Valid Promissory Note Document for the State of New Jersey

Valid Promissory Note Document for the State of New Jersey

| Fact Name | Details |

|---|---|

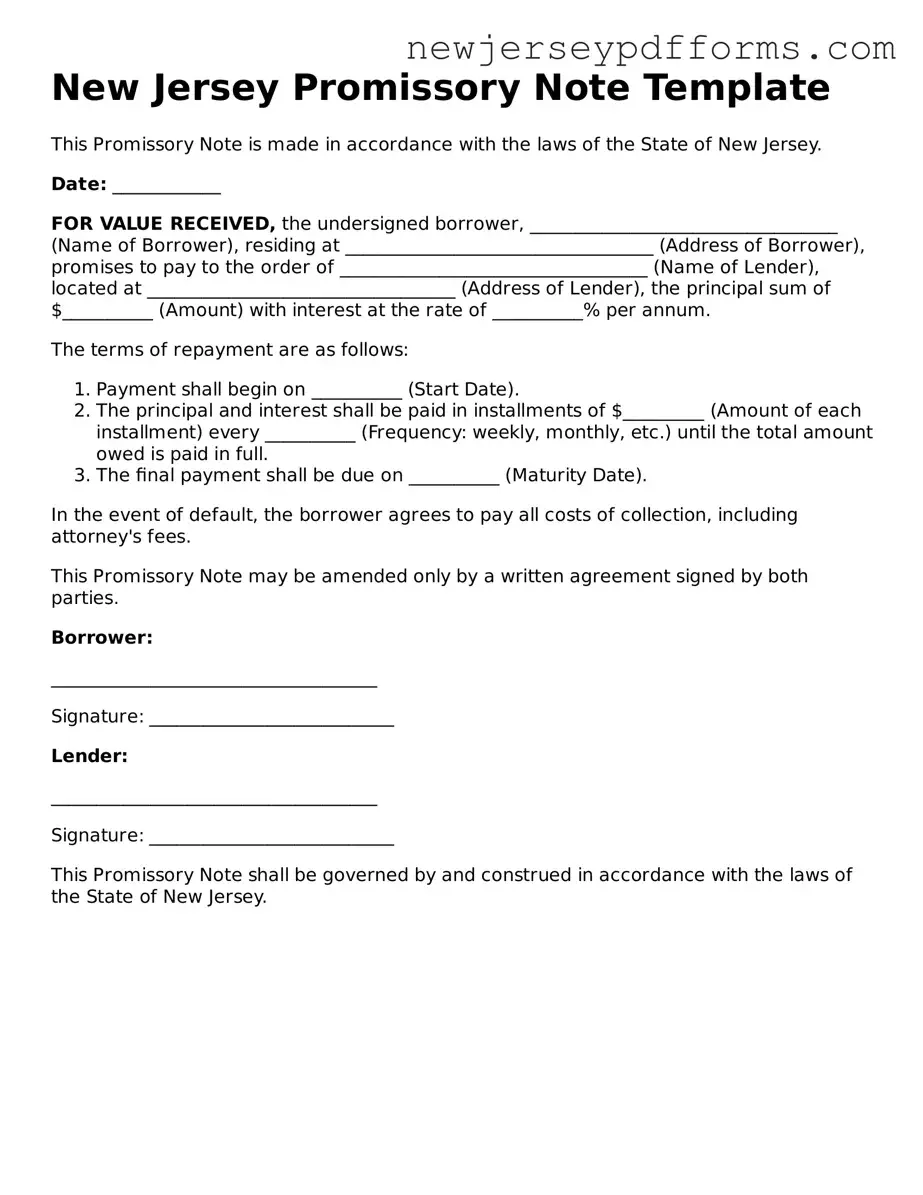

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated person or entity at a defined time. |

| Governing Law | In New Jersey, promissory notes are governed by the New Jersey Uniform Commercial Code (UCC), specifically N.J.S.A. 12A:3-104. |

| Parties Involved | The two main parties are the maker (the person who promises to pay) and the payee (the person to whom the payment is owed). |

| Key Elements | A valid promissory note includes the amount, the interest rate (if any), the due date, and the signatures of the involved parties. |

| Interest Rates | Interest rates on promissory notes in New Jersey must comply with state usury laws, which limit the maximum allowable interest rate. |

| Enforceability | To be enforceable, a promissory note must be clear and unambiguous in its terms and conditions. |

| Transferability | Promissory notes can often be transferred to other parties, making them negotiable instruments under the UCC. |

| Default Consequences | If the maker defaults on the note, the payee may pursue legal action to recover the owed amount, including interest and fees. |

