Printable Nj W 3M Form

Printable Nj W 3M Form

| Fact Name | Details |

|---|---|

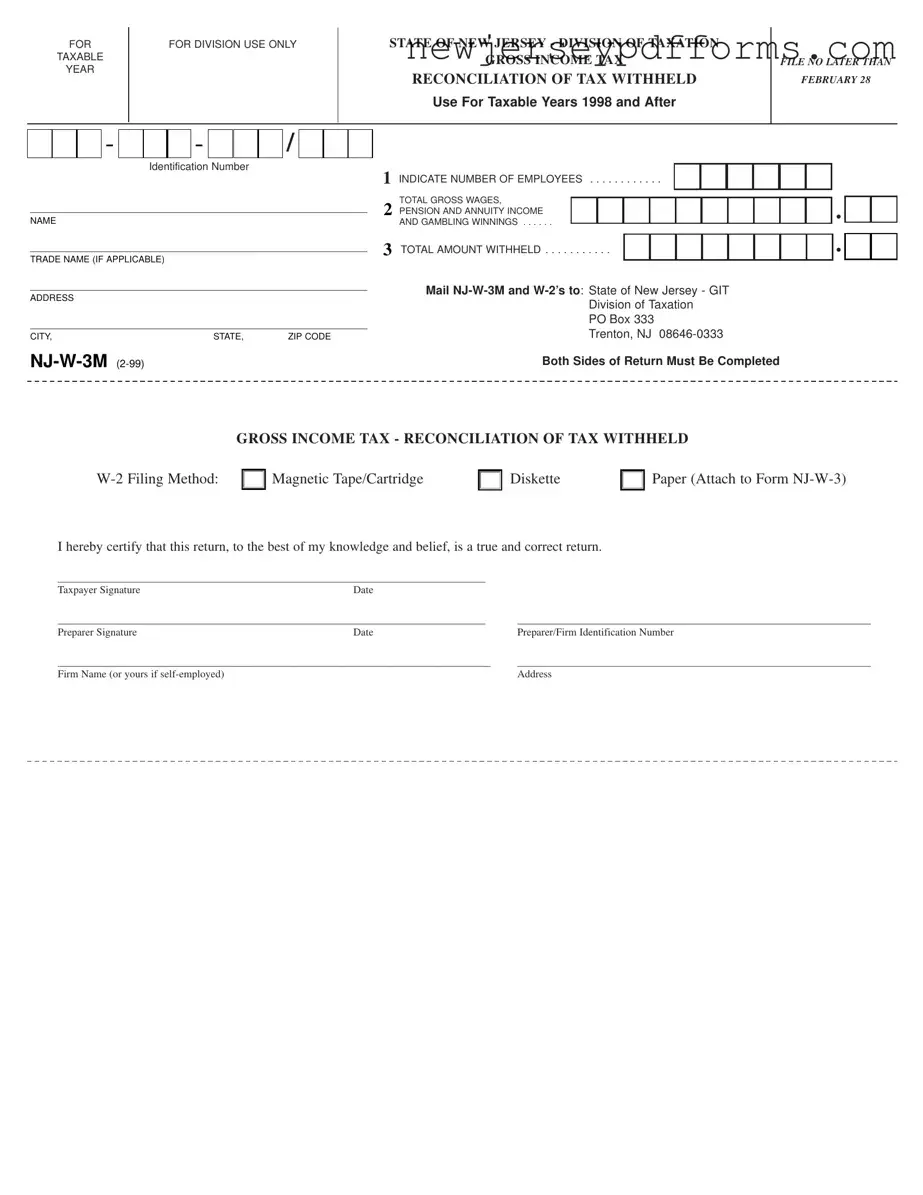

| Purpose | The NJ W-3M form is used for reconciling gross income tax withheld for employees in New Jersey. |

| Filing Deadline | This form must be filed no later than February 28 of the year following the taxable year. |

| Applicable Tax Years | The NJ W-3M form is applicable for taxable years 1998 and after. |

| Governing Law | The form is governed by New Jersey's Gross Income Tax Act, N.J.S.A. 54A:1-1 et seq. |

| Employee Information | Employers must indicate the number of employees and total gross wages on the form. |

| Submission Address | Completed forms should be mailed to the State of New Jersey, GIT Division of Taxation, PO Box 333, Trenton, NJ 08646-0333. |

Nj Lemon Law Used Car - Chronicle all repair attempts in detail, including dates and the duration your vehicle was out of service.

