Printable Nj W3 Form

Printable Nj W3 Form

| Fact Name | Fact Description |

|---|---|

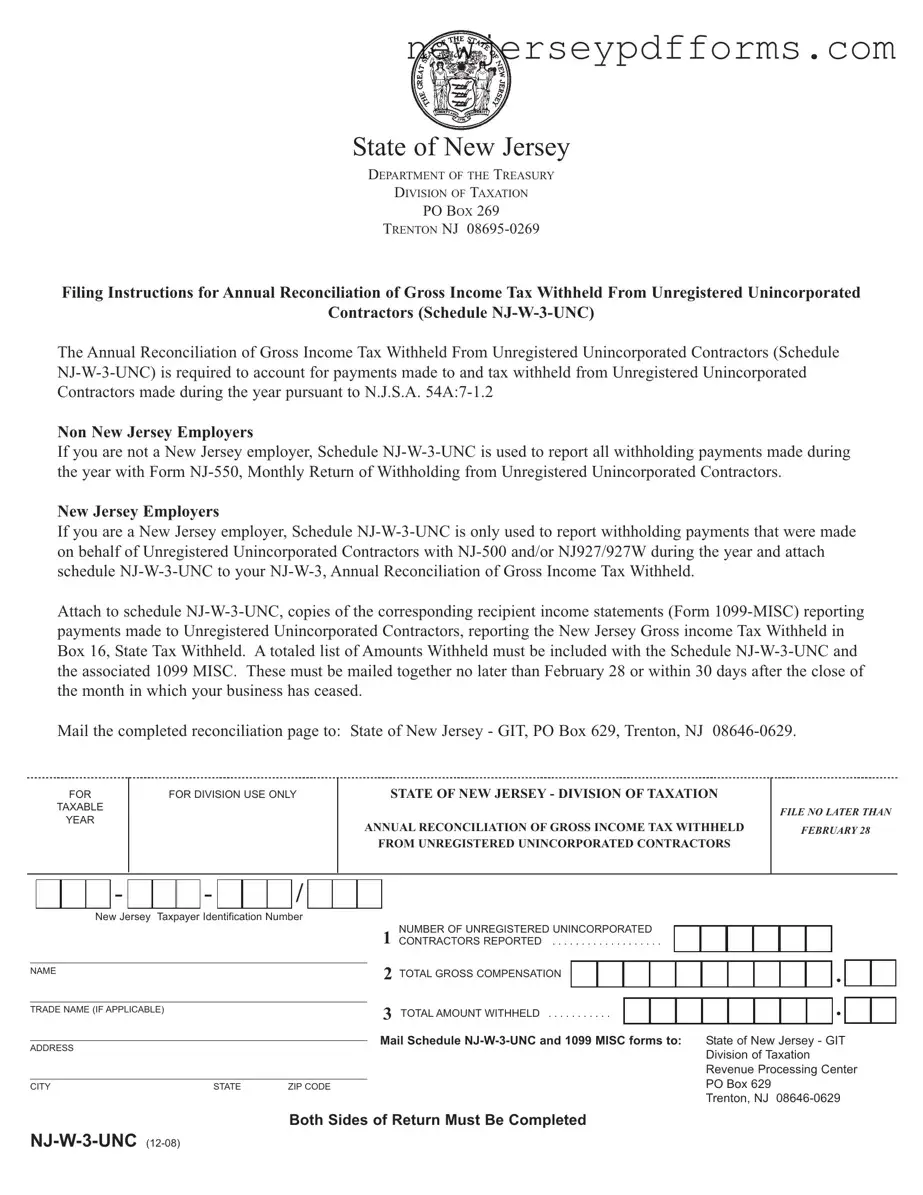

| Purpose | The NJ W3 form is used for the annual reconciliation of gross income tax withheld from unregistered unincorporated contractors. |

| Governing Law | The form is governed by New Jersey Statutes Annotated, specifically N.J.S.A. 54A:7-1.2. |

| Filing Deadline | Completed forms must be submitted by February 28 or within 30 days after the close of the month in which the business has ceased. |

| Recipient Statements | Taxpayers must attach copies of Form 1099-MISC, which report payments made to contractors and the corresponding New Jersey gross income tax withheld. |

| Reporting Requirements | New Jersey employers must report withholding payments made on behalf of unregistered contractors using NJ-500 and/or NJ-927/927W. |

| Mailing Address | Completed forms should be mailed to the State of New Jersey - GIT, PO Box 629, Trenton, NJ 08646-0629. |

| Identification Number | Taxpayers must provide their New Jersey Taxpayer Identification Number on the form. |

| Contractor Count | Line 1 of the form requires the number of unregistered unincorporated contractors to whom payments were made during the year. |

| Gross Compensation | Line 2 requires the total gross compensation paid to unregistered unincorporated contractors during the year. |

| Withholding Amount | Line 3 asks for the total amount withheld from payments to unregistered unincorporated contractors during the year. |

Work in Nj Live in Pa Taxes - The form requires personal information including your name, address, and Social Security number.