New Jersey Power of Attorney Form - Regularly updating your POA can keep it aligned with your current life circumstances and goals.

Nj Gun Permit Application Pdf - Buyers and sellers can utilize this form to ensure compliance with local and federal laws.

Nj Bill of Sale - The form can be stored for personal records or provided to the buyer as proof of sale.

Filling out a New Jersey Promissory Note form can be straightforward, but many people make common mistakes that can lead to issues later on. One frequent error is not including all required information. The form asks for specific details, such as the names of the borrower and lender, the loan amount, and the repayment terms. Omitting any of these details can render the document incomplete.

Another common mistake is failing to clearly define the interest rate. If the interest rate is not specified or is written ambiguously, it can lead to confusion or disputes down the line. It is crucial to state whether the interest is fixed or variable and to provide the exact percentage.

People often overlook the importance of dates. A mistake in the date can affect the validity of the note. Ensure that the date of the agreement and the repayment schedule are accurate. Inaccurate dates can complicate enforcement of the note if payment issues arise.

Some individuals neglect to include a repayment schedule. The Promissory Note should outline how and when payments will be made. A vague or missing repayment schedule can create misunderstandings between the borrower and lender.

Another mistake is not having the document signed by both parties. A Promissory Note is only valid when it is signed by the borrower and lender. Without signatures, the document may not hold up in court if disputes occur.

Additionally, many people fail to keep copies of the signed note. After signing, it is essential to make copies for both the borrower and the lender. This helps ensure that both parties have a record of the agreement and its terms.

Some individuals also forget to include any collateral details if applicable. If the loan is secured by collateral, this should be clearly stated in the document. Not mentioning collateral can lead to complications if the borrower defaults.

Another common error is not reviewing the document for errors before finalizing it. Typos or incorrect information can lead to misunderstandings. Taking the time to proofread the document can prevent future issues.

People sometimes fail to consider state-specific laws. New Jersey has specific requirements for Promissory Notes. Not adhering to these laws can make the document unenforceable. It is important to ensure that the note complies with state regulations.

Lastly, some individuals do not seek legal advice when needed. While filling out the form may seem simple, legal nuances can arise. Consulting with a legal professional can provide clarity and ensure that the Promissory Note is properly executed.

What is a New Jersey Promissory Note?

A New Jersey Promissory Note is a written promise to pay a specific amount of money to a designated person or entity at a specified time or on demand. It serves as a legal document that outlines the terms of the loan, including the interest rate and repayment schedule.

Who uses a Promissory Note?

Individuals and businesses often use Promissory Notes. They are commonly utilized in personal loans, business transactions, and real estate deals. The note can be used by lenders to formalize an agreement with borrowers.

What are the key components of a Promissory Note?

A typical Promissory Note includes the following components: the names of the borrower and lender, the principal amount, the interest rate, the repayment terms, and any penalties for late payments. It may also specify whether the note is secured or unsecured.

Is a Promissory Note legally binding?

Yes, a Promissory Note is a legally binding document. Once signed by both parties, it can be enforced in court if the borrower fails to repay the loan as agreed. It is important to ensure that the terms are clear and mutually understood.

Do I need a lawyer to create a Promissory Note?

While it is not required to have a lawyer, consulting one can be beneficial. A legal professional can help ensure that the note meets all legal requirements and adequately protects your interests.

Can a Promissory Note be modified?