To ensure that your workplace injury claims are handled with the utmost care and efficiency, it is essential to be familiar with the process outlined in the Georgia WC-14 form. This important document notifies the Georgia State Board of Workers' Compensation of your claims and facilitates the necessary procedures for mediation or hearings. For further details and access to the form, please visit https://formsgeorgia.com.

Form 1040-es Estimated Tax for Individuals - The closing date of the transaction should be included on the form.

Filling out the NJ W-3M form can be straightforward, but many individuals make common mistakes that can lead to complications. One frequent error is failing to complete both sides of the return. This form requires information on both sides, and omitting details can delay processing.

Another mistake is not providing accurate identification numbers. Whether it’s the employer identification number or the taxpayer identification number, errors here can cause significant issues. Double-checking these numbers before submission is crucial.

Many people also overlook the importance of signing the form. The certification statement at the bottom requires a signature from both the taxpayer and the preparer, if applicable. Without these signatures, the form may be considered incomplete.

Inaccurate wage reporting is a common pitfall. Ensure that the total gross wages, pension and annuity income, and gambling winnings are accurately reported. Misreporting these figures can lead to discrepancies in tax calculations.

Another mistake involves the filing method selection. The form allows for different filing methods, including magnetic tape, diskette, or paper. Failing to indicate the correct method can result in processing delays.

People often forget to include the total amount withheld. This figure is essential for reconciling the gross income tax withheld. Missing this information can complicate the review process.

Incorrectly entering the number of employees is another issue that arises frequently. This number should reflect the total employees for whom W-2s are being filed. An inaccurate count can lead to further inquiries from the tax division.

Some individuals neglect to include the trade name, if applicable. If the business operates under a different name, it’s important to provide this information to avoid confusion.

Inadequate attention to detail in the address section can also create problems. Ensure that the address is complete and accurate, including city, state, and ZIP code. An incorrect address may cause the form to be misdirected.

Lastly, failing to mail the NJ W-3M and W-2s to the correct address can lead to delays. Always verify the mailing address provided on the form to ensure timely processing.

What is the NJ W-3M form?

The NJ W-3M form is used for the reconciliation of tax withheld for gross income tax in New Jersey. It is required for taxable years 1998 and later. Employers must file this form along with their W-2s to report the total wages paid and the taxes withheld from employees.

Who needs to file the NJ W-3M form?

Employers who have employees in New Jersey and withhold state income tax from their wages must file the NJ W-3M form. This includes businesses of all sizes, from small companies to large corporations.

When is the NJ W-3M form due?

The NJ W-3M form must be filed no later than February 28 of the year following the tax year for which the wages and withholding are reported. For example, for the 2023 tax year, the form is due by February 28, 2024.

What information is required on the NJ W-3M form?

The form requires several key pieces of information, including the employer's identification number, name, trade name (if applicable), address, total number of employees, total gross wages, pension and annuity income, gambling winnings, and the total amount withheld for taxes.

How do I submit the NJ W-3M form?

The completed NJ W-3M form, along with all W-2 forms, should be mailed to the State of New Jersey, Division of Taxation, at the specified address: PO Box 333, Trenton, NJ 08646-0333. Ensure that both sides of the return are completed before submission.

Can I file the NJ W-3M form electronically?

Yes, employers can file the NJ W-3M form electronically if they choose to use magnetic tape, cartridge, or diskette filing methods. However, if filing on paper, the form must be attached to the W-2 forms.

What happens if I miss the filing deadline?

Failing to file the NJ W-3M form by the deadline may result in penalties and interest on any taxes owed. It's important to file on time to avoid these additional costs and complications.

Is there a penalty for incorrect information on the NJ W-3M form?