The Profit and Loss form, often referred to as the income statement, is a financial document that summarizes a company's revenues and expenses over a specific period. It helps businesses understand their financial performance, illustrating how much profit or loss was generated. For those looking to simplify this process, templates can be invaluable, and resources like PDF Document Service provide useful tools for creating accurate reports that drive informed decision-making regarding operations and strategies.

Child Custody Application Form Nj - The application requires detailing why the modification is necessary or requested.

Filling out the NJ W3 form can be a straightforward process, but many individuals make common mistakes that can lead to complications. Understanding these pitfalls is essential to ensure a smooth filing experience. Here are nine mistakes to watch out for.

One frequent error is failing to include the New Jersey Taxpayer Identification Number. This number is crucial for the state to identify your business and process your submission. Without it, your form may be delayed or rejected. Always double-check that this number is entered correctly.

Another common mistake is not reporting the correct number of unregistered unincorporated contractors. Line 1 of the form requires you to enter the exact number of contractors you made payments to during the year. An incorrect count can lead to discrepancies in your tax records.

Many people also overlook the total gross compensation amount. Line 2 must reflect the total gross amount paid to these contractors. If this figure is inaccurate, it could result in penalties or audits, so be meticulous when calculating this amount.

In addition, individuals often forget to include the total amount withheld on Line 3. This figure is vital for the state to understand how much tax has been withheld from the payments made to contractors. Missing this information can complicate your tax obligations.

Some filers neglect to attach the necessary copies of the Form 1099-MISC. These forms must accompany the NJ W3 form to verify the payments made to contractors. Ensure that you include all relevant documentation to avoid any issues with your submission.

Another mistake is mailing the forms to the wrong address. The completed NJ W3 form and the 1099 MISC forms should be sent to the designated address in Trenton, NJ. Double-check the mailing address to prevent delays in processing.

Additionally, it is essential to remember that both sides of the NJ W3 form must be completed. Failing to fill out one side can lead to rejection or requests for additional information, which could delay your filing.

Many people also forget to sign the form. Both the taxpayer and the preparer must provide their signatures and dates. Missing signatures can result in the form being considered incomplete.

Lastly, ensure that you mail the form by the deadline. The NJ W3 form must be submitted no later than February 28 or within 30 days after the close of the month in which your business has ceased. Missing the deadline can lead to penalties and interest on any unpaid taxes.

By being aware of these common mistakes, you can take the necessary steps to complete the NJ W3 form accurately and efficiently. Taking the time to review your submission before mailing it can save you from unnecessary complications.

What is the NJ W3 form?

The NJ W3 form, specifically known as Schedule NJ-W-3-UNC, is used for the Annual Reconciliation of Gross Income Tax Withheld from Unregistered Unincorporated Contractors in New Jersey. It is required for reporting payments made to unregistered contractors and the corresponding tax withheld during the year. This form ensures compliance with New Jersey tax laws and helps maintain accurate records of tax obligations.

Who needs to file the NJ W3 form?

Both New Jersey employers and non-New Jersey employers may need to file the NJ W3 form. New Jersey employers must report withholding payments made on behalf of unregistered contractors using the NJ W3 form along with the NJ-500 and/or NJ-927/927W forms. Non-New Jersey employers use this form to report all withholding payments made during the year, alongside Form NJ-550.

What information is required on the NJ W3 form?

The NJ W3 form requires several key pieces of information. You must provide your New Jersey Taxpayer Identification Number, the names of the contractors, the total gross compensation paid to them, and the total amount withheld. Additionally, you will need to attach copies of the corresponding Form 1099-MISC for each contractor, which reports the payments and taxes withheld.

When is the NJ W3 form due?

