Printable St 7 New Jersey Form

Printable St 7 New Jersey Form

| Fact Name | Fact Description |

|---|---|

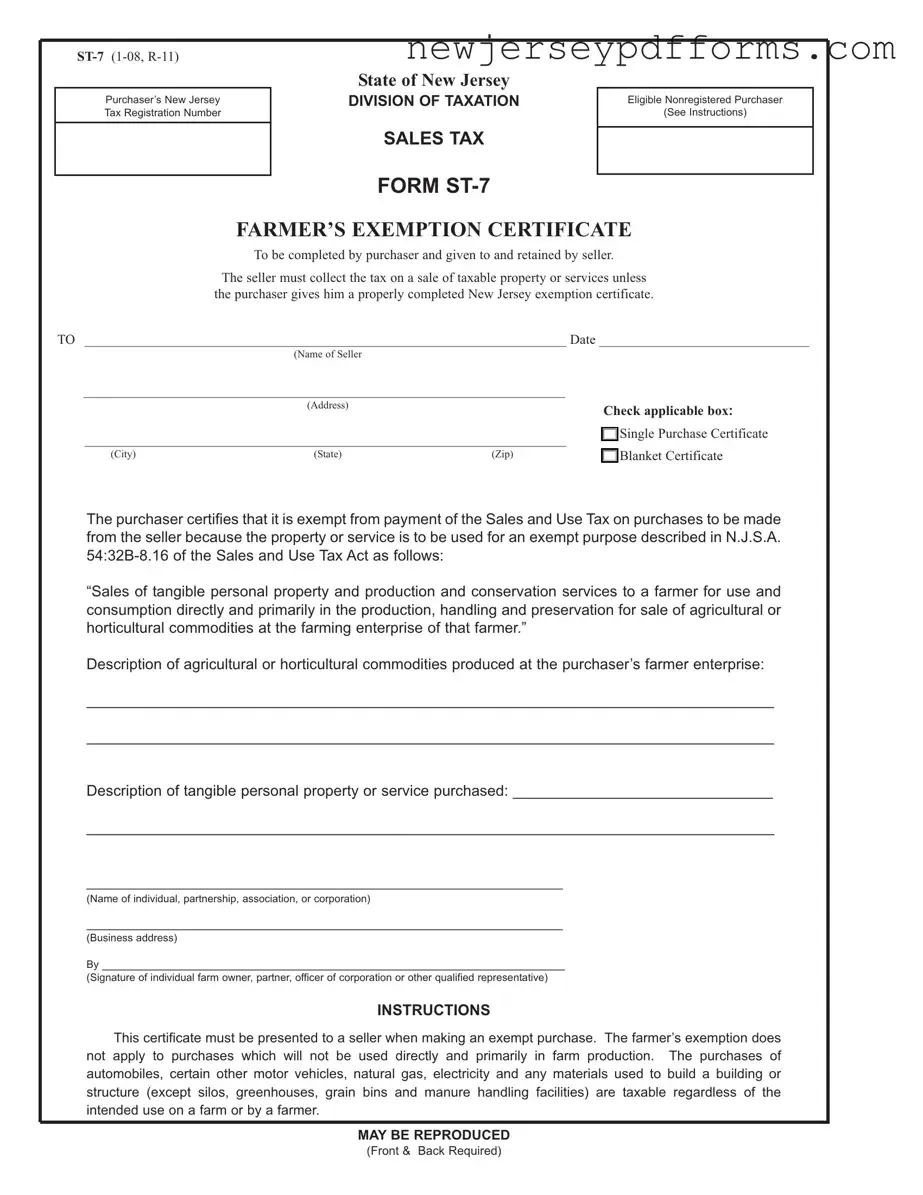

| Form Purpose | The ST-7 form serves as a Farmer’s Exemption Certificate, allowing eligible farmers to purchase certain items without paying sales tax. |

| Governing Law | This form is governed by the New Jersey Sales and Use Tax Act, specifically N.J.S.A. 54:32B-8.16. |

| Eligible Purchasers | Only businesses recognized as "farming enterprises" under the law can utilize this exemption certificate. |

| Exempt Items | The exemption applies to tangible personal property and services used directly in agricultural production, excluding certain vehicles and utilities. |

| Certificate Retention | Sellers must keep the completed ST-7 forms for at least four years from the date of sale. |

| Good Faith Acceptance | Sellers who accept the ST-7 in good faith are relieved from liability regarding the collection of sales tax on the transaction. |

How to Fill Out Iowa W-4 - The clarity of your financial situation will help in filling out the NJ W-4 accurately.

Nj Transit Bus Fare Price - Applicants should understand the importance of detailing their specific impairments on the form.

To simplify the process of finding the right tenant, many landlords turn to the Rental Application form, a vital tool designed to collect key details about prospective renters. By ensuring that all information is completed properly, applicants can improve their chances of success in securing a rental property. For those interested in streamlining this process, templates are available through services like PDF Document Service, which can help facilitate the application preparation.

What Are the 6 Points of Id - A signature is mandatory to validate the application; unstamped signatures will not be accepted.

When filling out the ST-7 New Jersey form, many people make common mistakes that can lead to delays or issues with their exemption claims. One of the most frequent errors is not providing the New Jersey Tax Registration Number. This number is essential for identifying the purchaser. If you do not have one, you must include your Federal Identification Number or, if you are a sole proprietor, the last three digits of your Social Security Number. Forgetting this step can invalidate your exemption.

Another mistake is failing to properly describe the agricultural or horticultural commodities produced at your farming enterprise. The form requires a clear description of what you produce. If this section is vague or incomplete, it may raise questions about your eligibility for the exemption. Sellers need specific information to ensure compliance with tax regulations.