Yes, providing incorrect information on the NJ W-3M form can lead to penalties. It's crucial to ensure that all information is accurate and complete to avoid any issues with the New Jersey Division of Taxation.

Can I amend the NJ W-3M form after filing?

If you discover an error after submitting the NJ W-3M form, you can amend it. You will need to file a corrected NJ W-3M form along with corrected W-2 forms to rectify any inaccuracies.

Where can I find more information about the NJ W-3M form?

For more detailed information, you can visit the New Jersey Division of Taxation's website or contact their office directly. They provide resources and guidance to help employers comply with filing requirements.

Understanding the NJ W-3M form is crucial for accurate tax reporting in New Jersey. However, several misconceptions can lead to confusion. Below is a list of common misconceptions, along with clarifications for each.

Clarifying these misconceptions can help ensure compliance and accuracy in tax reporting. It is advisable to consult the New Jersey Division of Taxation for the most current information and guidance.

The IRS Form W-3 serves as a summary of the W-2 forms issued by an employer. Similar to the NJ W-3M, it reconciles the total wages paid and taxes withheld for employees. Employers must file the W-3 by the end of January each year, ensuring that the information matches the individual W-2s submitted to the IRS. Both forms are essential for accurate tax reporting and compliance, helping to ensure that the correct amount of tax is reported and paid.

The 1099-MISC form is another document that shares similarities with the NJ W-3M. This form is used to report income paid to independent contractors and freelancers. Like the W-2, the 1099-MISC requires accurate reporting of the total amount paid and any taxes withheld. Both forms serve to provide transparency in income reporting, ensuring that the IRS receives the necessary information for tax purposes.

The 1099-NEC is specifically designed for reporting non-employee compensation, making it closely related to the NJ W-3M. This form was reintroduced in 2020 to separate non-employee compensation from other types of income reported on the 1099-MISC. Both forms require the payer to report total payments made, ensuring that recipients report their income accurately on their tax returns.

For those considering a purchase, having a legal record such as a reliable Horse Bill of Sale document can be invaluable. This form protects both parties involved in the transaction by documenting ownership transfer and ensuring clarity on the sale details.

The NJ-1040 form is the New Jersey resident income tax return. It is similar to the NJ W-3M in that it requires individuals to report their total income and taxes withheld. Both documents are crucial for tax compliance in New Jersey, as they ensure that residents fulfill their tax obligations based on their earnings and withholdings throughout the year.

The Schedule C form is used by sole proprietors to report income or loss from a business. While it does not directly reconcile withholdings like the NJ W-3M, it shares the goal of providing accurate income reporting. Both documents are essential for ensuring that taxpayers report their earnings correctly, allowing for proper tax assessment and compliance.

The Form 941 is the Employer's Quarterly Federal Tax Return. This form is similar to the NJ W-3M in that it reports the total wages paid and taxes withheld for employees. While the NJ W-3M is an annual reconciliation, Form 941 is filed quarterly, ensuring that the IRS receives timely updates on tax withholdings and payments made throughout the year.

The 1095-C form is used by applicable large employers to report health insurance coverage offered to employees. Although it focuses on healthcare rather than income, it shares the common purpose of ensuring accurate reporting of employee-related information. Both forms contribute to the overall compliance of employers with federal and state regulations.

The Form 1098 is used to report mortgage interest paid by individuals. While it is not directly related to employment income, it serves a similar purpose in terms of income reporting. Both the 1098 and the NJ W-3M are essential for taxpayers to provide accurate information to the IRS, ensuring that deductions and credits are claimed correctly.

The Form 4506-T is a request for a transcript of tax return information. While it does not report income directly, it is used by taxpayers to verify information with the IRS. Similar to the NJ W-3M, it plays a role in ensuring that accurate records are maintained, which is crucial for tax compliance and auditing purposes.

The Form 1040 is the U.S. Individual Income Tax Return, where individuals report their total income, including wages and other sources. Like the NJ W-3M, it requires accurate reporting of income and taxes withheld. Both forms are essential for ensuring that taxpayers meet their obligations and that the correct amount of tax is assessed based on reported earnings.