Yes, a Promissory Note can be modified if both parties agree to the changes. It is advisable to document any modifications in writing and have both parties sign the amended note to avoid future disputes.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, the lender may take legal action to recover the owed amount. This could include filing a lawsuit or seeking a judgment. The specific actions depend on the terms outlined in the Promissory Note.

Are there any tax implications related to a Promissory Note?

Yes, there may be tax implications for both the lender and borrower. Interest income may be taxable for the lender, while the borrower may not be able to deduct the interest unless it is for a qualified purpose. Consulting a tax professional is recommended.

Can a Promissory Note be transferred to another party?

A Promissory Note can often be transferred or assigned to another party, depending on the terms of the note. The new holder of the note will have the right to collect payments under the original agreement.

Where can I obtain a New Jersey Promissory Note form?

Promissory Note forms can be found online through legal document websites, office supply stores, or legal professionals. It is important to ensure that the form complies with New Jersey laws and suits your specific needs.

Many people have misunderstandings about the New Jersey Promissory Note form. Here are some common misconceptions:

The New Jersey Promissory Note form shares similarities with the Loan Agreement. Both documents outline the terms under which money is borrowed and specify the repayment schedule. A Loan Agreement, however, tends to be more comprehensive, often including clauses related to default, collateral, and other conditions. In contrast, a Promissory Note is typically more straightforward, focusing on the borrower's promise to repay the loan amount with interest.

Another document akin to the New Jersey Promissory Note is the Mortgage. While a Promissory Note represents a promise to repay a loan, a Mortgage secures that promise with the property being financed. If the borrower defaults on the Promissory Note, the lender can initiate foreclosure on the property to recover the owed amount. Thus, the Mortgage adds an additional layer of security for the lender.

The New Jersey Promissory Note is also similar to a Personal Guarantee. In a Personal Guarantee, an individual agrees to be personally responsible for a debt or obligation incurred by another party. This document provides assurance to the lender that, should the primary borrower fail to repay, the individual will cover the debt. Both documents serve to protect the lender's interests, but a Personal Guarantee extends liability beyond the borrower.

A Business Loan Agreement is another document that resembles the New Jersey Promissory Note. Similar to a standard Loan Agreement, this document is specifically tailored for business transactions. It outlines the terms of the loan, including repayment schedules and interest rates. However, a Business Loan Agreement may also incorporate terms unique to business operations, such as performance covenants or financial reporting requirements.

When dealing with various financial documents, such as a Sample Tax Return Transcript, it's crucial to understand their importance in facilitating transactions and verifications. For instance, when you're preparing for a loan, having a clear overview of your financial situation through documents like the Sample Tax Return Transcript can be pivotal. To further assist with documentation needs, resources like PDF Document Service can provide templates and guidance.

The New Jersey Promissory Note can also be compared to an Installment Sale Agreement. In both cases, the buyer agrees to pay for a purchase over time, typically in regular installments. However, in an Installment Sale Agreement, the seller retains ownership of the property until the final payment is made. This contrasts with a Promissory Note, where ownership of the borrowed amount is transferred immediately upon receipt of funds.

Another document that bears similarities is the Secured Note. Like the New Jersey Promissory Note, a Secured Note includes a promise to repay a loan. However, a Secured Note is backed by collateral, which provides additional security to the lender. If the borrower defaults, the lender has the right to seize the collateral to satisfy the debt, whereas a standard Promissory Note may not offer such protections.

The New Jersey Promissory Note is also comparable to a Conditional Sales Agreement. In this agreement, the seller retains ownership of the goods until the buyer fulfills specific conditions, often related to payment. While both documents involve a promise to pay, a Conditional Sales Agreement typically relates to the sale of goods rather than a cash loan, making it a unique variant in the landscape of financial agreements.

Lastly, the New Jersey Promissory Note is similar to a Credit Agreement. A Credit Agreement outlines the terms under which a lender extends credit to a borrower. Like a Promissory Note, it specifies repayment terms and conditions. However, a Credit Agreement often encompasses a broader range of financial terms, including interest rates, fees, and conditions for drawing on the credit line, making it a more detailed document than a standard Promissory Note.