Additionally, some individuals do not date the form. This is a crucial step. Without a date, the seller may have difficulty verifying when the exemption was claimed. It is also important to ensure that the form is signed by the appropriate person, such as the farm owner or a qualified representative. An unsigned form can lead to complications.

Many people also overlook the importance of indicating whether the certificate is a single purchase or a blanket certificate. This distinction matters because it affects how the seller processes the exemption. A blanket certificate allows for multiple purchases, but it must be clearly marked to avoid confusion in future transactions.

Another common error is using the certificate for purchases that are not eligible for exemption. For instance, items like motor vehicles or construction materials (with some exceptions) do not qualify. Misunderstanding the scope of the exemption can lead to tax liabilities that could have been avoided.

Lastly, individuals sometimes fail to keep a copy of the certificate for their records. Sellers are required to retain these documents for a minimum of four years. If questions arise later, having a copy can help clarify any issues. Proper record-keeping is essential for both parties involved in the transaction.

What is the ST-7 form used for?

The ST-7 form, also known as the Farmer’s Exemption Certificate, is used by farmers in New Jersey to certify that their purchases of certain tangible personal property and services are exempt from sales tax. This exemption applies specifically to items that will be used directly and primarily in agricultural or horticultural production. By presenting this form to sellers, farmers can avoid paying sales tax on qualifying purchases, thereby supporting their farming operations.

Who is eligible to use the ST-7 form?

Only businesses classified as “farming enterprises” under New Jersey law can use the ST-7 form. This includes those engaged in the production of agricultural or horticultural commodities for sale, such as dairy, poultry, fruits, vegetables, and livestock. However, it’s important to note that the exemption does not apply to purchases that are not used directly in farm production, such as automobiles or materials for building structures, with a few exceptions like silos and greenhouses.

How should the ST-7 form be completed?

When completing the ST-7 form, the purchaser must fill in the seller's name and address, select whether it is a single purchase or a blanket certificate, and provide a description of the agricultural products produced. Additionally, the form requires the purchaser’s signature and the date. If the purchaser is not registered in New Jersey, they must include their Federal Identification Number or, if a sole proprietor, the last three digits of their Social Security Number. It’s essential to ensure that all information is accurate and complete to maintain the validity of the exemption.

What happens if the ST-7 form is not properly executed?

If the ST-7 form is not properly filled out or if it does not meet the necessary requirements, the sales transaction may be deemed taxable. In such cases, the seller is responsible for collecting the sales tax, and the burden of proof that the tax was not required falls on them. Therefore, it is crucial for both purchasers and sellers to ensure that the form is completed correctly to avoid any tax liabilities.

How long must sellers retain the ST-7 form?

Sellers are required to retain the ST-7 form for a minimum of four years from the date of the sale covered by the certificate. Keeping these records is important for compliance with tax regulations and may be necessary in the event of an audit or inquiry from tax authorities.

Understanding the Farmer’s Exemption Certificate, known as the ST-7 form in New Jersey, can be tricky. Here are some common misconceptions that people often have about this form:

Being aware of these misconceptions can help farmers navigate the tax system more effectively and ensure they are complying with New Jersey's regulations. Understanding the specifics of the ST-7 form is essential for making the most of the available exemptions.

The ST-4 Exempt Use Certificate serves a similar purpose as the ST-7 form. It allows purchasers to claim exemption from sales tax on certain purchases that will be used for exempt purposes. While the ST-7 is specifically for farmers, the ST-4 can be used by various entities, including those purchasing vehicles for exempt use. Both forms require the purchaser to provide identification information and a description of the items being purchased, ensuring that the seller can validate the exemption claim.

The ST-5 Resale Certificate is another document that shares similarities with the ST-7. This certificate is used by businesses to purchase goods intended for resale without paying sales tax. Like the ST-7, the ST-5 requires the purchaser to provide their tax identification number and details about the items being purchased. The key difference is that the ST-5 is focused on resale, whereas the ST-7 is aimed at exempt agricultural purchases.

The ST-8 Exempt Organization Certificate is also comparable to the ST-7. This form allows qualifying nonprofit organizations to make tax-exempt purchases. Both documents require the purchaser to certify their eligibility for exemption and provide relevant identification. However, the ST-8 is specifically designed for organizations, while the ST-7 targets individual farmers and farming enterprises.

The ST-3 Sales Tax Exempt Certificate is another related document. It is used for purchases made by government entities or certain exempt organizations. Similar to the ST-7, it requires the buyer to provide their identification and a description of the items being purchased. The main distinction lies in the type of purchaser; the ST-3 is for government or exempt entities, while the ST-7 is for farmers.

The ST-9 Certificate of Exempt Use is another form that parallels the ST-7. This document is utilized for specific exempt uses not covered by other certificates. Both forms require detailed descriptions of the intended use of the purchased items. However, the ST-9 is broader in scope, covering various exempt uses beyond just agricultural purposes.

The ST-10 Certificate of Exempt Sale is also similar to the ST-7. It is used for sales that are exempt from sales tax due to specific conditions. Both forms require the purchaser to provide relevant identification and a description of the items. The ST-10 is more general, while the ST-7 is specifically tailored for agricultural purchases.

The ST-11 Direct Payment Certificate is another document that bears resemblance to the ST-7. It allows certain purchasers to pay sales tax directly to the state rather than to the seller at the point of sale. Both forms require the purchaser to provide identification and details about the transaction. The ST-11 is typically used by larger businesses, while the ST-7 is focused on individual farmers.

Lastly, the ST-12 Sales Tax Exempt Certificate is similar to the ST-7 in that it allows certain transactions to be exempt from sales tax. This form is often used by educational institutions and government agencies. Both require the purchaser to provide identification and a description of the exempt items. The ST-12 is specific to educational and governmental entities, while the ST-7 is specifically for agricultural purchases.