable tax rate to find the estimated tax due.

What happens if the information on the NJ TTD form is incorrect?

If the information provided is incorrect, the seller may face penalties. The form includes a declaration stating that the information is accurate. Providing false information can lead to legal consequences, including fines or other penalties from the state.

Is there a deadline for submitting the NJ TTD form?

The NJ TTD form should be submitted at the time of the asset transfer, typically during the closing of the transaction. It is important to ensure that this form is filed promptly to avoid complications with tax liabilities.

What if there are installment proceeds involved in the asset transfer?

If the sale involves installment proceeds, the seller must indicate this on the form. Additional details about the installment terms should be provided. The estimated tax may be adjusted based on the specifics of the installment agreement.

Can the NJ TTD form be reproduced?

Yes, the NJ TTD form can be reproduced. It is important that all copies maintain the same format and clarity as the original to ensure proper processing by the New Jersey Division of Taxation.

What should be done after submitting the NJ TTD form?

After submitting the form, the estimated tax will be held in escrow until the transaction closes. The Division of Taxation will review the form and communicate any necessary adjustments. The seller will then file their year-end tax return, claiming credit for the estimated tax paid.

Where can I obtain the NJ TTD form?

The NJ TTD form can be obtained from the New Jersey Division of Taxation's website or by contacting their office directly. It is also available at various tax preparation offices and legal service providers.

Understanding the NJ TTD form can be challenging. Here are five common misconceptions about it.

The NJ TTD form, which is used for asset transfer tax declarations, bears similarities to the IRS Form 8594, Asset Acquisition Statement. Both documents are essential for reporting the transfer of assets in business transactions. The IRS Form 8594 requires sellers and buyers to disclose information about the assets being transferred, including the total consideration paid. This form also helps determine the tax consequences of the sale, similar to how the NJ TTD form calculates the estimated tax on gains from asset transfers. Both forms aim to ensure transparency and compliance with tax regulations, providing a clear record of the transaction for tax authorities.

The understanding of financial documents, such as the Profit and Loss form, extends beyond traditional business practices. For instance, organizations can find templates that help in preparing these forms easily; one such resource is the PDF Document Service, which provides handy tools for accurate financial documentation and analysis. By effectively utilizing such resources, businesses can enhance clarity in their financial dealings and ensure compliance with necessary regulations.

Another comparable document is the New Jersey Corporation Business Tax (CBT) return. This return is filed by corporations to report income, calculate taxes owed, and claim any credits. Like the NJ TTD form, the CBT return requires detailed financial information, including income, deductions, and tax calculations. Both documents serve as critical tools for the state to assess tax liabilities accurately. They ensure that businesses report their financial activities correctly and pay the appropriate amount of tax, which is vital for maintaining the state's revenue stream.

The IRS Form 1065, U.S. Return of Partnership Income, also shares similarities with the NJ TTD form. This form is used by partnerships to report income, deductions, and other tax-related information. Like the NJ TTD, it requires detailed financial disclosures and determines how much tax is owed based on the partnership's earnings. Both forms emphasize the importance of accurate reporting and compliance, as they are essential for the proper assessment of tax liabilities for partnerships operating in New Jersey.

The NJ-1040 form, which is the New Jersey Resident Income Tax Return, is another document that parallels the NJ TTD form. This form is used by individuals to report their income and calculate state taxes owed. While the NJ TTD focuses on the transfer of business assets, the NJ-1040 captures personal income and tax obligations. Both forms require taxpayers to provide detailed financial information and calculations, ensuring that the state can accurately assess and collect taxes owed based on the reported income or gains.

Lastly, the New Jersey Sales Tax Certificate of Authority is akin to the NJ TTD form in that it regulates financial transactions within the state. This certificate allows businesses to collect sales tax from customers and remit it to the state. Similar to the NJ TTD form, it serves to ensure compliance with tax laws and provides the state with necessary information about business transactions. Both documents aim to facilitate proper tax collection and reporting, which is crucial for maintaining the state's fiscal health.