The NJ W3 form is due no later than February 28 of the year following the tax year being reported. If your business ceases operations, the form must be submitted within 30 days after the close of the month in which the business ended. Timely filing is crucial to avoid penalties and ensure compliance with state tax regulations.

Where should the NJ W3 form be mailed?

The completed NJ W3 form, along with the attached Form 1099-MISC, should be mailed to the following address: State of New Jersey - GIT, PO Box 629, Trenton, NJ 08646-0629. Ensure that all sections of the form are completed before mailing to avoid any processing delays.

Here are some common misconceptions about the NJ W3 form, along with clarifications:

This form is required for both New Jersey employers and non-New Jersey employers who have made payments to unregistered unincorporated contractors.

The NJ W3 form must be submitted no later than February 28 or within 30 days after your business has ceased operations.

It is essential to attach copies of the corresponding recipient income statements (Form 1099-MISC) and a totaled list of amounts withheld.

Currently, the NJ W3 form must be mailed to the specified address and cannot be filed electronically.

All payments made to unregistered unincorporated contractors during the year must be reported, regardless of the amount.

Only the official NJ Taxpayer Identification Number should be used on the NJ W3 form.

The NJ W3 form is an annual reconciliation, while the NJ-550 is a monthly return of withholding from unregistered unincorporated contractors.

Late submission of the NJ W3 form can result in penalties, so timely filing is crucial.

The NJ W3 form shares similarities with the IRS Form W-2, which is used by employers to report wages paid to employees and the taxes withheld from those wages. Both forms serve the purpose of reconciling income and tax withholdings for a specific tax year. The W-2 is submitted to both the employee and the IRS, while the NJ W3 is specifically tailored for reporting payments made to unregistered contractors in New Jersey. Both forms require detailed information about the taxpayer, including identification numbers and total amounts withheld, ensuring accurate reporting for tax purposes.

Another related document is the IRS Form 1099-MISC, which reports miscellaneous income, including payments made to independent contractors. Like the NJ W3, the 1099-MISC is used to report tax withheld on payments made throughout the year. The NJ W3 requires the attachment of 1099-MISC forms when reporting payments to unregistered contractors, illustrating the interconnectedness of these forms in the tax reporting process. Both documents aim to ensure that income is accurately reported and taxes are appropriately withheld.

If you're in the process of transferring ownership, understanding the details of a horse transaction is critical. For this, consider utilizing a "thorough guide to the Horse Bill of Sale" found at https://californiapdfforms.com/horse-bill-of-sale-form/.

The NJ-500 form is also similar, as it is used by employers to report withholding payments made to unregistered unincorporated contractors on a monthly basis. While the NJ W3 serves as an annual reconciliation, the NJ-500 provides a more frequent reporting mechanism. Employers must compile the information from the NJ-500 when completing the NJ W3, making the two forms complementary in nature. Both documents require accurate reporting of payments and withholdings to ensure compliance with state tax laws.

In addition, the NJ-927 form functions similarly as a quarterly report of employee and contractor withholdings. Employers use the NJ-927 to summarize their withholding obligations throughout the year, which then informs the annual reporting on the NJ W3. The information contained in the NJ-927 is crucial for the accurate completion of the NJ W3, as it provides a detailed account of the amounts withheld from contractors. Both forms aim to ensure transparency and compliance in tax reporting.

The IRS Form 941 is another document that bears resemblance to the NJ W3. This form is used by employers to report income taxes, Social Security tax, and Medicare tax withheld from employee wages. While the NJ W3 focuses specifically on unregistered contractors, both forms require similar information regarding the taxpayer and the amounts withheld. They both serve as reconciliation tools, ensuring that the taxes reported and paid align with the amounts withheld throughout the year.

Additionally, the IRS Form 945 is relevant, as it is used to report federal income tax withheld from non-payroll payments, including payments to independent contractors. Like the NJ W3, the Form 945 serves as a reconciliation tool, summarizing the total amounts withheld for a tax year. Both forms require detailed reporting of payments made and taxes withheld, reinforcing the importance of accurate reporting in compliance with tax regulations.

Finally, the New Jersey Division of Taxation's Annual Reconciliation of Withholding (Form NJ-W-3) is comparable to other state-specific reconciliation forms used across the United States. These forms serve a similar purpose in providing a summary of withholding for various types of income, ensuring that taxpayers report their income accurately and comply with state tax laws. Each state may have its own specific requirements, but the overarching goal remains consistent: to provide a clear accounting of income and taxes withheld throughout the year.